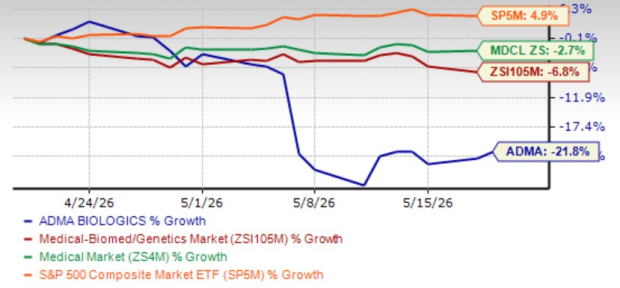

ADMA Biologics’ ADMA shares have crashed 21.8% over the past month compared with the industry’s decline of 6.8%.

The stock has also underperformed the sector and the S&P 500 Index in this time frame.

ADMA Underperforms Industry, Sector & S&P 500 Index

Image Source: Zacks Investment Research

Much of this decline came after the company reported first-quarter results on May 6. The company also lowered its annual guidance.

Against this backdrop, a closer examination of ADMA’s key strengths and potential challenges is warranted to better assess the stock’s investment appeal.

Why Did ADMA Cut Its 2026 Guidance?

ADMA Biologics markets plasma-derived biologics for the treatment of immune deficiencies and the prevention of certain infectious diseases.

The company’s top line currently comprises sales of three FDA-approved products — Bivigam (an Intravenous Immune Globulin [“IVIG”] product to treat primary humoral immunodeficiency), Asceniv (to treat primary immunodeficiency disease or PIDD) and Nabi-HB (to treat and provide enhanced immunity against the hepatitis B virus).

Management noted that increased competition, elevated channel inventories and aggressive pricing activity in standard immunoglobulin (IG) products created temporary pressure on top-line performance, particularly for Bivigam.

Total revenues in the first quarter were $114.5 million, down 0.3% from the year-ago quarter’s level. Bivigam revenues declined 54% year over year, which management attributed largely to the same distribution and inventory dynamics affecting the standard IG market.

Given rapidly evolving competitive dynamics in the plasma products and immunoglobulin market, ADMA updated its full-year expectations and withdrew previously issued long-term guidance. The company now expects 2026 revenues to be in the range of $530 million to $560 million (previous guidance: exceeding $635 million).

ADMA now expects 2026 adjusted net income of $170-$200 million (previous guidance: more than $255 million).

Management said the outlook assumes sustained pressure on standard IG pricing through the remainder of the year while maintaining confidence in Asceniv’s growth trajectory and relative insulation from broader standard IG volatility.

Can Asceniv Stabilize ADMA?

Asceniv, its lead product, is a plasma-derived IVIG that contains naturally occurring polyclonal antibodies.

Asceniv remained the key contributor to ADMA’s revenue performance, while the company’s other product lines trended in the opposite direction.

Asceniv recorded 28% year-over-year revenue growth, driven by record utilization, expanding prescriber adoption, strong patient adherence and continued new patient starts.

Management believes that underlying Asceniv demand remained strong, citing record utilization growth, record new patient starts, expanding prescriber breadth and steady patient adherence. ADMA also noted that April demand supported a second-quarter run rate consistent with first-quarter direct sales, giving early signs of normalization in ordering patterns.

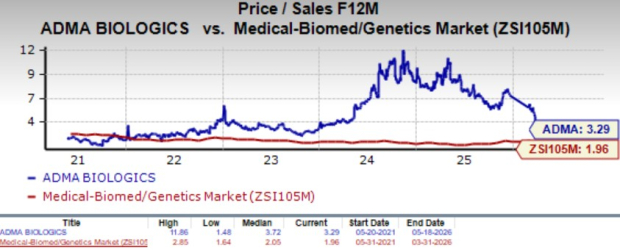

ADMA’s Valuation & Estimates

Going by the price/sales ratio, ADMA’s shares currently trade at 3.29x forward sales, lower than its mean of 3.72x but higher than the industry’s 2.05x.

Image Source: Zacks Investment Research

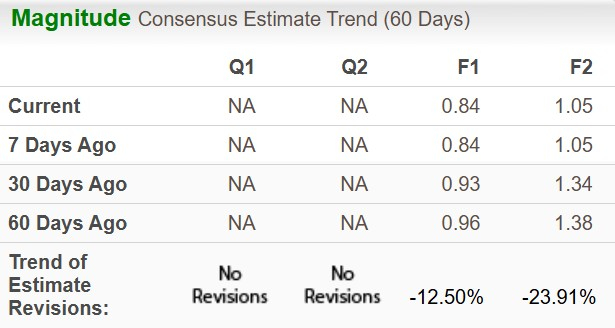

Estimate Movement

The Zacks Consensus Estimate for ADMA’s 2026 earnings per share has moved south to 84 cents from 94 in the past 30 days while that for 2027 EPS has declined to $1.05 from $1.34 in the same time frame.

Image Source: Zacks Investment Research

Avoid ADMA Stock for Now

ADMA Biologics, which competes with Takeda TAK and Grifols GRFS in the U.S. market for plasma-derived products, has remained under pressure since late March following a bearish report issued by Culper Research on March 24, 2026.

Investor sentiment toward the stock has weakened further after the company lowered its annual guidance, raising concerns about its ability to navigate ongoing challenges in the IG market amid intensifying competition and shifting market dynamics.

Although demand for Asceniv continues to be solid, broader pressure across the U.S. plasma-derived products space suggests a more cautious near-term outlook. Competitive intensity, pricing dynamics and market share concerns could continue to weigh on growth visibility and margin expansion prospects.

Given the combination of negative market sentiment, reduced guidance and declining earnings estimates, we believe ADMA stock currently offers an unfavorable risk-reward balance and advise investors to remain cautious until the company’s growth outlook and competitive position become clearer.

ADMA currently has a Zacks Rank #5 (Strong Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Grifols, S.A. (GRFS): Free Stock Analysis Report

ADMA Biologics Inc (ADMA): Free Stock Analysis Report

Takeda Pharmaceutical Co. (TAK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).