JPMorgan’s JPM fee income is likely to grow strongly in the second quarter of 2026, supported by robust trading activity and sustained momentum in investment banking (IB).

Last week, at the Bernstein Strategic Decisions Conference, chairman and CEO Jamie Dimon struck an upbeat tone on the company’s second-quarter fee income prospects. JPMorgan expects markets revenues to rise 11%, reflecting persistent volatility and strong client demand across FICC (Fixed Income, Currencies and Commodities) and equities. IB fees are anticipated to increase 10%, or “a little better,” aided by healthy capital markets and advisory activity.

Rate transitions have fueled volatility across FICC, boosting client hedging and trading activity. With its top-tier trading platform, JPMorgan is well-positioned to benefit from stronger FICC and equities volumes as investors reposition amid a challenging operating backdrop, uncertainty around the ongoing Middle East conflict and the resultant oil price shock.

Further, M&A momentum has strengthened meaningfully so far this year. Corporate deals have driven activity as companies pursue scale, technology capabilities and strategic repositioning. A broader return of private equity firms will further support deal-making, as sponsors look for exit opportunities and new investments.

JPMorgan entered 2026 on a strong note, with the first quarter marked by robust trading activity and improved capital markets performance. In the Commercial & Investment Bank segment, markets revenues rose 20% year over year to $11.6 billion, while IB fees surged 28% to $2.88 billion.

With JPMorgan expecting this momentum to continue in the second quarter, its fee income outlook appears encouraging. Fee income contributes nearly half of the company’s total net revenues, and a favorable view for trading and IB revenues should support top-line growth even as net interest income remains sensitive to the rate path, economic growth and loan demand.

What Does JPM’s Peers Expect for IB & Trading in Q2?

At the same Bernstein Conference, Bank of America BAC and Wells Fargo WFC outlined updated expectations across IB and trading businesses for the second quarter of 2026.

Bank of America expects trading revenues to rise nearly 15% year over year, marking the 17th consecutive quarter of growth in sales and trading revenues. BAC also noted that its IB pipelines remain “pretty good,” supported by improving deal-making activity. Further, Bank of America’s wealth management revenues are expected to increase in the low-teens percentage range year over year, supporting broader noninterest income growth.

Wells Fargo expects a solid improvement in fee-generating businesses, with IB and trading revenues projected to increase in the mid-teens percentage range year over year. Wells Fargo also expects wealth management revenues to grow in the low double-digit percentage range year over year, driven by strong client engagement and continued expansion in relationship-based banking activities, indicating broad-based strength in fee income.

JPMorgan’s Price Performance, Valuation and Estimates

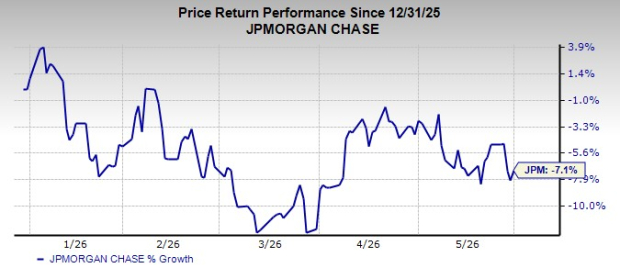

JPM’s shares have lost 7.1% so far this year.

Image Source: Zacks Investment Research

From a valuation standpoint, JPMorgan trades at a 12-month trailing price-to-tangible book (P/TB) of 2.91X, slightly below the industry average.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for JPMorgan's 2026 earnings indicates a 10.1% year-over-year rise, while 2027 earnings are expected to grow at a rate of 5.3%. Over the past month, earnings estimates for 2026 have moved lower to $22.40, while those for 2027 have moved higher to $23.59.

Image Source: Zacks Investment Research

JPMorgan currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Bank of America Corporation (BAC): Free Stock Analysis Report

Wells Fargo & Company (WFC): Free Stock Analysis Report

JPMorgan Chase & Co. (JPM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).