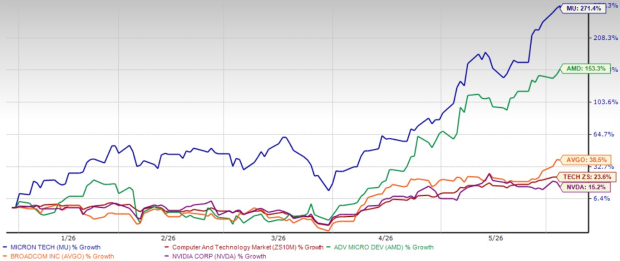

Micron Technology, Inc. MU has been one of the biggest winners in the semiconductor space this year. The memory chip giant has benefited from the explosive growth of artificial intelligence (AI) and high-performance computing (HPC), which are driving unprecedented demand for advanced memory solutions. Shares of Micron Technology have surged 271.4% year to date, significantly outperforming the broader Zacks Computer and Technology sector's gain of 23.6%.

The stock has also delivered stronger returns than several leading semiconductor names, including Advanced Micro Devices, Inc. AMD, Broadcom Inc. AVGO and NVIDIA Corporation NVDA. YTD, shares of Advanced Micro Devices, Broadcom and NVIDIA have soared 153.3%, 38.5% and 15.2%, respectively.

While such a massive rally may make some investors question whether the stock has run too far, Micron Technology's strong fundamentals suggest there could still be room for upside. The company remains one of the clearest beneficiaries of the AI infrastructure boom, and demand trends continue to work heavily in its favor.

Micron Technology YTD Price Return Performance

Image Source: Zacks Investment Research

Micron Technology’s Solid Financial Health

Despite ongoing macroeconomic challenges, geopolitical issues, and trade and tariff wars, MU’s financials remain rock solid. In the second quarter of fiscal 2026, revenues soared 196% year over year to $23.86 billion. Non-GAAP earnings per share jumped 682% to $12.20. Both figures comfortably exceeded analysts’ expectations, highlighting the strength of demand across Micron Technology’s key markets.

Profitability improved dramatically as well. Non-GAAP gross margin expanded to 74.9% from 37.9% a year ago, while non-GAAP operating income climbed to $16.46 billion from $2.01 billion. Non-GAAP operating margin reached an impressive 69% from 24.9% in the year-ago quarter, reflecting Micron Technology’s ability to convert booming AI-driven demand into substantial profits.

Micron Technology, Inc. Price, Consensus and EPS Surprise

Micron Technology, Inc. price-consensus-eps-surprise-chart | Micron Technology, Inc. Quote

Analysts continue to expect strong growth. The Zacks Consensus Estimate for fiscal 2026 revenues and EPS calls for year-over-year growth of 197.7% and 619.8%, respectively. The consensus mark for fiscal 2027 revenues and EPS indicates a year-over-year increase of 63.3% and 72.8%, respectively.

Cash generation remains another major strength. During the first half of fiscal 2026, Micron Technology generated $20.31 billion in operating cash flow and $10.81 billion in free cash flow. The company ended the quarter with $16.7 billion in cash and short-term investments, up from $12.02 billion in the previous quarter.

This financial flexibility gives Micron Technology multiple growth options. The company can continue investing aggressively in research and development, expand manufacturing capacity and reward shareholders at the same time. During the first half of fiscal 2026, the memory chip maker repurchased $650 million worth of stock and paid $266 million in dividends, demonstrating confidence in its long-term outlook.

New Tech Trends to Drive MU’s Prospects

Micron Technology sits at the center of several powerful technology trends that are likely to support growth for years. The company has meaningful exposure to AI, cloud data centers, industrial IoT and autonomous vehicles, all of which require increasingly advanced memory solutions. As AI adoption accelerates, demand for DRAM and NAND products continues to rise. MU has invested heavily in next-generation memory technologies, positioning itself to meet the growing performance and efficiency requirements of AI systems.

The company has also become more diversified. Rather than relying heavily on the historically volatile consumer electronics market, Micron Technology has increased its focus on enterprise, cloud and automotive customers. This shift should help reduce earnings volatility over time and make the business more resilient during industry downturns.

A particularly important growth driver is high-bandwidth memory (HBM), which has become essential for advanced AI workloads. Micron Technology’s HBM3E and HBM4 products are seeing exceptionally strong demand because they offer the speed and efficiency required by modern AI systems.

The strength of this demand is evident in Micron Technology’s order book. The company has already sold out its HBM3E and HBM4 supply for the calendar year 2026, while a significant portion of 2027 production is already committed through long-term customer agreements.

Micron Technology’s position in the AI ecosystem continues to strengthen. NVIDIA identified Micron Technology as a key HBM supplier for its GeForce RTX 50 Blackwell GPUs, reinforcing the company’s importance within the AI supply chain. Demand for HBM4 is also benefiting from next-generation AI infrastructure deployments, including NVIDIA’s Vera Rubin platform. Meanwhile, Micron Technology’s ongoing expansion of its advanced HBM packaging facility in Singapore should help support future growth.

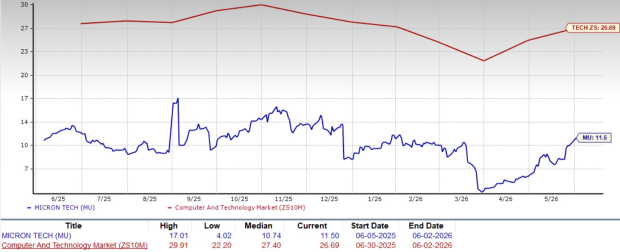

Low Valuation Makes MU an Attractive Bet

Despite a robust rally, MU stock still looks reasonably priced. It trades at a forward 12-month price-to-earnings (P/E) multiple of 11.50, which is significantly lower than the sector average of 26.69. This discount adds to the appeal for long-term investors.

Micron Technology Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

Compared with other major semiconductor players, Micron Technology has a lower P/E multiple than Advanced Micro Devices, Broadcom and NVIDIA. At present, Advanced Micro Devices, Broadcom and NVIDIA trade at P/E multiples of 57.24, 31.56 and 23.75, respectively.

Given its exposure to AI growth, Micron Technology’s relative valuation strengthens the case for buying the stock.

Conclusion: Buy Micron Technology Stock for Now

Micron Technology has delivered extraordinary stock performance, but the rally appears to be backed by equally strong business fundamentals. The company is benefiting from powerful AI-driven demand, generating record profits and cash flows, expanding its leadership in high-bandwidth memory and securing long-term customer commitments.

At the same time, the stock continues to trade at a valuation that is significantly lower than that of many of its semiconductor peers. With earnings expected to grow rapidly over the next two fiscal years and AI-related demand showing no signs of slowing, Micron Technology remains well-positioned for further growth.

Micron Technology sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Advanced Micro Devices, Inc. (AMD): Free Stock Analysis Report

Micron Technology, Inc. (MU): Free Stock Analysis Report

NVIDIA Corporation (NVDA): Free Stock Analysis Report

Broadcom Inc. (AVGO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).