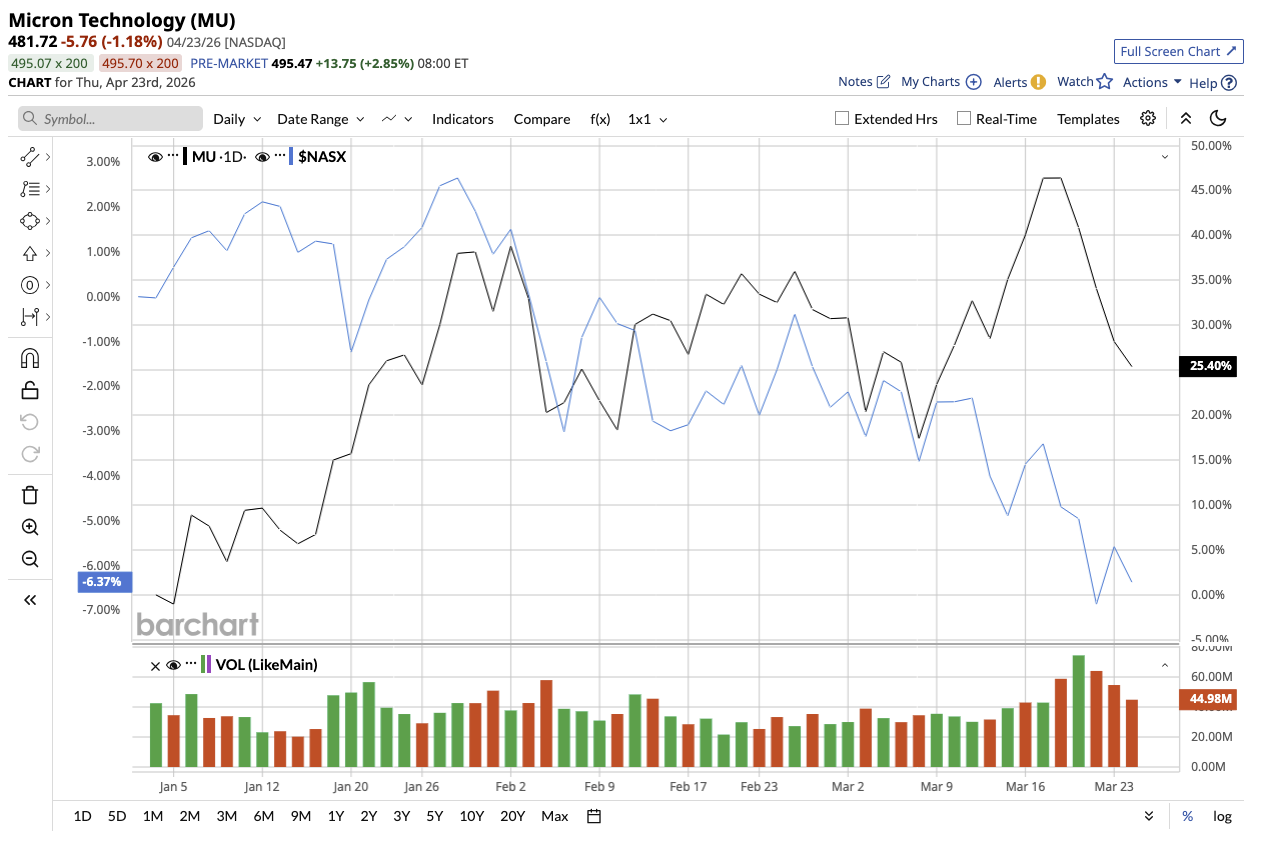

Micron Technology (MU) stock has been on a wild ride for the past year, rising by an eye-catching 560%. The scale of its AI-driven growth has made analysts rethink what the business is worth. While some investors believe the stock is done, Wall Street has an ambitious price target of $852 over the next year, almost double current levels. MU stock is up 85% year-to-date (YTD), outperforming the tech-heavy Nasdaq Composite's ($NASX) gain of almost 7%.

Should you grab Micron stock before it hits Wall Street's bold price target?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comPricing Power Is Driving Micron’s Story

Micron’s second quarter showed what a memory company can earn in an AI era. The company specializes in memory and storage chips, including DRAM, NAND, and high-bandwidth memory (HBM). In Q2 fiscal 2026, revenue surged 196% year-over-year (YOY) to $23.9 billion. EPS increased a staggering 682% YOY to $12.20. Currently, Micron’s growth is mainly driven by pricing power. AI systems need massive amounts of memory to handle data, but there is insufficient supply of DRAM and NAND to match the increasing demand. This imbalance has resulted in increased memory-chip pricing, which boosts Micron's revenue and profits.

At the moment, HBM is a game changer for Micron, which is partly why Wall Street is so optimistic. HBM is a more advanced, high-speed memory used in AI chips and GPUs. The company has already begun volume shipments of HBM4 products and is working closely with major AI hardware players. Its upcoming HBM4E generation is expected to improve performance and strengthen its competitive position.

Micron is spending aggressively to sustain its position in the memory. The firm expects to spend more than $25 billion in capital expenditures in fiscal 2026, with plans for higher spending in fiscal 2027. These investments include new fabs in the U.S., expansions in Japan, and a new NAND facility in Singapore. The company is also ramping advanced nodes, which are expected to dominate production by mid-2026. Additionally, Micron is planning to capitalize on emerging opportunities in AI, robotics, and edge computing. The memory industry is cyclical, so this kind of forward guidance is rare. This suggests that the current demand for Micron’s product is not only strong but also long-lasting.

For the third quarter, management expects this momentum to continue. Revenue is projected to rise more than threefold YOY to $33.5 billion, compared to $9.3 billion in the prior-year quarter. EPS is forecast at $19.15, plus or minus $0.40, compared to $1.91 in Q3 2025. Gross margin is projected to land at 81%, up from 75% in Q2.

Why Wall Street Predicts an $852 Bull Case

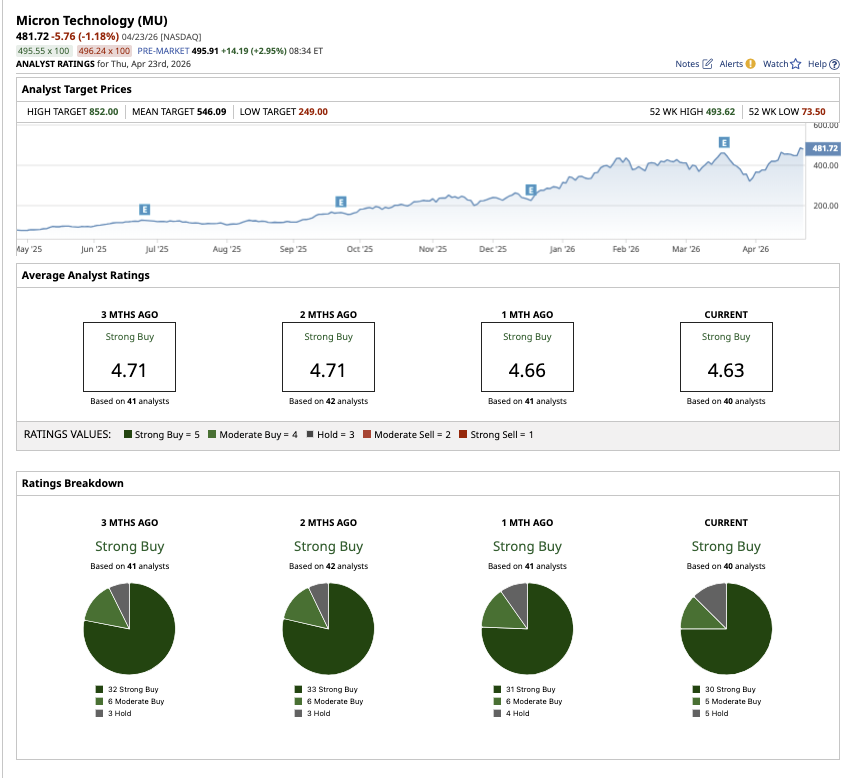

Following the stellar Q2 results, many analysts raised their price targets for MU stock. Overall, Wall Street has a mean target price of $546.09 for MU stock, which implies the stock could climb by 5% from current levels. The most bullish estimate stands at $852, suggesting potential upside of 63% over the next 12 months.

At first glance, the idea of Micron reaching $852 may sound aggressive, but it is not an impossible target given the company’s rapidly expanding earnings power. Analysts expect earnings to surge by 651% in fiscal 2026, followed by 69% growth in fiscal 2027. If the company can sustain high margins and elevated pricing, this level of earnings expansion could continue boosting stock performance. Furthermore, if the demand-supply imbalance improves, Micron’s profitability could remain elevated for a long time.

Despite this strong growth outlook, MU stock is trading cheap at just 8.3 times forward earnings. This discounted valuation likely reflects investors’ caution around the cyclical nature of the memory market, with concerns that this earnings surge was the peak and future oversupply could compress margins. That said, Wall Street remains strongly bullish about MU stock. Of the 40 analysts covering the stock, 30 rate it as a “Strong Buy,” five have a “Moderate Buy” rating, and five analysts offer a “Hold" rating.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Here's Why Wall Street Thinks Micron Stock Can Touch $852 The $100 Million Man: What the ‘Richest Ever’ Fed Chair Nominee Kevin Warsh, With Investments in Elon Musk’s SpaceX, Means for Your Portfolio The Biggest Catalyst for Tesla Stock in History Could Trigger in Just 3 Months The 3 Dividend Aristocrats Wall Street Calls a ‘Strong Buy’ With Up to 46% Upside