SoundHound AI SOUN is making a significant strategic push toward proprietary artificial intelligence models as it seeks to strengthen its competitive position in the rapidly evolving conversational and agentic AI market. The company believes owning the full AI stack can improve performance, lower costs and create a sustainable competitive advantage.

The clearest example of this strategy is OASYS, SoundHound’s newly launched self-learning agentic AI platform. Management describes OASYS as a system where AI can automatically create, orchestrate, evaluate and improve AI agents, reducing deployment times from months to minutes. The platform is designed to operate across voice, text, web, kiosks, vehicles and other channels, creating a unified AI ecosystem for enterprise customers.

A key reason behind this push is cost efficiency. During the first quarter of 2026 earnings call, SoundHound highlighted that OASYS will increasingly rely on Polaris, its proprietary speech foundation model, along with internally developed specialized large language models and speech synthesis technologies. Management stated that most customer interactions could eventually be powered by SoundHound’s own models rather than expensive third-party frontier models, generating meaningful long-term cost savings.

The company also believes proprietary models can deliver better performance for targeted enterprise use cases. Rather than building general-purpose AI systems, SoundHound is developing specialized models focused on customer service, order processing, financial transactions and workflow automation. According to management, these models can outperform larger frontier models in specific applications while operating at lower costs.

The planned acquisition of LivePerson further strengthens this strategy. By combining SoundHound’s voice AI with LivePerson’s digital messaging platform, the company expects to gain access to tens of billions of annual customer interactions, creating a powerful proprietary data foundation that can improve model training and automation outcomes.

With first-quarter 2026 revenue rising 52% year over year to $44.2 million and demand growing across multiple industries, SoundHound is betting that proprietary AI models will help drive faster innovation, higher margins and stronger long-term growth.

What Sets SoundHound Apart in Enterprise AI

Two notable competitors in the enterprise conversational AI space are NICE Ltd. NICE and Five9, Inc. FIVN. Both NICE and Five9 have invested heavily in AI-powered customer engagement platforms, but their strategies differ from SoundHound’s growing focus on proprietary AI models.

NICE primarily integrates advanced AI capabilities into its customer experience platform to automate service workflows and improve contact center efficiency. While NICE benefits from a large enterprise customer base and deep industry expertise, it often relies on a broader ecosystem of AI technologies. NICE continues to expand its AI offerings, but its approach is more platform-centric than model-centric.

Five9 has also emerged as a major force in cloud contact center automation. Five9 leverages AI to enhance agent productivity and customer interactions across voice and digital channels. However, Five9’s strategy centers on orchestration and workflow automation rather than building a fully proprietary AI stack.

This is where SoundHound seeks differentiation. By developing its own speech foundation model, specialized AI models and the OASYS platform, SoundHound aims to reduce dependence on third-party AI providers. As enterprises increasingly prioritize cost efficiency, customization and data control, SoundHound believes its vertically integrated AI approach could provide an edge over both NICE and Five9.

SOUN’s Price Performance, Valuation & Estimates

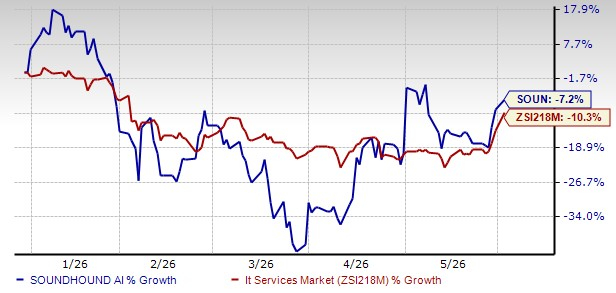

SoundHound shares have lost 7.2% year to date (YTD), outperforming the industry, as shown below:

SOUN’s YTD Price Performance

Image Source: Zacks Investment Research

From a valuation standpoint, SOUN trades at a forward price-to-sales (P/S) multiple of 16, above the industry’s average of 13.48.

SOUN’s P/S Ratio (Forward 12-Month) vs. Industry

Image Source: Zacks Investment Research

Over the past 30 days, the Zacks Consensus Estimate for SoundHound’s 2026 loss per share has widened to 18 cents, as shown below. The expected loss also remains wider than the previous year’s loss of 13 cents.

EPS Trend of SOUN Stock

Image Source: Zacks Investment Research

SOUN’s Zacks Rank

SOUN currently has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Nice (NICE): Free Stock Analysis Report

Five9, Inc. (FIVN): Free Stock Analysis Report

SoundHound AI, Inc. (SOUN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).