Netflix (NFLX) stock has fallen 28.72% from its 52-week high, as the market grew cautious about the streaming giant’s growth outlook, profitability, and leadership transition.

Despite delivering a strong first-quarter performance, Netflix management maintained its full-year 2026 revenue guidance instead of raising expectations. That surprised investors who expected management to signal accelerating momentum. The decision immediately raised concerns that Netflix may be seeing slower growth ahead.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Profitability concerns have also added pressure to the stock. Netflix expects a second-quarter operating margin of 32.6%, compared to 34.1% in the same period last year. The projected margin compression reflects higher amortization expenses for content.

Another factor creating uncertainty is the upcoming leadership transition. Netflix co-founder and chairman Reed Hastings will step down when his term expires in June. Hastings has played a central role in turning Netflix into a global streaming leader, and his departure marks the end of an important era for the company. Founder departures often make investors nervous about execution risk.

Still, the market may be overlooking what continues to work exceptionally well at Netflix.

Subscriber engagement remains strong. The company continues to dominate global streaming, its advertising business is expanding, and free cash flow generation remains impressive. Importantly, the recent stock decline has eased valuation concerns, potentially creating a more attractive entry point for investors.

www.barchart.com

www.barchart.com Netflix Stock: Why the Long-Term Bull Case Still Looks Strong

Despite the recent correction, Netflix continues to dominate global streaming. Subscriber engagement remains exceptionally strong, supported by a steady pipeline of original content. The platform’s scale advantage continues to separate Netflix from competitors struggling to achieve profitability.

Importantly, Netflix is diversifying its content. Management is aggressively expanding into new formats, including gaming and video podcasts, as the company seeks to deepen engagement and increase the time users spend on its platform.

Another major strength is its ability to increase pricing. Notably, Netflix recently raised subscription prices while still adding subscribers. This shows its appeal to subscribers.

Meanwhile, Netflix’s advertising-supported tier is rapidly becoming a meaningful growth engine. The company’s ad business is expected to grow aggressively in 2026, with management projecting revenue to reach $3 billion this year. The segment creates a powerful second revenue stream alongside subscriptions while also helping Netflix attract more price-sensitive consumers.

Margins may face some near-term pressure, but management still expects operating leverage to improve in the second half of the year and reaffirmed its full-year operating margin target of 31.5%. That matters because it suggests Netflix can continue investing heavily in content and platform expansion while still driving long-term earnings growth.

And valuation finally looks more reasonable. After years of trading at premium valuation multiples, Netflix stock now trades at 24.36 times forward earnings following the recent selloff. Given analysts' expectations of earnings growth of more than 42% in 2026, that valuation multiple appears compelling.

Is Netflix Stock a Buy After the Selloff?

Netflix faces short-term challenges. Further, competition remains intense, content spending is enormous, and leadership transitions always introduce execution uncertainty. But Netflix’s prospects remain solid.

The company continues to benefit from strong user engagement, growing advertising revenue, pricing power, and expanding free cash flow generation. And after a 28% decline, the stock’s valuation looks far more attractive relative to its long-term growth potential. All these factors make NFLX stock a “Buy.”

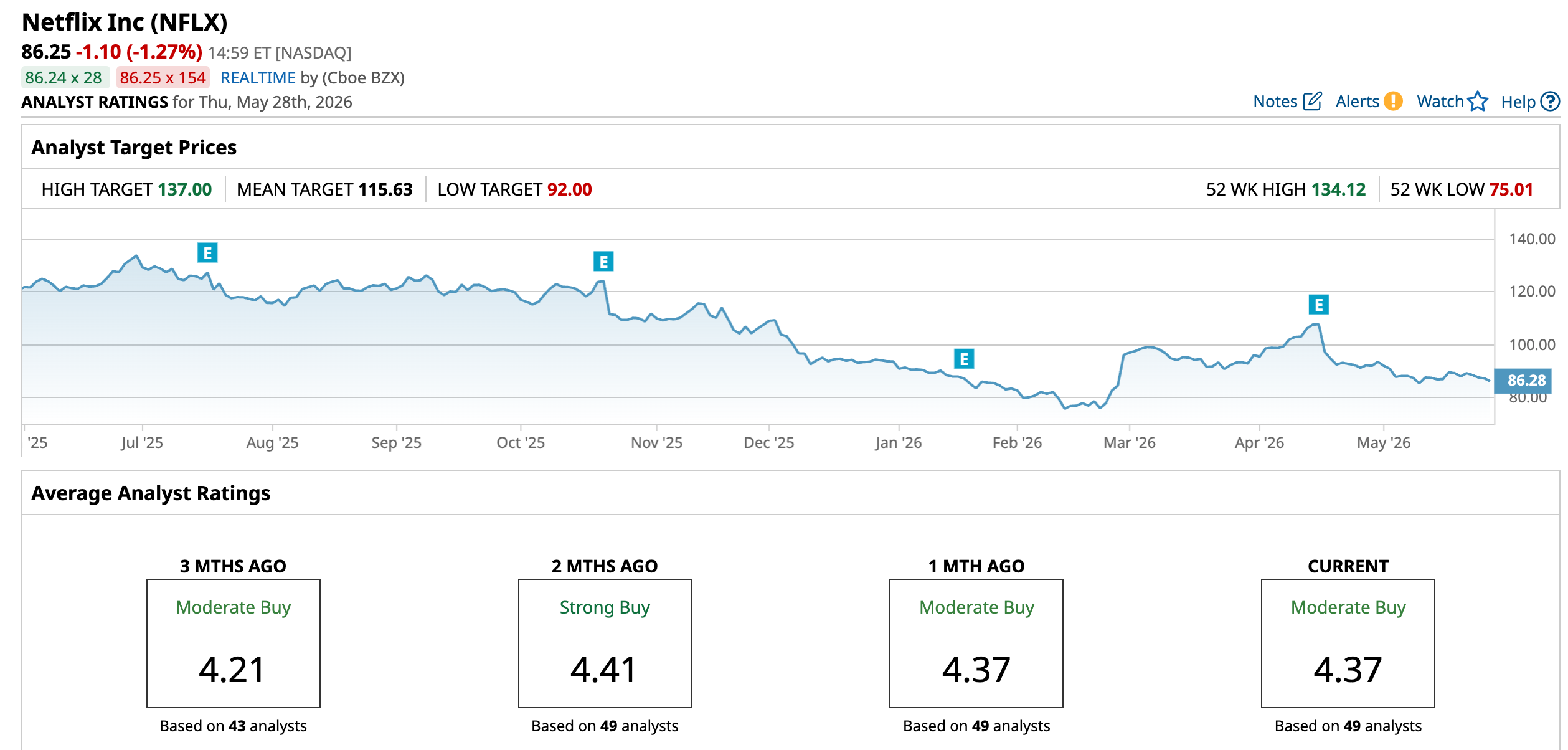

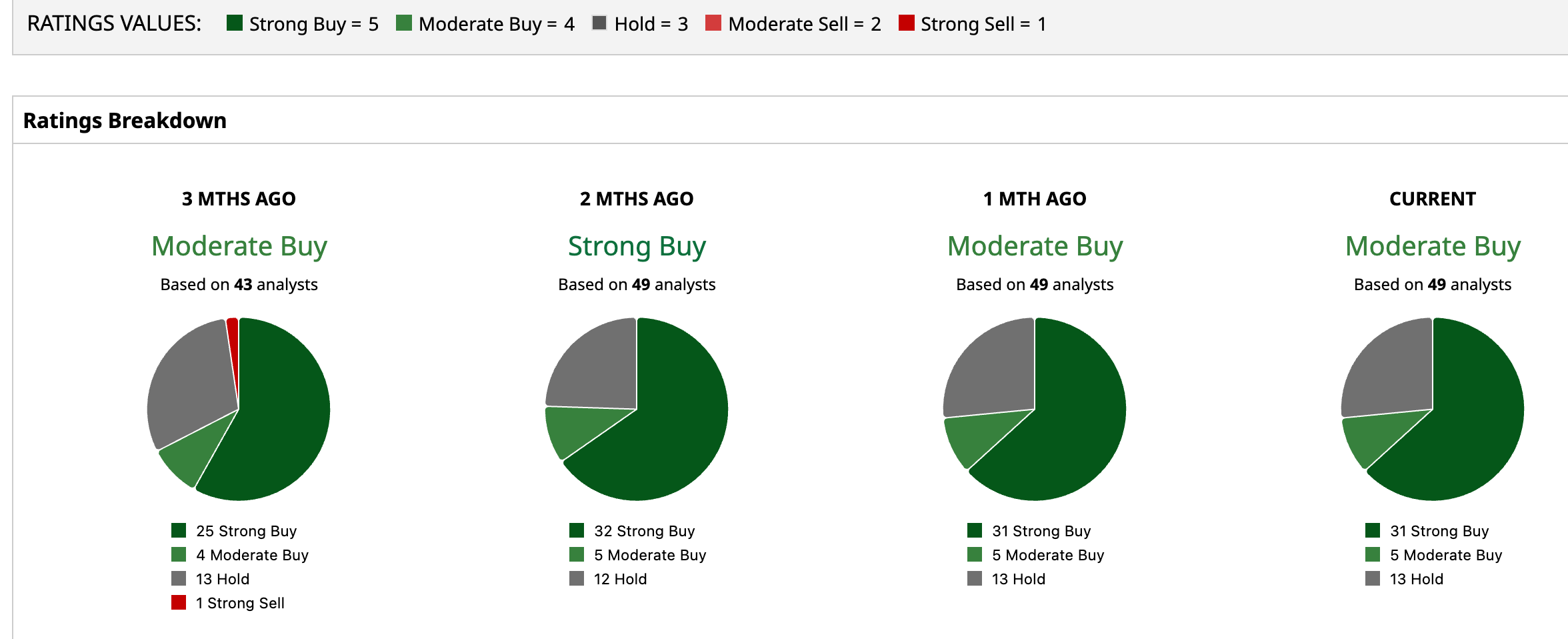

Meanwhile, Wall Street analysts still maintain a “Moderate Buy” consensus rating on the stock.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Down 28%, Netflix Stock Is Suddenly a Bargain IBM Missed the Bus on AI. New Federal Funding Means IBM Stock Could Be a Winner in Quantum Computing. A Giant Short Squeeze Could Be Brewing in Wolfspeed Stock You’ve Likely Never Heard of This Stock, But Data Center Demand Just Took Shares to New 52-Week Highs