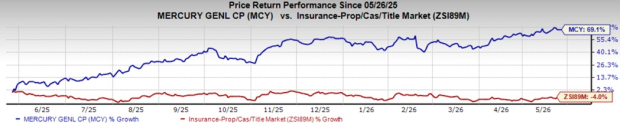

Mercury General Corporation MCY shares have risen 69.1% in the past year against the industry’s decline of 3.6%. Shares of MCY have outperformed the Finance sector and the Zacks S&P 500 composite’s growth of 13.3% and 33.1%, respectively.

Image Source: Zacks Investment Research

Mercury General has outperformed its peers, including Axis Capital Holdings Limited AXS, The Travelers Companies, Inc. TRV and Cincinnati Financial Corporation CINF. Shares of AXS have lost 0.7 while TRV and CINF have gained 13.1% and 15.3%, respectively, in the past year.

MCY’s Expensive Valuation

MCY’s shares are trading at a premium compared with the industry. Its forward price-to-book value of 2.16X is higher than the industry average of 1.39X, the Finance sector’s 4.34X, and the Zacks S&P 500 composite’s 8.12X.

Image Source: Zacks Investment Research

MCY’s Growth Projection Encourages

The Zacks Consensus Estimate for Mercury General’s 2026 earnings per share (EPS) indicates a year-over-year increase of 48.7%. The consensus estimate for revenues is pegged at $6.24 billion, implying a year-over-year improvement of 8.5%.

The consensus estimate for 2027 revenues and EPS indicates an increase of 5.7% and 2.1%, respectively, from the corresponding 2026 estimates.

Earnings have grown 16.4% in the past five years. MCY has an impressive Growth Score of A. This style score helps analyze the growth prospects of a company.

Optimistic Analyst Sentiment on MCY

The Zacks Consensus Estimate for 2026 and 2027 has moved 30.5% and 50% north, respectively, in the last 30 days, reflecting analysts’ optimism.

MCY’s Favorable Return on Capital

Return on equity for the trailing 12 months was 32.9%, which compared favorably with the industry’s 7.4%. This reflects its efficiency in utilizing shareholders’ funds.

Return on invested capital in the trailing 12 months was 22.7%, better than the industry average of 5.7%, reflecting MCY’s efficiency in utilizing funds to generate income.

Key Points to Note for MCY

Mercury General has been gaining ground by relying on a set of core organic strengths. Premiums have trended steadily higher, supported by rate increases across insurance lines and a growing policy base. The Property and Casualty segment has also held up well, signalling a stable backdrop for the company’s operations. These organic drivers are lifting Mercury General’s top line and shaping the path for continued expansion.

Over the past five years, the top line has witnessed a compound annual growth rate of 7.6%, supported by higher net premiums earned and other revenues. California remains a key driver, with higher rates in the homeowner’s line and a growing number of auto policies strengthening the company’s premium base.

Net investment income has also played a key role in Mercury General’s growth. Over the past five years, it has witnessed a compound annual growth rate of 15.7%, supported by higher average yields and a larger base of invested assets. Management highlighted continued investments in private credit and venture funds and expects liquidation and distributions from these private investment funds over the next 1-7 years. These could provide an ongoing contribution to future investment income and long-term returns.

Mercury General’s strong liquidity position further supports its growth. It had a solid cash balance of $1.3 billion as of March 31,2026. The company believes thatits cash flow from future operations is adequate to satisfy liquidity requirements. Investment maturities are also available to meet the company’s liquidity needs. The average annual net cash provided by operating activities in the past 10 years was approximately $468 million, and cash generated from operations was sufficient to meet the liquidity requirements during this period.

Conclusion

Solid performance across its Property and Casualty segment, rate increases, a rise in the number of policies written, higher average invested assets and cash, as well as financial flexibility, make Mercury General a strong contender for being in one’s portfolio. The Zacks average price target is $120 per share, suggesting a potential 17.3% upside from the last closing price.

Coupled with favorable estimates, solid growth projections, and higher return on capital, the time appears right for potential investors to bet on this Zacks Rank #1 (Strong Buy) insurer. You can see the complete list of today’s Zacks #1 Rank stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

The Travelers Companies, Inc. (TRV): Free Stock Analysis Report

Cincinnati Financial Corporation (CINF): Free Stock Analysis Report

Axis Capital Holdings Limited (AXS): Free Stock Analysis Report

Mercury General Corporation (MCY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).