The biggest winner in the stock market this year isn’t Nvidia (NVDA) or one of the Magnificent Seven stocks. And I’ll bet it won’t be SpaceX, Anthropic, or OpenAI, although those upcoming IPOs will get a lot of attention this year.

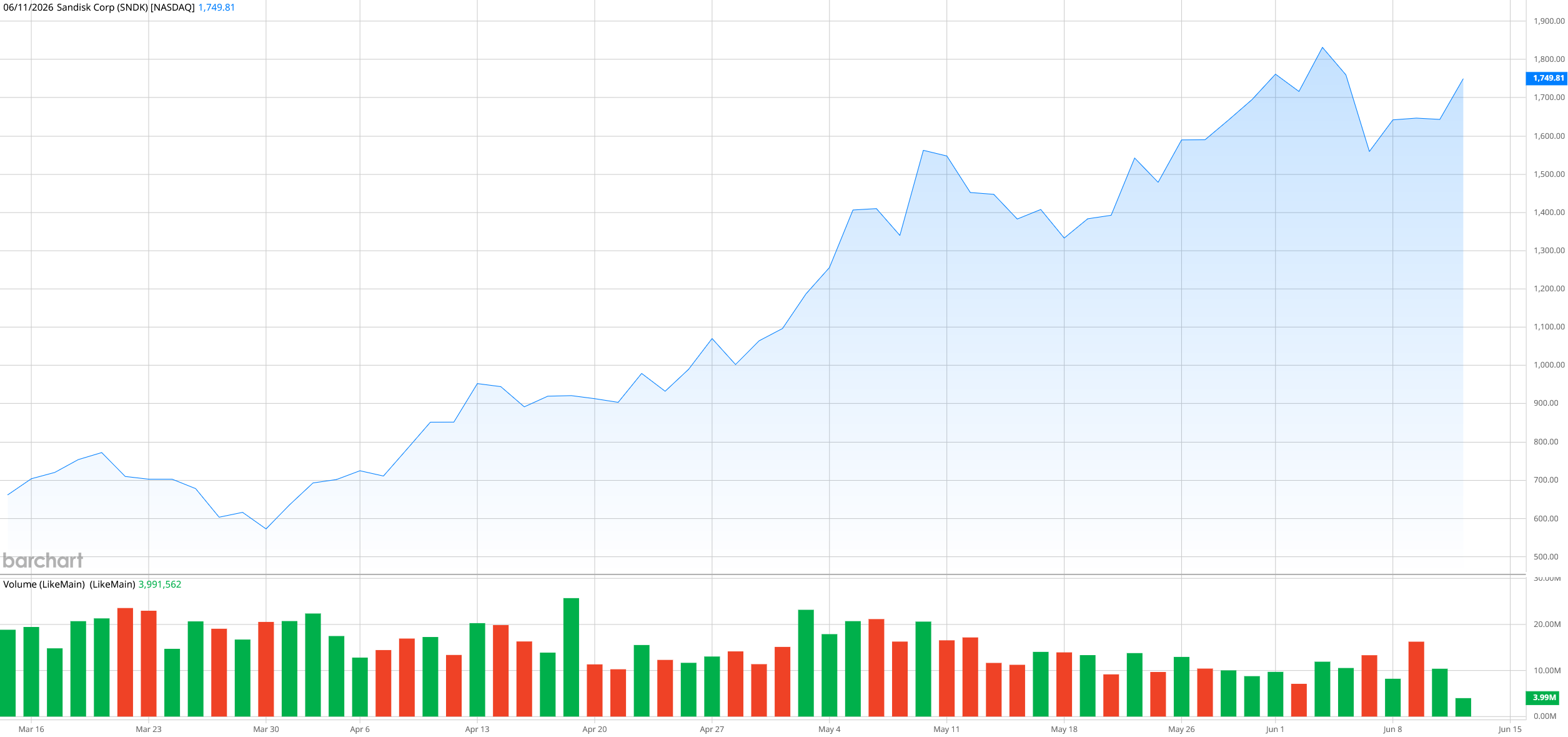

Instead, the biggest winner so far this year is SanDisk (SNDK), an AI infrastructure company on an outstanding two-year run. SNDK stock jumped nearly 560% in 2025 after the company completed its spinoff from Western Digital (WDC) in February. And so far this year, it's up another 650%.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Let me put it this way. Had you invested $10,000 in SNDK stock the day its split was complete just 16 months ago, you’d be sitting on $344,800 today. That’s an incredible return.

www.barchart.com

www.barchart.com But amazingly, the run doesn’t appear to be coming to an end. SanDisk just got a bullish update from the financial institution Mizuho, which reiterated its “Outperform” rating on SNDK stock and raised its price target from $1,825 to $2,200.

“We continue to see AI as the driving force behind the supply-demand imbalance in the memory market, as we note increasing demand in (2027-2028) could add further pressure to the market,” analysts wrote.

Let’s take a closer look at SanDisk, which appears destined to be the best-performing stock in the S&P 500 this year.

About SanDisk Stock

SanDisk, which is headquartered in Milpitas, California, makes products for flash and advanced memory computer storage. The company was acquired by Western Digital in 2016, but in 2023, the companies announced that SanDisk would be spun back off. The newly emerged company includes SanDisk's and Western Digital's flash products with an emphasis on solid-state drives (SSDs), memory cards, and USB drives.

SanDisk’s storage technology can be used in phones, laptops, cameras, and game systems. The company’s biggest revenue stream is its edge computing division, which supplies storage for cars, drones, security cameras, and other smart devices that create data. But the greatest growth opportunity comes from its data center division, and that’s what’s drawing the most investor interest right now. Shares in the last 12 months are up over 4,300%, and it is by far the best-performing stock in the S&P 500 ($SPX) this year.

| S&P 500 Stocks | Year-to-Date Return |

| SanDisk | 650% |

| Micron Technology (MU) | 225% |

| Dell Technologies (DELL) | 203% |

| Seagate Technology (STX) | 207% |

| Intel (INTC) | 223% |

Despite that run, SNDK isn’t tremendously expensive. Its forward price-to-earnings ratio is 26.3—high for the company, but fellow storage stocks Seagate and Western Digital have forward P/Es greater than 50. And the forward P/E of the S&P 500 is 22, meaning you are paying only a small premium for SNDK stock compared to the greater index.

SanDisk Beats on Earnings

Nothing would put a damper on a stock’s momentum like an earnings miss. But fortunately for investors, SanDisk has been a consistent winner when it steps to the earnings podium.

Revenue for the fiscal third quarter of 2026 (ending April 3, 2026) was $5.95 billion, up 251% from a year ago. The company posted net income of $3.61 billion, an increase of 287% from last year, and earnings of $23.41 per share versus expectations of $14.66 per share.

The quarter saw explosive growth in SanDisk’s data center division, which grew its revenue by 233% on a sequential basis and 645% from a year ago.

| Revenue | Q3 2026 | Q2 2026 | Q/Q Growth | Q3 2025 | Y/Y Growth |

| Data Center | $1.467 billion | $440 million | 233% | $197 million | 645% |

| Edge | $3.663 billion | $1.678 billion | 118% | $927 million | 295% |

| Consumer | $820 million | $907 million | (10%) | $571 million | 44% |

| Total Revenue | $5.950 billion | $3.025 billion | 97% | $1.695 billion | 251% |

“This quarter marks a fundamental inflection point for SanDisk—where our technology leadership is enabling a deliberate shift in our mix toward the highest-value end markets, led by data center,” CEO David Goeckeler said. “We are also advancing to a new business model built on multi-year customer engagements backed by firm financial commitments. Together, this transformation is driving structurally higher and more durable earnings power.”

SanDisk issued fourth-quarter guidance calling for revenue in the range of $7.75 billion and $8.25 billion, with gross margins between 79% and 81%. The company is projecting earnings per share of $30 to $33.

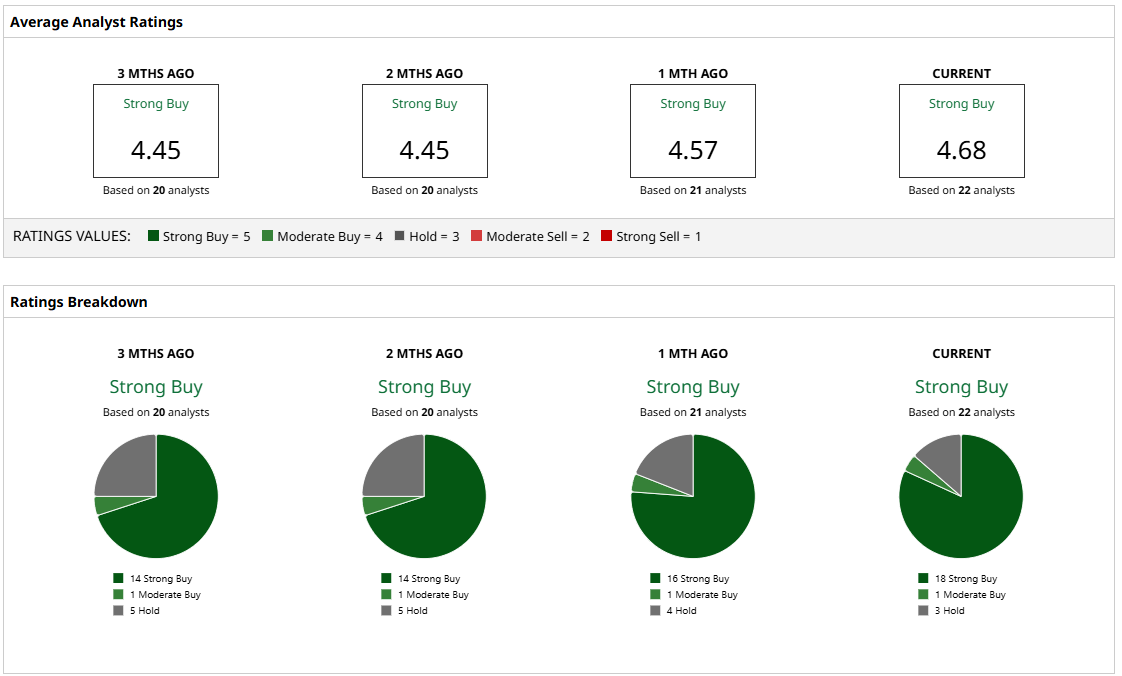

What Do Analysts Expect for SNDK Stock?

Simply put, analysts are expecting more of the same from SanDisk. Of 22 analysts who cover the stock, 19 of them have “Buy” ratings and the other three recommend holding. The consensus price target of $1,863.06 is lower than Mizuho’s bullish outlook but still represents potential upside of 8%. If you go by the Mizuho target of $2,200, then you’re looking at a potential upside of 28%. And the most bullish target of $3,250 implies dramatic gains of 89%.

At this point, SanDisk has risen so quickly—and has so much projected staying power—that it’s an ideal candidate for a stock split soon to make shares more accessible to retail investors. But in the meantime, don’t hesitate to use fractional shares to scoop up shares of SanDisk stock now.

www.barchart.com

www.barchart.com On the date of publication, Patrick Sanders had a position in: NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FuelCell Energy Missed on Q2 Revenue. Investors Are Betting That AI Data Centers Will Save the Day. This AI Infrastructure Stock Is Up 650% This Year. Wall Street Still Sees More Upside. Cathie Wood Is Buying the Dip in Broadcom Stock Micron Got a Major Vote of Confidence From Nvidia’s Jensen Huang on AI Returns. I Still Wouldn’t Chase MU Stock Here.