Industrial heavyweight Honeywell International (HON) is giving investors plenty to watch as it advances a sweeping transformation aimed at reshaping the company and unlocking shareholder value. Honeywell is preparing to split into two independent publicly traded businesses while also moving ahead with the highly anticipated initial public offering (IPO) of its quantum computing subsidiary, Quantinuum, this month.

On June 1, the company took another step toward that vision by unveiling new brand identities for its automation and aerospace operations, Honeywell Technologies and Honeywell Aerospace. The two businesses are set to begin trading as separate public companies on June 29, when Honeywell completes the spin-off of its Aerospace division. With that milestone rapidly approaching, all eyes are now on the company’s June 3 investor day, where management is expected to lay out the strategy, growth outlook, and financial profile of the future Honeywell Aerospace.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The event could offer investors critical insights into the value-creation opportunities stemming from the separation. Additionally, Honeywell is scheduled to host a separate investor event for its automation business on June 11.

About Honeywell Stock

Founded in 1906, Honeywell International has grown from a heating controls manufacturer into a diversified industrial and technology powerhouse with operations spanning aerospace, building technologies, industrial automation, and advanced software solutions. The company serves customers across a wide range of industries through its Honeywell Accelerator operating system and Honeywell Forge platform, helping businesses improve efficiency, safety, and sustainability.

Over more than a century of innovation, Honeywell has built a brand estimated to be worth $18 billion, establishing itself as a key player in several mission-critical end markets. As part of its ongoing transformation, Honeywell has unveiled distinct identities for the two businesses that will emerge from its planned separation. The automation segment will operate as Honeywell Technologies and continue trading on the Nasdaq under the ticker HON. The company is expected to focus on industrial automation, software, and autonomous technologies aimed at improving productivity and operational performance across industries.

Meanwhile, the aerospace unit will become Honeywell Aerospace and trade under the ticker HONA following the planned spin-off. As a standalone company, it will rank among the largest pure-play aerospace suppliers, with a portfolio spanning aircraft systems, avionics, propulsion technologies, and next-generation solutions tied to electrification and autonomous flight.

The separation is designed to give each business greater strategic focus as they pursue growth opportunities in their respective markets. Investors have increasingly embraced Honeywell as the company moves closer to its planned breakup and the anticipated IPO of Quantinuum. The industrial giant, now valued at approximately $150.72 billion by market capitalization, has delivered a solid 9.64% return over the past year.

However, the real momentum has come in 2026, with the stock soaring 20.18% year-to-date (YTD) as enthusiasm surrounding its strategic transformation continues to build. That performance has easily outpaced the broader S&P 500 Index ($SPX), which has gained 10.73% over the same period. After climbing to a record 52-week high of $248.18 in March, Honeywell shares remain near their peak, sitting just 5.28% below that level.

www.barchart.com

www.barchart.com Inside Honeywell’s Q1 Earnings Report

Honeywell’s first-quarter fiscal 2026 results, published on April 23, painted a picture of a company executing well operationally, even as revenue came in slightly below expectations. The industrial conglomerate reported adjusted earnings of $2.45 per share, up 11% from the prior year and comfortably ahead of Wall Street’s forecast of $2.32 per share. Revenue rose 2.4% on both a reported and organic basis to $9.14 billion, although it fell modestly short of analysts’ consensus estimate of $9.28 billion. Beneath the surface, profitability remained a bright spot.

Honeywell expanded its adjusted segment margin by 90 basis points to 23.3%, benefiting from strong pricing discipline, productivity initiatives, and accelerated efforts to eliminate stranded costs. On a GAAP basis, however, results were weighed down by one-time items tied to the company’s ongoing transformation. Operating margin declined 320 basis points to 16.1%, while GAAP earnings per share fell 35% year-over-year (YOY) to $1.29, primarily due to debt restructuring charges and asset impairment costs related to non-core businesses held for sale.

Performance across Honeywell’s business segments was mixed. Building Automation stood out as a key growth driver, with sales jumping 11% to $1.88 billion as demand remained robust across data center and hospitality markets. Aerospace Technologies also delivered solid growth, with revenue rising 4% to $4.32 billion, supported by continued strength in commercial original equipment manufacturing and aftermarket services.

In contrast, the Process Automation and Technology segment faced a more challenging environment, with organic sales declining 6% amid project delays and disruptions stemming from geopolitical tensions in the Middle East. One of the quarter’s most encouraging signals came from Honeywell’s future demand pipeline. Organic orders increased 7% across the portfolio, reflecting broad-based customer demand and pushing the company’s total backlog to a record $38.3 billion.

The resulting book-to-bill ratio of more than 1.1x underscored the strength of Honeywell’s long-term growth visibility. Cash flow, however, was pressured by several temporary factors. Operating cash flow came in at -$0.7 billion, declining from the prior year due to higher spin-off and separation-related payments as well as costs associated with settling Flexjet-related litigation.

Free cash flow totaled $0.1 billion and was lower YOY, largely because of collection timing issues, some of which were linked to disruptions caused by the U.S.-Iran war. Despite these headwinds, management reaffirmed its full-year outlook following the stronger-than-expected earnings performance. Honeywell continues to project fiscal 2026 sales of $38.8 billion to $39.8 billion, representing organic growth of 3% to 6%.

Also, the company maintained its adjusted earnings guidance of $10.35 to $10.65 per share, implying annual growth of 6% to 9%. Operating cash flow is expected to range between $4.4 billion and $4.7 billion, while free cash flow guidance remains unchanged at $5.3 billion to $5.6 billion, signaling confidence in the company’s ability to navigate ongoing geopolitical and macroeconomic uncertainties.

How Are Analysts Viewing Honeywell Stock?

As Honeywell moves closer to its highly anticipated breakup, Wall Street is growing increasingly constructive on the stock’s prospects. Reflecting that optimism, Barclays raised its price target on Honeywell to $251 from $243 on May 27 while maintaining its “Overweight” rating. The firm cited several near-term catalysts, including two upcoming capital markets days and the company’s planned spinoffs, which are expected to reshape the industrial giant and potentially unlock additional shareholder value.

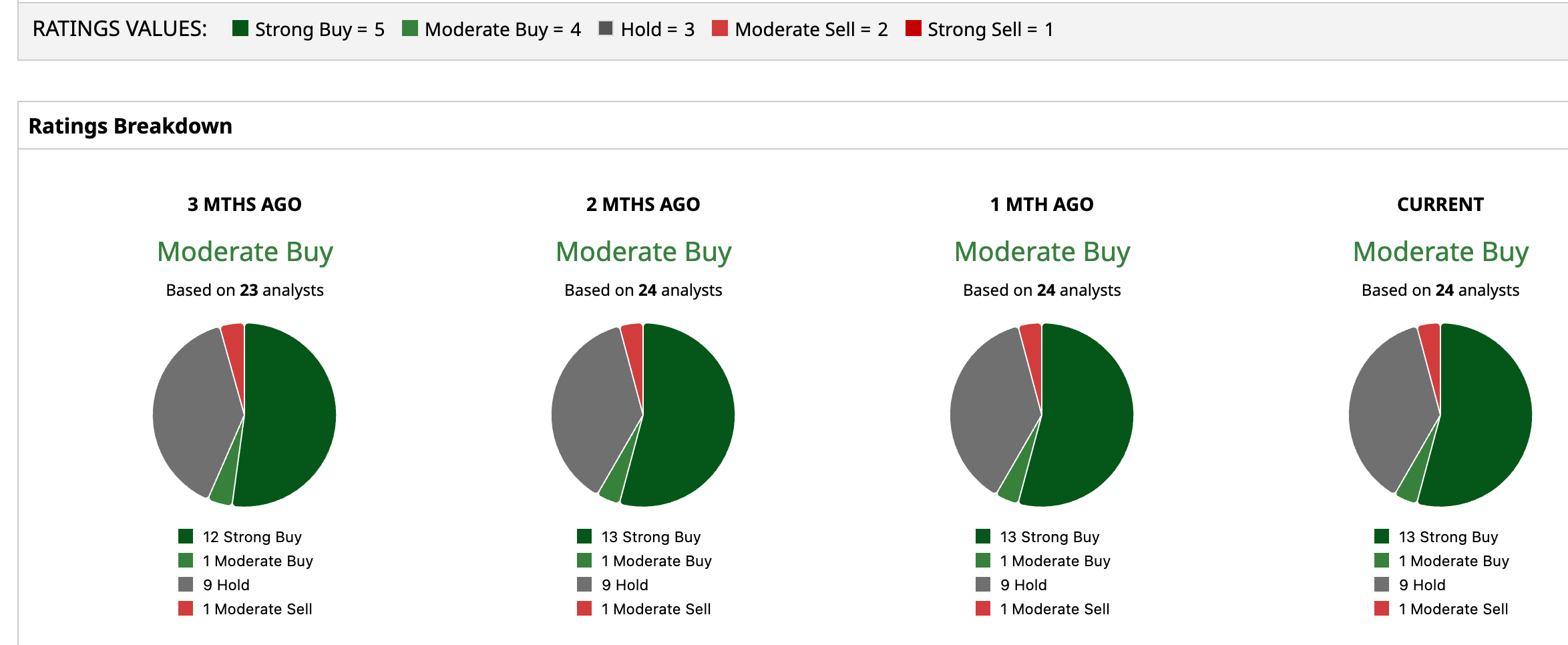

That bullish sentiment is broadly shared across the analyst community. Honeywell currently carries a consensus “Moderate Buy” rating from 24 analysts covering the name, which includes 13 “Strong Buy” ratings and one “Moderate Buy.” Meanwhile, nine analysts remain on the sidelines with “Hold” ratings, while only one analyst recommends a “Moderate Sell.”

The average price target of $249.71 implies 6.24% upside from current levels, while the Street-high target of $290 suggests the stock could gain as much as 23.38% as investors continue to bet on the company's transformation story.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Honeywell Stock Fans, Mark Your Calendars for June 3 NXT Stock Alert: Solar Company Nextpower Is Taking on Data Centers With New Acquisition Costco Just Reported 'Record-Breaking' Gas Sales. COST Stock Is Falling Anyway. Dell Stock Could Be Worth 30% More - Based on Strong AI Demand and FCF