With sticky inflation re-emerging as the dominant macro story, retail investors are aggressively searching for a shield to protect their purchasing power. Naturally, there’s a flood of advice pointing them to Treasury Inflation-Protected Securities (TIPS) —specifically to giant index trackers like the iShares TIPS Bond ETF (TIP).

The narrative sounds bulletproof, right? Consumer prices are rising, so an asset legally engineered to adjust its principal alongside inflation must be a slam dunk.

Join 200K+ Subscribers: Find out why the midday Barchart Brief newsletter is a must-read for thousands daily.

Let’s be clear on this: TIPS are a very good invention, and will help a lot of long-term investors automate a part of their retirement portfolio. And I’m a huge fan of bond ladders. As I’ve written here at some length, my zero-coupon U.S. Treasury Bond ladder is the biggest single part of my own retirement portfolio. And I’m semi-retired, so this is not some “one day I will…” situation.

But I’m here to give you a very serious tip: You need to be incredibly careful with TIPS. That includes buying them directly or via an ETF like the nearly $15 billion in assets TIP from Blackrock’s iShares.

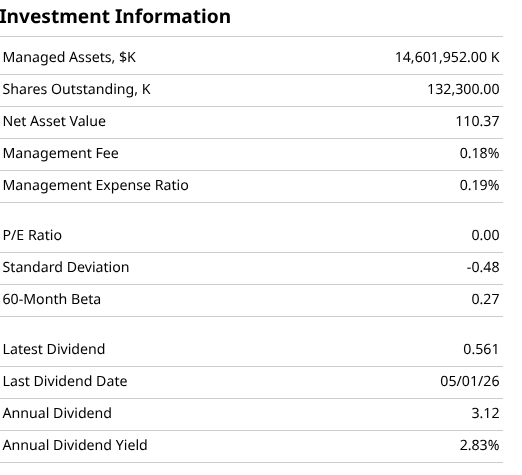

www.barchart.com

www.barchart.com The biggest misunderstanding in the retail investing world is the assumption that buying a TIPS ETF is the exact same thing as buying a pure inflation hedge. It isn’t.

When you buy a fund like TIP, you aren’t just making a targeted bet on consumer price changes. You are taking on a massive amount of traditional bond market risk. Simply said, TIPS investing is not quite as simple as “buy these bonds, make a nice inflation-adjusted return.”

To understand the vulnerability of these instruments, look no further than what happens when the bond market starts selling off long-term debt. TIPS are still bonds. They possess duration, which means their underlying prices remain highly sensitive to fluctuations in broader interest rates.

Lately, the 10-year U.S. Treasury yield has been breaking out of its long-term ranges, climbing aggressively. When the bond market sells off bonds and pushes yields higher, bond prices fall across the board — and TIPS are absolutely not immune.

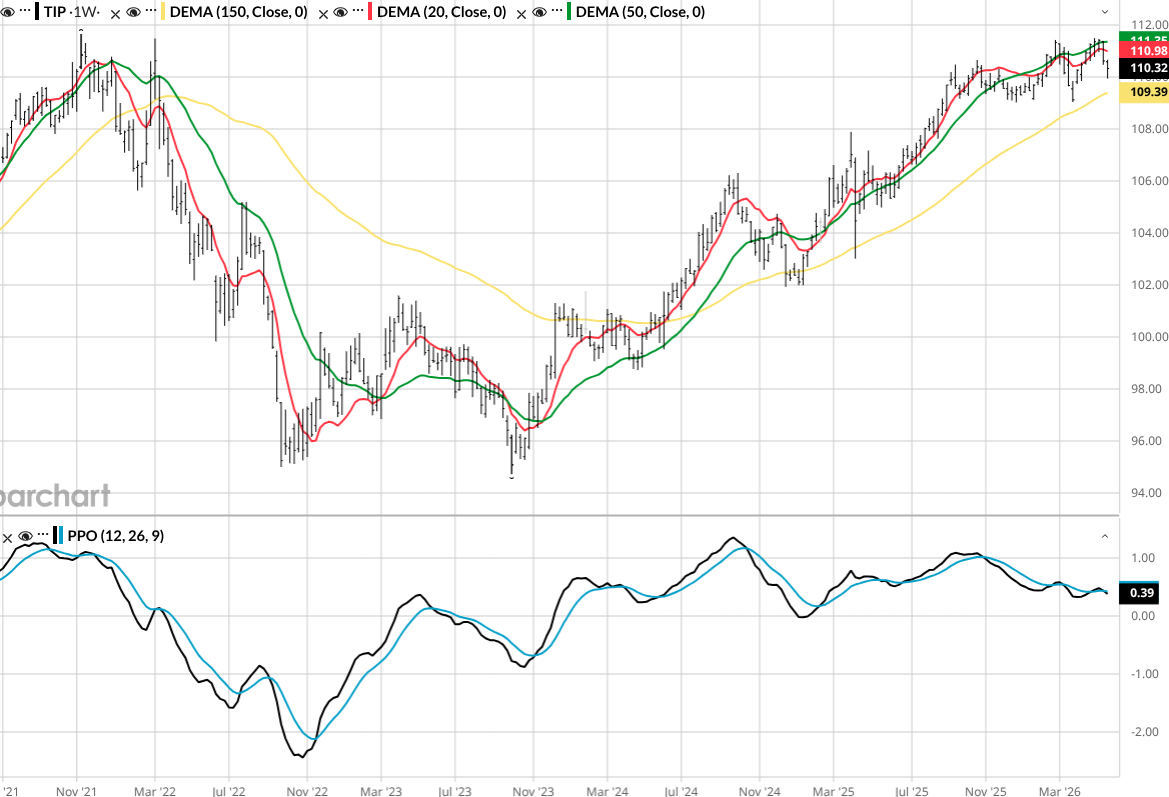

As you can see in the chart below, TIPS are OK, but they are not the same as a regular bond ladder. While you can build a ladder with TIPS, the pricing mechanism is such that you cannot say today exactly how much you are getting at each maturity date. You will get the principal back, but the interest return is not set in stone. It is a fixed return plus a floating inflation-driven percentage. The latter fluctuates with each semi-annual payment. That might be higher or lower than what you could have locked in with a traditional ladder.

www.barchart.com

www.barchart.com The first thing to note about that chart above is that it has been rising in price. But so have bond yields, which means “regular” bonds without inflation protection are falling in price. Quite a bit in fact, at the long end of the yield curve.

But the inflation protection lifts the yield and thus the return, offsetting what would normally be pressure on the bond price. That’s great while inflation is spiking. But it might lure people into TIPS for temporary reasons. That’s part of my concern.

For a shorter-duration version of owning TIPS through an ETF, the Vanguard Short-Term Inflation-Protected Securities ETF (VTIP) is an alternative. Why? Because we don’t know what inflation will be a year from now, much less 15-30 years from now. So at least with that shorter-term approach, you are not locked in for terribly long.

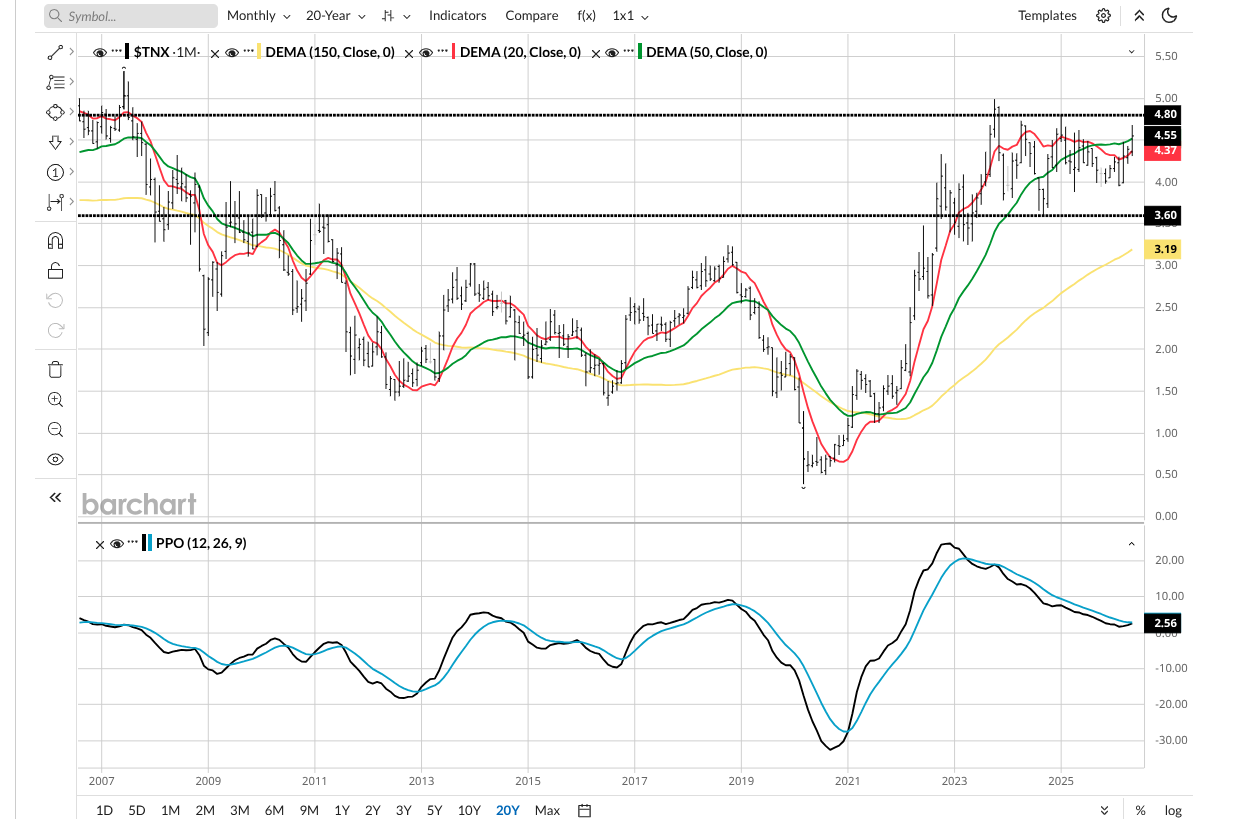

As I see it, inflation now is very different from what it could be. And in what direction, I don’t know. So putting lots of chips on what to me are uncertain strategies, innovative as they are, is not ideal. Consider those who bought TIPS bonds, directly (owning the bonds) or through an ETF or mutual fund, back when inflation and interest rates were around the current level, about 20 years ago. Then, inflation and rates fell to zero during the financial crisis, and stayed on the floor for a long time.

The opportunity, albeit with perfect hindsight, was to lock in the rate levels like you see on the far left side of this chart. Inflation and rates fell together, as they typically do. That left TIPS total yields much lower for much longer.

www.barchart.com

www.barchart.com Even though inflation is proving to be sticky and elevated, the downward pressure exerted by surging long-term yields can completely wipe out the positive adjustments you get from inflation indexing. The underlying net asset value of the ETF can bleed capital during a fixed-income bear market, leaving long-only investors holding paper losses despite inflation running hot.

Why Using CPI to Set TIPS Rates Is a Problem

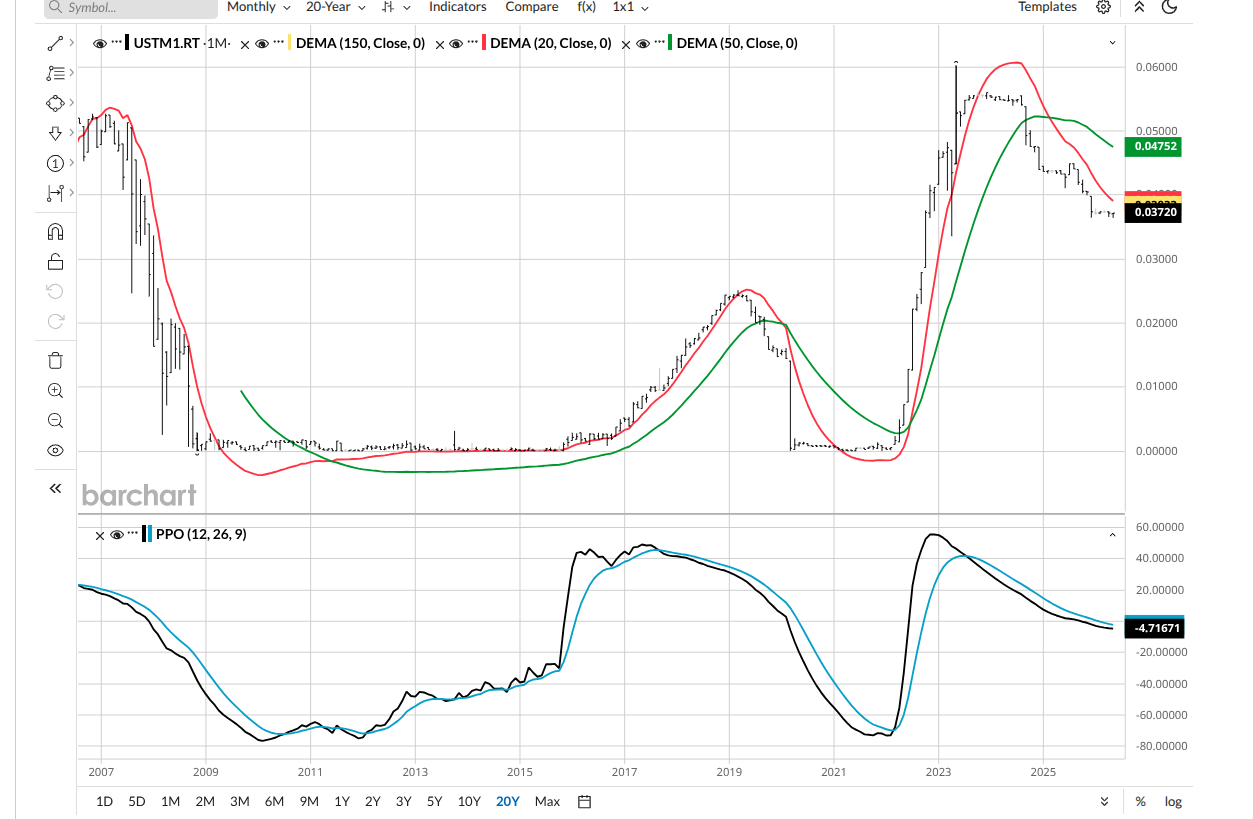

This has everything to do with the U.S. official inflation rate, the Consumer Price Index (CPI). I’ve used 1-month T-bills as a proxy in this chart. When it dives, so does your return on TIPS, since much of it is based on this. It is a tradeoff. In periods of higher rates, TIPS are competitive. If rates go down and stay down, as in this previous case, then locking in for longer makes sense.

www.barchart.com

www.barchart.com I don’t know about you, but if I look at CPI inflation, then my own personal inflation, they are not always in sync. But I can’t plug my own inflation rate in and buy TIPS bonds based on that. I’m beholden to the CPI, which is questionably an archaic way to calculate “inflation.”

Why do I prefer building a bond ladder using zero-coupon bonds? Because I want to know exactly what I’m getting and on what date I’m getting it. No, there’s no inflation protection built into that. But there’s more certainty. And that means I can manage around those dedicated, known “nominal dollar” cash flows as I see fit. That’s the active manager in me talking.

But that’s not for everyone. Which is why I have no major issues with TIPS. They are just not for me, not at this point. Check back with me if CPI is on its way to double-digits.

Treating a long-term TIPS ETF as a simple, risk-free inflation hedge ignores basic bond math. If long-term interest rates continue to push into restrictive territory, vehicles like TIP will face severe structural drag. Be smart, manage your risk, and handle TIPS with care.

Rob Isbitts created the ROAR Score, based on his 40+ years of technical analysis experience. ROAR helps DIY investors manage risk and create their own portfolios. For Rob’s written research, check out ETFYourself.com.

On the date of publication, Rob Isbitts did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Don’t Ignore Basic Bond Math and Jump Into TIPS: The ‘Inflation Hedge’ Story Isn’t Everything Telecom Stocks Are Surging Ahead of the SpaceX IPO. This Chart Reminds Us All Rockets Come Crashing Back to Earth Eventually. This Sports-Betting ETF Is Set to Stage a Comeback in the Second Half of 2026 When Growth Stocks Finally Collapse, You’ll Want This 1 Anti-Beta ETF in Your Portfolio