Despite dominating the cloud computing and artificial intelligence (AI) space, Microsoft (MSFT) stock has gone nowhere.

Over the past year, shares have fallen roughly 9.6%, lagging rivals such as Alphabet (GOOG) (GOOGL), whose stock has surged on AI enthusiasm, and Amazon (AMZN) , which has gained 28%.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Microsoft’s underperformance relative to peers suggests its AI strategy is becoming expensive.

www.barchart.com

www.barchart.comWhy Microsoft Stock Has Struggled?

Microsoft is spending aggressively to win the AI race. The company plans to spend nearly $190 billion on capital expenditures in 2026, including roughly $25 billion on rising component costs.

Those investments are pressuring margins and frustrating investors looking for faster, near-term returns.

At the same time, management expects only a modest acceleration in Azure (its cloud computing platform) growth in the near future, even as spending ramps higher. Ongoing supply constraints, especially around AI infrastructure capacity, are expected to persist through at least 2026, limiting Microsoft's ability to meet demand.

In short, soaring spending and only gradual growth have weighed heavily on sentiment.

The Bull Case Investors May Be Overlooking

While MSFT stock has underperformed, the key issue isn’t demand. Microsoft continues to see strong enterprise adoption of AI tools, rising usage across its cloud platform, and expanding customer demand for compute capacity. In other words, the business fundamentals remain intact.

In the latest quarter, Microsoft generated $82.9 billion in revenue, up 18% year-over-year. Microsoft Cloud revenue climbed 29% to $54.5 billion, while Azure and related cloud services grew 40%, driven by broad enterprise AI adoption across industries and geographies.

More importantly, management said demand continues to exceed available capacity. This doesn’t indicate that MSFT’s business is slowing.

Supporting its investment case is the strong commercial remaining performance obligation (RPO), which surged 99% to $627 billion. Roughly one-quarter of that backlog is expected to convert into revenue over the next 12 months. Further, MSFT’s longer-duration commitments jumped 138%.

Those numbers suggest customers are not pulling back. They are locking in long-term commitments to AI and cloud spending.

At the same time, Microsoft’s AI business has become enormous. The company said its AI revenue run rate now exceeds $37 billion annually, growing 123% year-over-year. Copilot adoption is accelerating rapidly, with paid seats surpassing 20 million, up 250% from last year. Even more notable, the number of enterprises deploying more than 50,000 seats has quadrupled.

Looking ahead, management expects continued momentum. Intelligent Cloud revenue is projected to reach as much as $38.25 billion next quarter, representing growth of up to 28%, while Azure growth is expected to remain near 40% in constant currency.

Management believes the current constraints are temporary rather than structural. If additional AI infrastructure comes online over the next several quarters, Azure growth could meaningfully reaccelerate in the second half of 2026. If that happens, today’s heavy AI spending may ultimately look less like margin pressure and more like the foundation of Microsoft’s next major growth cycle.

Microsoft May Be the Cheapest AI Megacap Stock

What makes MSFT stock compelling is its valuation. Despite its dominant positions in enterprise software, cloud infrastructure, and generative AI, Microsoft trades at a more attractive valuation than peers like Alphabet and Amazon. That creates a potentially compelling opportunity for long-term investors.

Microsoft currently trades at a forward P/E ratio of 24.3, below Alphabet’s 27.1 and far cheaper than Amazon’s 34.5.

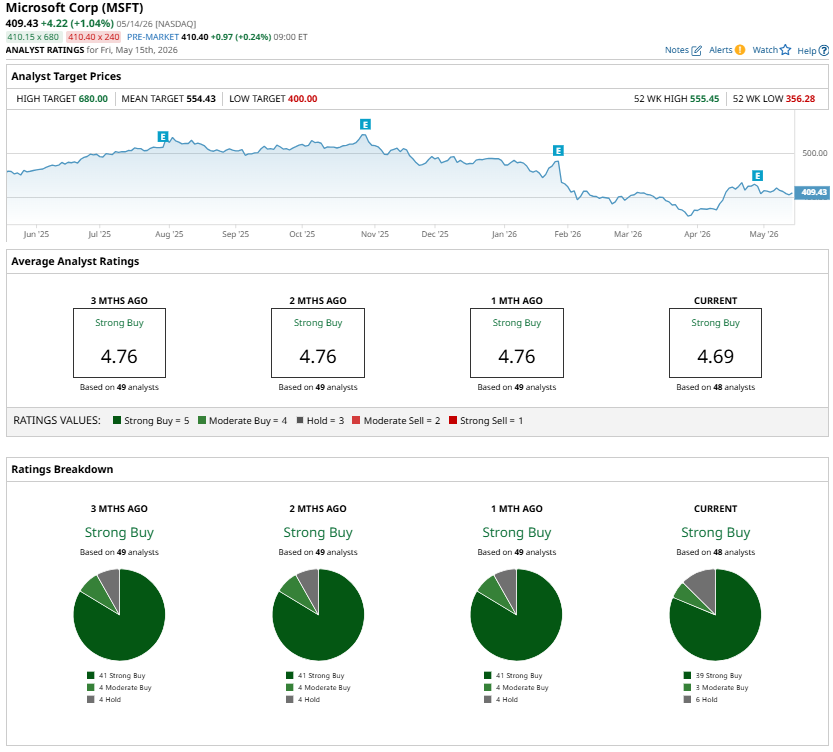

Further, Wall Street is bullish on MSFT stock. Analysts continue to rate Microsoft a “Strong Buy.”

Billionaire investor Bill Ackman is making the same bet. Ackman’s hedge fund, Pershing Square Capital Management, initiated a new position in Microsoft, citing an attractive valuation.

All these indicate that if Azure growth accelerates as supply constraints ease, Microsoft stock may not stay cheap for long.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Microsoft Stock Is an AI Bargain That Investors Are Missing Nvidia’s AI Lead Is Back in Focus as Wolfe Research Doubles Down A $1.5 Trillion Reason to Buy Taiwan Semi Stock Here