Whirlpool Corporation’s WHR MDA North America segment delivered strong share gains in the fourth quarter of 2025, driven by successful new product launches. Margins were pressured by intense promotional activity, as industry pricing failed to keep pace with tariff-related cost increases. Consequently, the segment reported a modest EBIT margin of 2.8% in the fourth quarter, reflecting the ongoing challenge of balancing volume growth with profitability amid competitive pricing.

Whirlpool aims to offset global volatility through a North American recovery. The company highlighted that its MDA North America segment is well-positioned for continued organic growth and margin expansion, supported by strong structural drivers. A key factor is its robust lineup of new products. In 2025, more than 30% of the portfolio was transitioned to new offerings, which have received a strong response from both trade customers and consumers. These products have secured significantly more floor space at key retailers compared to their predecessors, contributing to share gains toward the end of the year. With additional innovation planned for 2026, the segment is set to build further on this momentum.

Whirlpool’s strong position as a domestic manufacturer in a tariff-driven environment is another driver of growth. The company produces more appliances domestically than its peers, which manufacture only about 25% of their U.S. sales locally. Its operations rely 96% on American steel and suppliers, supported by large-scale plants and ongoing investments. Tariffs are beginning to act as a tailwind, with reduced industry promotions in January indicating rising cost pressures on importers and improving competitive dynamics for domestic producers.

The company expects growth in MDA North America from new products, while continued strength in SDA Global and international segments is expected to drive 80-110 basis points of margin expansion to 5.5-5.8% by 2026. North America's strength and innovation provide momentum, positioning Whirlpool to offset global headwinds.

The Zacks Rundown for WHR

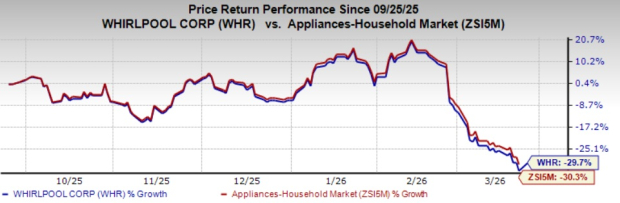

WHR’s shares have lost 29.7% in the past six-month period compared with the industry’s 30.3% decline. The company currently has a Zacks Rank #5 (Strong Sell).

Image Source: Zacks Investment Research

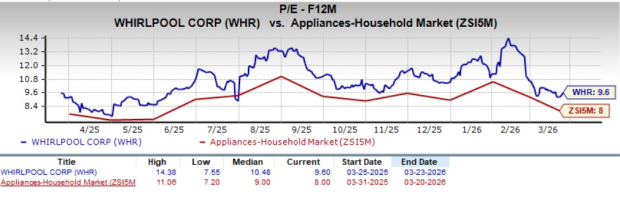

From a valuation standpoint, WHR trades at a forward price-to-earnings ratio of 9.60, higher than the industry’s average of 8.00.

Image Source: Zacks Investment Research

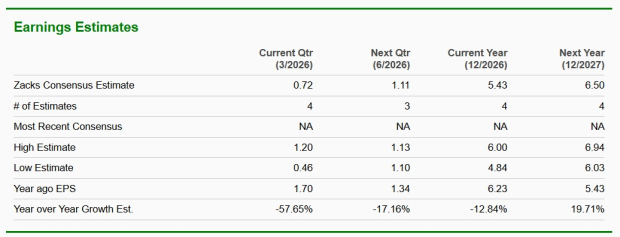

The Zacks Consensus Estimate for WHR’s current fiscal year earnings implies a year-over-year decline of 12.8%, while the estimate for the next fiscal year indicates 19.7% year-over-year growth.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

Columbia Sportswear Company COLM engages in the design, development, marketing and distribution of outdoor, active and lifestyle products in the United States, Latin America, the Asia Pacific, Europe, the Middle East, Africa and Canada. At present, COLM sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for COLM’s current fiscal-year sales implies growth of 2%, and the same for earnings indicates a decline of 6.2% from the year-ago figures. COLM delivered a trailing four-quarter earnings surprise of 25.2%, on average.

Wolverine World Wide, Inc. WWW designs, manufactures, sources, markets, licenses and distributes footwear, apparel and accessories. At present, WWW carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for WWW’s current fiscal-year sales and earnings indicates growth of 5.5% and 9%, respectively, from the year-ago figures. WWW delivered a trailing four-quarter earnings surprise of 31.8%, on average.

Crocs, Inc. CROX designs, develops, manufactures, markets, distributes and sells casual lifestyle footwear and accessories for men, women and kids. At present, CROX carries a Zacks Rank of 2.

The Zacks Consensus Estimate for CROX’s current fiscal-year sales and earnings implies growth of 0.4% and 7%, respectively, from the year-ago figures. CROX delivered a trailing four-quarter earnings surprise of 16.6%, on average.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

SeeWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Columbia Sportswear Company (COLM): Free Stock Analysis Report

Whirlpool Corporation (WHR): Free Stock Analysis Report

Wolverine World Wide, Inc. (WWW): Free Stock Analysis Report

Crocs, Inc. (CROX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).