Huntington Ingalls Industries, Inc. (HII), headquartered in Newport News, Virginia, designs, builds, overhauls, and repairs military ships. Valued at $12.6 billion by market cap, the company offers non-nuclear and nuclear-powered vessels for the U.S. Navy and Coast Guard, and also provides after-market services for military ships worldwide.

Shares of this largest military shipbuilding company have outperformed the broader market over the past year. HII has gained 42.8% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 27.9%. However, in 2026, HII stock is down 5.7%, compared to the SPX’s 9.2% rise on a YTD basis.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Narrowing the focus, HII’s underperformance is apparent compared to State Street SPDR S&P Aerospace & Defense ETF (XAR). The exchange-traded fund has gained about 46.6% over the past year. Moreover, the ETF’s 12.4% returns on a YTD basis outshines the stock’s single-digit losses over the same time frame.

www.barchart.com

www.barchart.com HII’s Q1 outperformance came from 18% shipbuilding sales growth on higher throughput and efforts to rebuild the U.S. maritime base. The company hired 1,600+ shipbuilders in Q1, hit Newport News milestones like CVN-79 sea trials, and targets about 15% throughput improvement this year. Mission Technologies landed major awards including $25 billion and $151 billion defense contracts while expanding autonomous systems and AI partnerships. CFO Tom Stiehle reaffirmed guidance, contingent on sustained throughput gains and upcoming Virginia and Columbia class submarine contracts.

On May 5, HII shares closed down more than 10% after reporting its Q1 results. Its EPS of $3.79 exceeded Wall Street expectations of $3.70. The company’s revenue was $3.1 billion, beating Wall Street forecasts of $3 billion.

For the current fiscal year, ending in December, analysts expect HII’s EPS to grow 12.4% to $17.29 on a diluted basis. The company’s earnings surprise history is impressive. It beat the consensus estimate in each of the last four quarters.

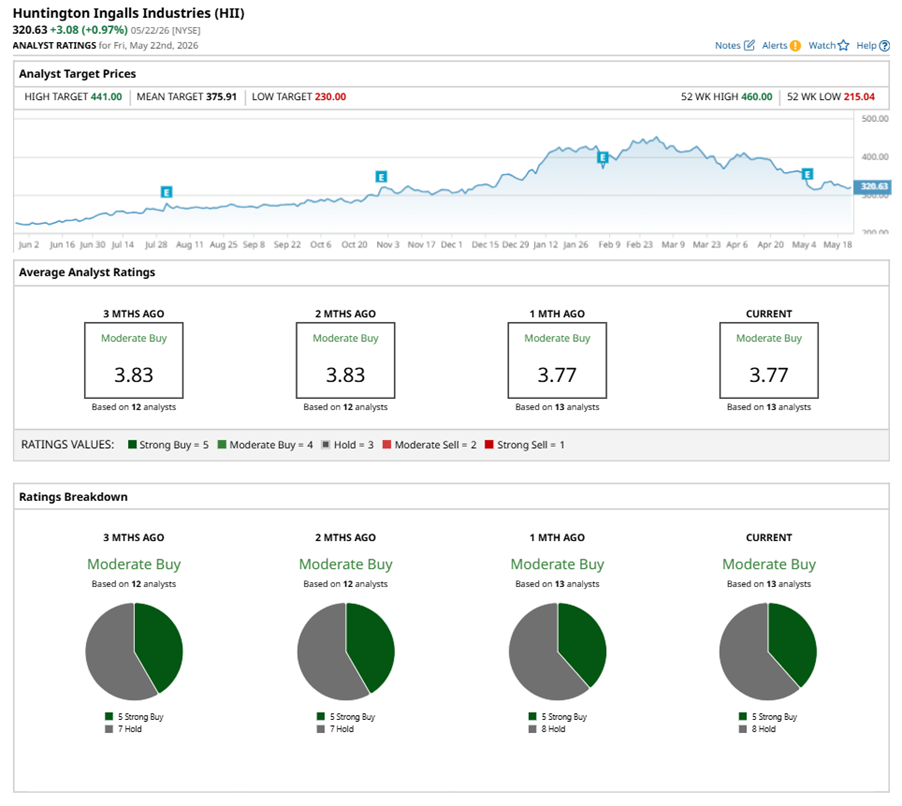

Among the 13 analysts covering HII stock, the consensus is a “Moderate Buy.” That’s based on five “Strong Buy” ratings, and eight “Holds.”

www.barchart.com

www.barchart.com The configuration has been relatively stable over the past three months.

On May 22, JPMorgan Chase & Co. (JPM) analyst Seth Seifman maintained a “Hold” rating on HII and set a price target of $375, implying a potential upside of 17% from current levels.

The mean price target of $375.91 represents a 17.2% premium to HII’s current price levels. The Street-high price target of $441 suggests a notable upside potential of 37.5%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

How to Trade Lockheed Martin Stock Now Amid Escalating U.S.-Iran Tensions Micron Stock Is Up 726%. This Options Strategy Pays You to Buy the Dip Lowe's Delivers Strong Free Cash Flow, But the Stock Fell - Time to Buy LOW? Bear Call Spread Opportunities for May 26