Bitcoin has halved from its all-time high of $126,200 and now trades near $61,000. Total crypto market capitalization has contracted roughly 48% to about $2.46 trillion, Google searches for "Bitcoin to zero" are increasing, and the Fear and Greed index is showing "Extreme Fear". That last data point tells you where sentiment sits, and history suggests that moments of maximum fear are usually the wrong time to give up on the asset class.

In this piece, we'll look at why crypto crashed, how the current drawdown stacks up against previous bear markets, what miners, institutions, and capital flows are telling us, and what would need to happen for the market to find a bottom.

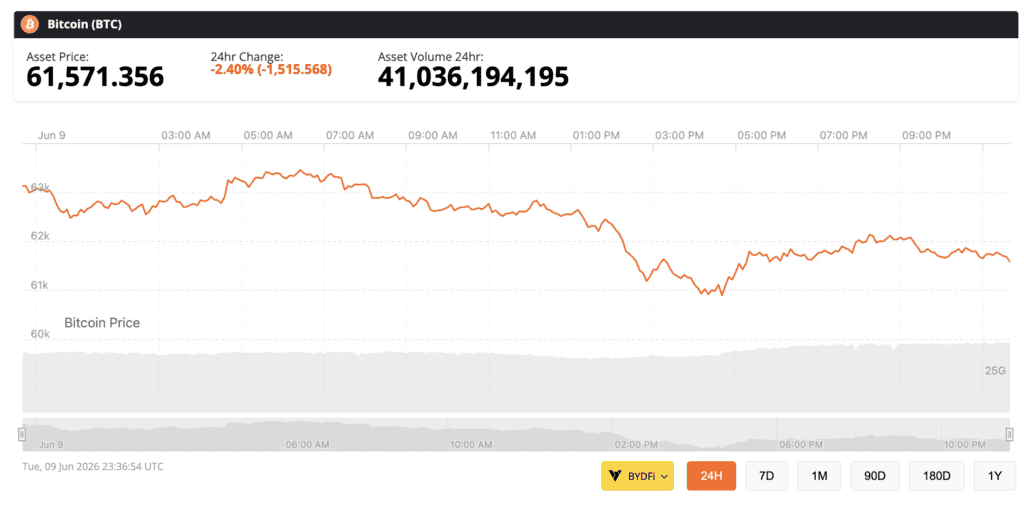

Bitcoin is down 2% overnight to $61,500, source: BNC

Why is crypto crashing in 2026?

The June 2026 selloff is macro-driven rather than crypto-native, and that distinction matters more than any other fact in this article.

Four forces converged at once. Sticky US inflation has pushed back expectations for Federal Reserve rate cuts, with BlackRock noting that the May CPI print will be an early test of how US-Iran tensions are feeding into already elevated prices. The same geopolitical risk hit equities and strengthened the dollar, which is always a headwind for Bitcoin's global bid. At the same time, US spot Bitcoin ETFs bled $4.4 billion across a record 13 consecutive sessions of outflows, institutional de-risking on a scale the ETF era had not yet seen. That streak has now ended, which the bulls will have noted. And finally, capital has rotated hard into AI. Bernstein analysts pointed out that Bitcoin inflows have slowed sharply in 2026 as investors chase AI exposure instead, with the Nasdaq up roughly 41% over the past year while Bitcoin fell 37%.

Leverage made everything worse. When Bitcoin broke below $64,000 in early June, more than $1.1 billion in leveraged positions were liquidated within 24 hours, and the subsequent break of $62,000 wiped out another $1.5 billion. The intraday low printed near $59,100, Bitcoin's weakest level since late 2024, before the market bounced back into the low $60,000s, where it sits at the time of writing.

Strategy (MSTR) added a serious jolt on top of all that. The largest corporate holder of Bitcoin sold 32 BTC, its first disclosed sale since December 2022, raising roughly $2.5 million to fund dividends on its STRC preferred stock. In dollar terms the sale was trivial, about 0.004% of the company's 843,706 BTC treasury, and TD Cowen analyst Lance Vitanza said reports of Strategy becoming a meaningful seller were overblown. Michael Saylor framed the move around the preferred equity, posting that the goal is to make STRC "the best credit instrument in the world." None of that stopped the market treating the news like a five-alarm fire, which probably says more about sentiment than about Strategy's balance sheet. It is worth noting, though, that the company's average cost basis of $75,699 is now underwater.

How does this crash compare to 2018 and 2022?

This is the question that separates a tradable correction from a bear market, and it is where the current drawdown looks different from the two everyone keeps comparing it to.

The 2018 bust erased 84% of Bitcoin's value and followed a pure retail speculative blow-off, an ICO mania built on very little. The 2022 collapse cut 78% and was triggered by fraud, with the Terra-Luna death spiral and the implosion of FTX destroying counterparty trust across the entire industry. Both of those bottoms took years to repair because the damage was internal. The system itself had failed, and confidence had to be rebuilt from scratch.

The 2026 correction is roughly 50% deep and the cause is external. No major exchange has collapsed, no stablecoin has depegged, and no flagship protocol has been exposed as fraudulent. DeFi infrastructure is functioning normally, network activity on Ethereum and Solana remains healthy despite falling token prices, and the regulatory direction of travel is constructive rather than hostile. The CLARITY Act continues to progress in the US, the UK's Financial Conduct Authority is moving to allow mutual funds 10% exposure to crypto ETNs, and Nasdaq has won SEC approval to trade tokenized securities.

History suggests a macro-driven drawdown with intact infrastructure resolves faster than a trust-driven one, because the recovery depends on a macro catalyst rather than a multi-year rebuild of confidence. The clearest such catalyst sits on this week's calendar. The mid-June FOMC meeting looms over everything, and while markets expect no cut (the Fed held at 3.50% to 3.75% in March, citing Middle East tensions), any dovish signal would remove the exact pressure that caused the crash in the first place.

What is the 200-week moving average telling us?

Bitcoin has fallen back to its 200-week moving average, currently around $61,800, for the first time this cycle. This is the line that has marked every major cycle bottom in Bitcoin's history. As Brave New Coin covered in detail last week, the 2015, 2018, and 2020 macro bottoms all formed on or just below this trendline, and over more than a decade Bitcoin has spent very little time trading beneath it. Veteran chartist Dave the Wave flagged the touch with a four-word caption, "#btc back to the 200 WMA", and didn't need to say anything else.

The timing rhyme is hard to ignore. Analyst Rekt Capital noted that Bitcoin tagged its 200-week average in June 2022 and has now done so again in June 2026, almost exactly four years on. There is an asterisk, of course. 2022 is also the one cycle where the line actually broke, and price spent months underneath it before recovering. The 200-week average is a zone where bottoms tend to form, not a guarantee that one has.

EMA Crossover played out, preceding -39% downside, wrote Rekt Capital On X

On-chain flows are giving a mixed read. CryptoQuant data shows large whales, wallets holding between 1,000 and 10,000 BTC, have been net sellers and have distributed roughly 188,000 BTC. On the other side of the ledger, Coinbase institutional strategist John D'Agostino says institutions have been buying near $65,000, with ETF ownership and corporate demand holding firm underneath the headline outflows.

https://www.youtube.com/watch?v=QnUArpkG_Mg

What does Bitcoin miner capitulation signal?

If you want a cycle-bottom indicator with a genuine track record, watch the miners, because right now they are in full capitulation.

Publicly traded Bitcoin miners sold more BTC in Q1 2026 than in all of 2025, surpassing the 20,000 BTC quarterly record set during the Terra-Luna collapse in Q2 2022, according to TheMinerMag. Hashprice, the standard measure of daily mining revenue per petahash, has been pinned near record lows around $31 to $33 per PH/s per day according to Hashrate Index data. That is below the roughly $35 breakeven for operators running older rigs, which leaves around 20% of the industry mining at a loss. CoinShares' Q1 mining report documented the exodus in detail. Core Scientific sold roughly 1,900 BTC in January alone, Bitdeer cut its treasury to zero, Riot sold 1,818 BTC in December, and CoinShares expects further capitulation among higher-cost operators through the first half of 2026 unless price recovers materially.

There is a structural twist this cycle in the form of an AI escape hatch. Miners have signed GPU co-location and cloud deals with hyperscalers worth more than $70 billion in aggregate, and repurposed infrastructure can earn five to ten times more revenue per megawatt than mining Bitcoin. Hashrate that leaves for AI probably never comes back, which is painful now but quietly bullish for the survivors, who will face slower difficulty growth and better margins at any given Bitcoin price. JPMorgan's read is that the exit of higher-cost miners has largely stabilized, and the bank remains positive on crypto for 2026.

The reason any of this matters for price is that miner capitulation has historically clustered at cycle bottoms. The hash ribbons indicator, which tracks miner shutdowns through hashrate moving-average crossovers, has marked some of the best buying opportunities in Bitcoin's history. Forced sellers exhausting themselves is, perversely, how floors get built.

Where is the money actually going?

Capital is not so much leaving crypto as rotating within it, and the destinations give you a decent preview of what the next cycle's leadership might look like.

Hyperliquid is the standout. While Bitcoin halved, HYPE gained roughly 160% year-to-date and broke to a new all-time high above $73 in the middle of a market-wide drawdown. The rally has little to do with memes or narrative momentum. Hyperliquid now accounts for about a third of total network fee revenue across all blockchains, and its rise reflects a shift in how the market values crypto assets, with verifiable cash flows, fee generation, and buybacks now counting for more than a good story. The contrast with Cardano, which has cratered to six-year lows below $0.23, shows just how ruthlessly this bear market is sorting assets with revenue from assets with only a narrative.

Tokenized real-world assets are the quiet bull market running underneath all of this. The RWA sector has grown 589% since early 2025, with tokenized stocks the fastest-growing segment. Securitize CEO Carlos Domingo argued at ETHConf that bringing stocks and ETFs onchain could unlock a market far larger than today's roughly $30 billion sector, putting the eventual figure at $5 trillion. The venture money agrees with him. Paradigm, a16z crypto, and Ribbit just led a $175 million round into the lending protocol Morpho to build out onchain credit market infrastructure. None of this activity looks like an industry in terminal decline.

What would signal the bottom is in?

Nobody rings a bell at the bottom, but the checklist for this particular cycle is unusually clear.

The first item is a dovish Fed. Because this crash is macro-driven, a macro pivot is the most direct cure, and the mid-June FOMC meeting is the single most important event on the calendar.

The second is sustained ETF inflows. The record 13-day outflow streak has ended, and what matters now is whether flows turn durably positive, which would tell us institutions are re-risking rather than simply pausing their selling.

The third is miner capitulation running its course. Hash ribbons turning, difficulty adjusting downward, and treasury sales slowing would echo the pattern that marked the 2018, 2020, and 2022 lows.

The last is the 200-week moving average holding. A weekly close meaningfully below the $61,800 area that sticks would open up the 2022 scenario, meaning months below the line and a potential deeper flush toward the $50,000 to $55,000 zone that bearish projections are targeting. If the level holds, the pattern of every previous cycle bottom forming here stays intact.

Analyst Dave the Wave suggests a local bottom is in, writing that $69,000 is now a shot term target for Bitcoin.

#btc shorter-term target of $69,000, wrote Dave the Wave on X

So, will crypto recover?

The honest answer is that nobody knows the timing, and anyone offering certainty is selling something. The structure of this drawdown matters, though. A 50% decline feels like the death of a cycle, but by Bitcoin's historical standards it is closer to the middle of an ordinary one. The previous two bear markets were deeper, took longer to heal, and were caused by the industry's own failures. This one was imported from the macro world, and the industry's plumbing, from exchanges and stablecoins to DeFi protocols and institutional rails, has held up throughout.

Meanwhile the parts of crypto that generate real revenue are setting all-time highs, tokenized assets are compounding at triple-digit rates, and the forced sellers, whether overleveraged longs, underwater miners, or skittish ETF allocators, are gradually exhausting themselves at the same long-term trendline where every previous cycle found its floor.

Peak fear has historically been a better contrarian buy signal than peak euphoria has been a sell signal. The bull market that began in 2023 is over. Whether June 2026 ends up being remembered as the start of a crypto winter or the bottom of cycle five will probably be decided by the Federal Reserve before it is decided by anyone in crypto.