Costco Wholesale Corporation’s COST March sales update offers a fresh perspective on the retail giant’s momentum. As a dominant force in the warehouse club segment with a consistent history of growth, Costco has been investors' favorite stock. Yet, the latest sales figures raise an important question: Is now the right time to buy, hold or book profits on Costco stock?

The March report showed solid comparable sales growth across regions and an acceleration in e-commerce, strengthening the narrative that Costco’s operational execution and customer loyalty remain intact despite a challenging retail backdrop.

Decoding Costco’s March Sales Report

Costco’s membership-driven model remains a core strength, with high renewal rates ensuring a dependable revenue stream. Its efficient supply chain and bulk purchasing power enable competitive pricing, reinforcing its strong market position. This combination of customer loyalty and operational efficiency continues to give Costco an advantage in a competitive retail landscape.

For the five weeks ended April 5, 2026, Costco reported a 9.4% year-over-year increase in total comparable sales. Regionally, comparable sales rose 8.7% in the United States, 10.7% in Canada and 11.9% in Other International markets. Digitally enabled comparable sales in March surged 23.3%. (Read: Costco's Comparable Sales Stay Resilient Despite Calendar Headwind)

As a result, Costco's net sales for March rose 11.3% to $28.41 billion, up from $25.51 billion in the same period last year. This follows a sales improvement of 9.5% in February and 9.3% in January.

A Sneak Peek Into Costco’s Tailwinds

Costco continues to demonstrate the strength of its membership-driven model, which underpins a stable and recurring revenue base. The annual fee structure not only ensures predictable income but also reinforces a sense of exclusivity and value for members. This dynamic was evident in the second quarter of fiscal 2026 when membership fee income advanced 13.6% year over year, supported by robust renewal rates of 92.1% in the United States and Canada and 89.7% globally, highlighting strong customer engagement.

The company’s focus on value remains central to its competitive positioning. By offering high-quality merchandise at prices lower than its peers, Costco reinforces customer loyalty and encourages frequent store visits. Its curated merchandising strategy, featuring a dynamic assortment of essentials, seasonal goods and unique offerings, keeps the shopping experience engaging while driving incremental purchases.

Private label expansion remains a key differentiator, with the Kirkland Signature brand playing an important role in driving both customer loyalty and margin efficiency. Known for delivering premium quality at compelling price points, Kirkland enhances Costco’s value proposition. The ongoing addition of new products across categories further strengthens brand equity and supports profitability. Costco launched about 30 new Kirkland items in the second quarter.

At the same time, Costco is leveraging technology to enhance the overall member experience and operational efficiency. Investments in digital capabilities are yielding tangible results, with online sales benefiting from strong traffic growth across both the website and mobile app. Enhancements such as mobile payment solutions, pharmacy pre-payment options and in-store automation initiatives are streamlining the shopping and complementing the company’s integrated omnichannel approach.

Costco’s growth trajectory remains supported by a disciplined expansion strategy. The company continues to add new warehouse locations in high-potential markets while maintaining a measured pace that supports productivity and returns. For fiscal 2026, the company expects to open 28 net new warehouses and is targeting 30-plus warehouse openings annually over the longer term. With plans to accelerate new openings in the coming years, this steady expansion, combined with strong membership growth, positions Costco well to sustain long-term revenue and earnings momentum.

Costco Navigates a Competitive Landscape as Peers Scale Up

Costco's impressive sales figures are part of a larger retail picture where competition is intensifying. Rivals like Ross Stores, Inc. ROST, Dollar General Corporation DG and Target Corporation TGT are investing in expanding their product assortments, enhancing supply-chain efficiency, and upgrading in-store and digital experiences to capture greater market share. These retailers are also sharpening their value propositions through competitive pricing, private-label expansion and targeted promotional strategies.

Margins remain a critical area to monitor, with potential concerns stemming from any deleverage in the selling, general and administrative rate. Foreign exchange volatility and potential tariffs on key imports create uncertainty.

Does Costco Tick the Boxes for Value Investing?

Costco stock has gained 2.5% over the past three months compared with the industry’s rise of 3.2%. A sneak peek into key retail peers' performance reveals that shares of Dollar General have fallen 21.4% during the said time frame, while Ross Stores and Target have climbed 14% and 6.1%, respectively.

Image Source: Zacks Investment Research

The stock is trading at a significant premium to its peers. Costco's forward 12-month price-to-earnings ratio stands at 45.48, higher than the industry’s ratio of 32.78 and the S&P 500's 21.29. Costco is trading at a premium to Target (with a forward 12-month P/E ratio of 14.49), Ross Stores (29.78) and Dollar General (16.07).

Image Source: Zacks Investment Research

Costco continues to trade at a notable premium to its peers, reflecting investor confidence in its strong brand image, loyal membership base and long-term growth potential.

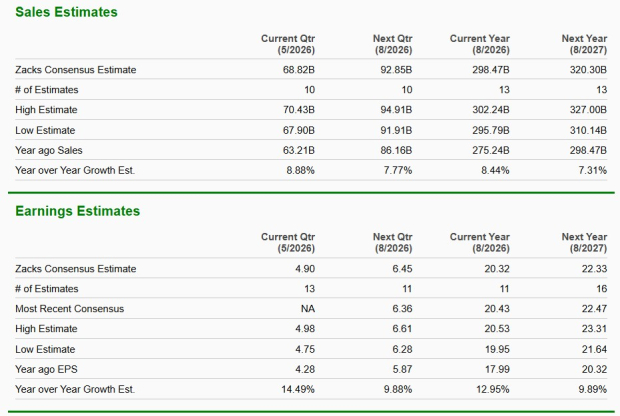

How Consensus Estimates Stack Up for Costco

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 8.4% and 13%, respectively. For the next fiscal year, the consensus estimate indicates a 7.3% rise in sales and 9.9% growth in earnings.

Image Source: Zacks Investment Research

How to Play Costco: Buy, Hold or Sell?

Costco’s March sales performance reinforces its core strengths — resilient demand, a highly loyal membership base, and strong execution across both physical and digital channels — indicating that the company’s long-term growth story remains intact despite a competitive and uncertain retail environment. However, the stock’s premium valuation suggests that much of this strength is already reflected in its price, leaving limited room for near-term upside. Existing investors should hold the stock, as the business fundamentals remain solid and are worth staying invested. For potential investors, it may be prudent to wait for more attractive entry points rather than chasing the stock at elevated levels, while those seeking to lock in gains could consider partial profit-booking without fully exiting a fundamentally strong name.

Costco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Dollar General Corporation (DG): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Ross Stores, Inc. (ROST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).