Artificial intelligence (AI) server powerhouse Super Micro Computer (SMCI) has experienced one of the most dramatic boom-and-bust stories of the AI era. Once celebrated as a top beneficiary of the AI revolution, Super Micro surged into the spotlight as demand exploded for the company’s high-performance storage, networking, and server solutions powering data centers, cloud computing infrastructure, and enterprise AI workloads.

But while the company rode the massive AI wave, it also found itself repeatedly caught in controversy, with investor enthusiasm often clashing against mounting concerns over shady accounting practices, governance issues, and regulatory scrutiny. Now, Super Micro’s reputation has once again landed in troubled waters. Last week, Taiwanese prosecutors announced an investigation into three individuals suspected of illegally exporting Super Micro-made high-end AI servers equipped with Nvidia (NVDA) chips that are restricted under U.S. export controls.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The development comes just months after SMCI shares were rocked in March, when the U.S. Justice Department charged three people tied to the company, including one of its co-founders, with allegedly helping smuggle at least $2.5 billion worth of U.S. AI technology into China in violation of American export laws. The situation has reportedly become serious enough for Nvidia CEO Jensen Huang to personally push Super Micro toward tightening its compliance practices.

According to Bloomberg, Huang said Nvidia remains “rigorous” in explaining regulations to all of its partners and added that he hopes Super Micro will “enhance and improve” compliance measures to prevent similar incidents from happening again. So, with chip giant Nvidia publicly calling on Super Micro to strengthen oversight and regulatory discipline, how should investors approach SMCI stock now?

About Super Micro Stock

Founded in San Jose, Super Micro Computer has grown into a global powerhouse in application-optimized IT infrastructure solutions. The company develops systems specifically designed for enterprise computing, cloud infrastructure, artificial intelligence workloads, and emerging technologies such as 5G and edge computing. Its broad portfolio spans servers, storage systems, AI platforms, IoT solutions, networking equipment, software, and related support services, placing Super Micro at the center of the rapidly expanding AI infrastructure boom.

A major pillar of Super Micro’s business model is its in-house design and manufacturing expertise. With operations spread across the U.S., Taiwan, and the Netherlands, the company maintains significant control over key components, including motherboards, power systems, and chassis. This vertically integrated structure not only helps improve operational efficiency and global scale, but also gives Super Micro the flexibility to rapidly adapt to evolving customer needs in the fast-moving AI and data-center markets.

Moreover, the company is well known for its modular “Server Building Block Solutions” approach, which allows customers to configure systems based on highly specific workload requirements. By offering flexibility across processors, memory, GPUs, storage, networking, and cooling technologies, including both air and liquid cooling solutions, Super Micro is able to cater to a wide range of enterprise, cloud, and AI-driven applications. Today, the company carries a market capitalization of roughly $23 billion.

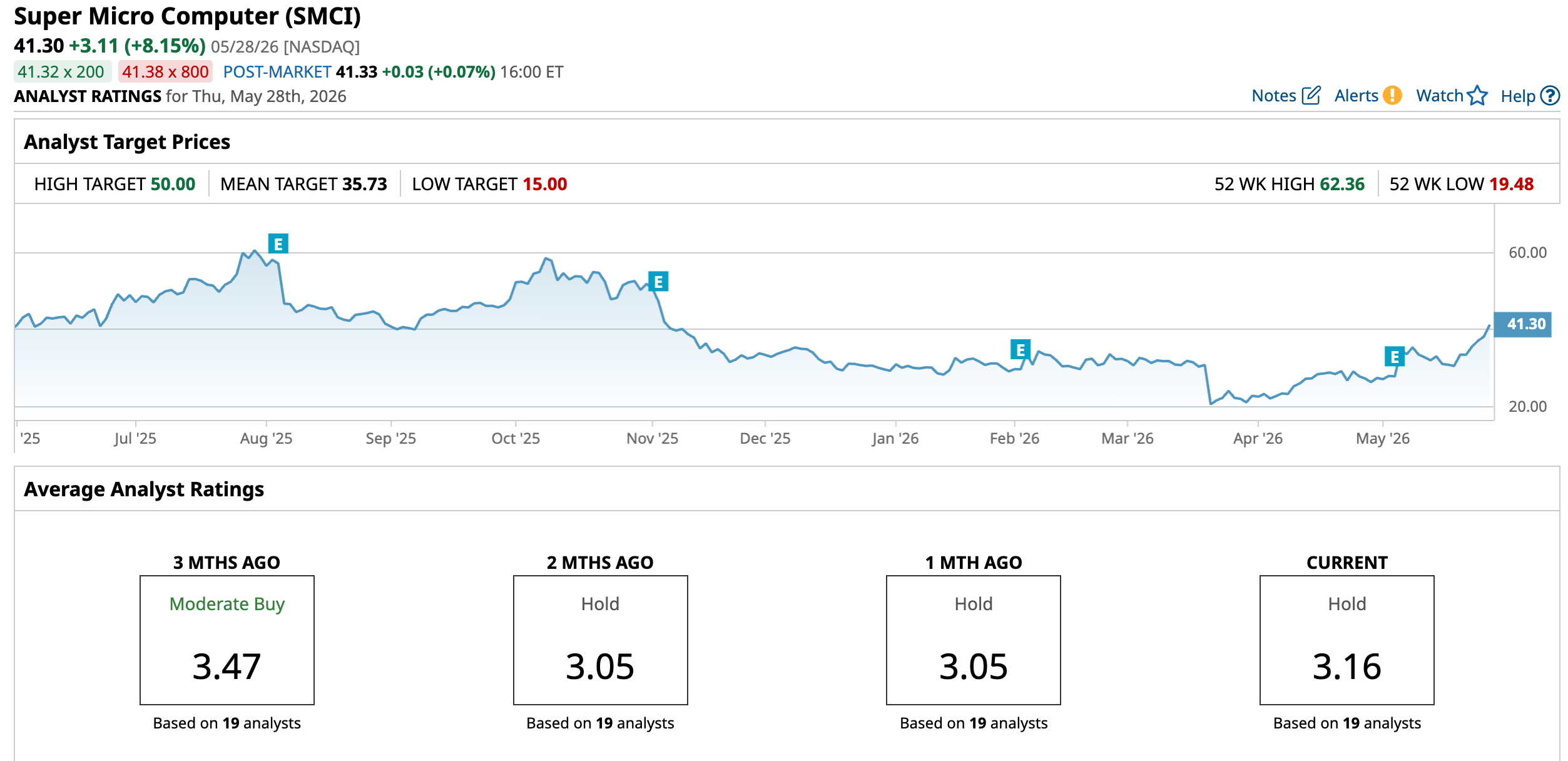

While SMCI’s regulatory troubles have undoubtedly pressured its shares, with the stock still down nearly 33.5% from its 52-week peak of $62.36 reached in July last year and lower by 0.46% over the past 12 months, the outlook has started to brighten in 2026. Explosive earnings results and the massive global buildout of AI infrastructure have continued to fuel investor enthusiasm despite the cloud of ongoing regulatory scrutiny. So far in 2026, SMCI shares have rallied an impressive 42.69%, sharply outperforming the broader S&P 500 Index ($SPX), which has posted a far more modest gain of 10.51% during the same stretch.

www.barchart.com

www.barchart.com Inside Super Micro’s Q3 Earnings Report

Super Micro delivered its fiscal third-quarter 2026 earnings report on May 5, and despite a mixed set of numbers, investors responded enthusiastically, sending the stock soaring an eye-popping 24.54% in the very next trading session. The results once again underscored both the volatility and enormous scale of the ongoing AI infrastructure boom.

The company reported net sales of $10.24 billion, representing a staggering 123% year-over-year (YOY) surge from the $4.6 billion posted in the same quarter last year. However, even after more than doubling revenue, Super Micro still fell short of Wall Street’s lofty expectations, as analysts had projected roughly $12.36 billion in sales amid sky-high optimism surrounding AI demand.

Beneath the headline miss, however, the underlying demand picture remained exceptionally strong. Super Micro said orders and backlog continued to build across its customer base, fueled by relentless AI infrastructure spending, with AI GPU-related platforms accounting for more than 80% of total revenue during the quarter.

Enterprise and channel revenue reached $2.8 billion, making up approximately 28% of total revenue compared to 15% in the previous quarter, while also climbing 46% YOY. Meanwhile, revenue from OEM appliance and large data center customers surged to $7.4 billion, representing roughly 72% of Q3 revenue versus 85% in the prior quarter and skyrocketing 183% from the same period last year.

On the profitability front, Super Micro delivered a massive upside surprise that helped restore investor confidence. The company posted non-GAAP adjusted earnings of $0.84 per share, crushing consensus analyst expectations of around $0.63 and surging 171% from $0.31 in the prior-year quarter. The earnings strength was driven largely by a much stronger-than-expected recovery in gross margins.

Although profitability remains pressured by intense competition, Q3 non-GAAP gross margin improved sharply to 10.1%, up from 6.4% in Q2 and 9.7% in Q3 2025. The company said margins benefited from favorable customer and product mix, along with lower tariff-related costs, reduced expedite expenses, and smaller inventory reserve charges.

At the same time, Super Micro’s balance sheet continued reflecting the heavy financial demands of scaling AI infrastructure at breakneck speed. Cash flow used in operations totaled $6.6 billion during Q3, while capital expenditures and investments came in at $97 million. As of March 31, 2026, the company held $1.3 billion in cash and cash equivalents, compared to total bank debt and convertible notes of $8.8 billion.

Looking ahead, Super Micro projected another massive quarter, forecasting fiscal fourth-quarter 2026 net sales between $11 billion and $12.5 billion. The company also guided for GAAP EPS between $0.53 and $0.67, while expecting non-GAAP EPS in the range of $0.65 to $0.79. For the full-year 2026, the company expects net sales in the range of $38.9 billion to $40.4 billion.

How Are Analysts Viewing Super Micro Stock?

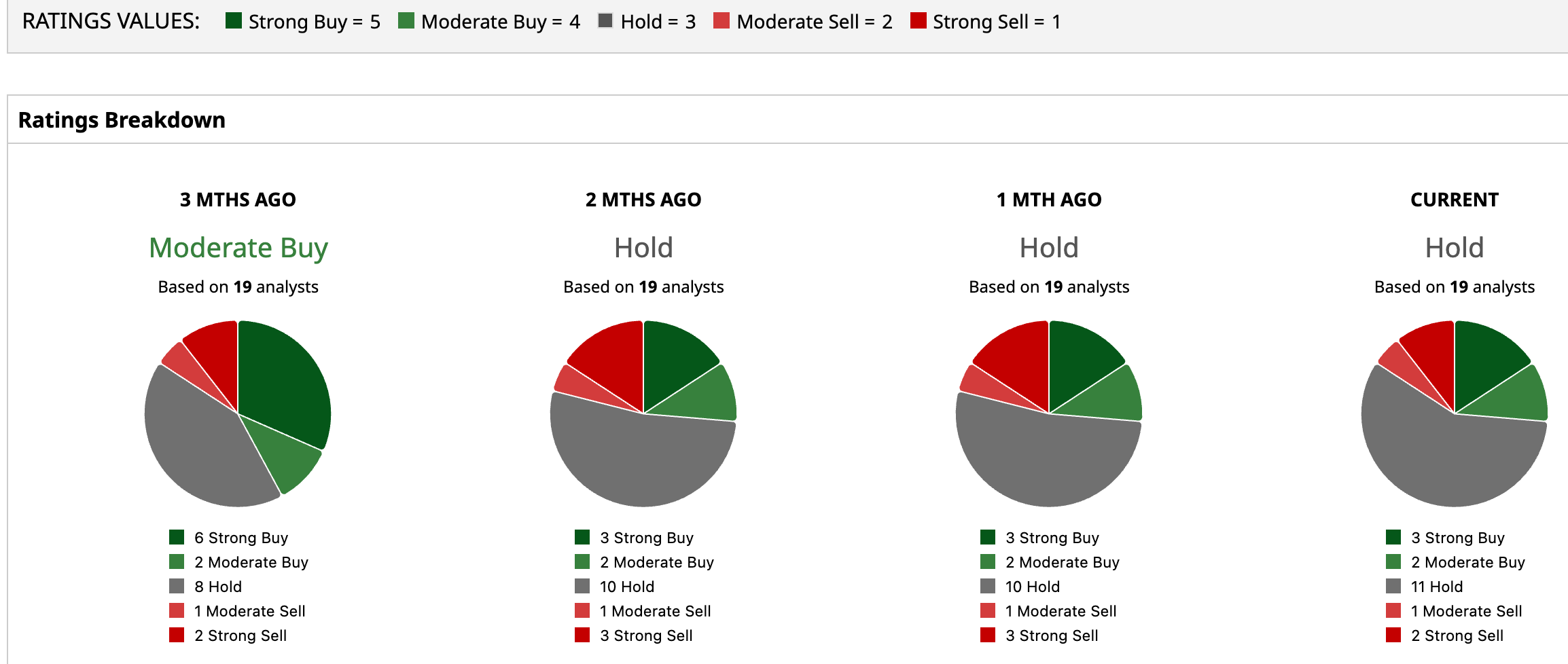

Even after its massive post-earnings surge, Wall Street is still taking a cautious stance on Super Micro as investors weigh the company’s explosive AI growth story against persistent regulatory concerns and execution risks. Overall, SMCI currently carries a consensus “Hold” rating. Of the 19 analysts covering the stock, three recommend “Strong Buy,” two rate it “Moderate Buy,” 11 remain neutral with “Hold” ratings, while one analyst has issued a “Moderate Sell” and two maintain “Strong Sell” recommendations.

While the stock has already climbed above the average analyst price target of $35.73, the Street-high target of $50 still points to potential upside of approximately 21.1% from current levels, suggesting that some analysts continue to believe Super Micro could have meaningful upside ahead if it can maintain its AI-fueled momentum and restore investor confidence.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wedbush Just Set a New Street-High Price Target of $325 on Palo Alto Networks. What This Means for PANW Stock. Billionaire Mark Cuban Asks Why Insurance Companies Pay $2,500 for an MRI When ‘a Center Down the Street’ Only Charges $350 Dropbox Gets A New CEO. The Payoff for DBX Stock Could Take a Long Time. Micron Stock Is Trading at 42x Trailing Earnings. Analysts Say That’s Still Cheap.