A short squeeze is one of Wall Street’s most painful traps. It happens when investors pile in, betting a stock will fall, only to watch it move sharply in the opposite direction. As losses mount, short sellers are often forced to buy back shares to close their positions. That buying can push the stock even higher, creating a powerful cycle that fuels even bigger gains.

That setup may now be taking shape in Cracker Barrel Old Country Store (CBRL). The restaurant and retail chain has suddenly found itself back in investors’ good graces after delivering a better-than-expected fiscal third-quarter report. The earnings surprise sparked a rally in CRBL stock, but the story did not end there.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Adding more fuel to the move, several Wall Street firms began warming up to the company, raising their price targets following the results, signaling growing confidence in Cracker Barrel’s turnaround efforts.

Meanwhile, short sellers remain heavily positioned against the stock. Nearly 30% of Cracker Barrel’s float is currently sold short, an exceptionally high level by market standards. Even more notable, it would take about 2.05 days of average trading volume for bearish traders to fully unwind their positions.

With improving sentiment, rising analyst optimism, and a massive short bet still hanging over the stock, Cracker Barrel may have all the ingredients for a major short squeeze.

About Cracker Barrel Stock

Founded in 1969 in Lebanon, Tennessee, Cracker Barrel Old Country Store has built its brand around the warmth and tradition of country hospitality. The company operates 657 company-owned locations across 43 states, serving generous portions of homestyle comfort food alongside a unique retail shopping experience.

Over the decades, Cracker Barrel has become a familiar stop for travelers and families seeking a welcoming atmosphere and classic American dining. The company also owns Maple Street Biscuit Company, expanding its presence in the fast-casual restaurant space. Today, Cracker Barrel carries a market capitalization of approximately $1.02 billion while continuing to honor its long-standing heritage.

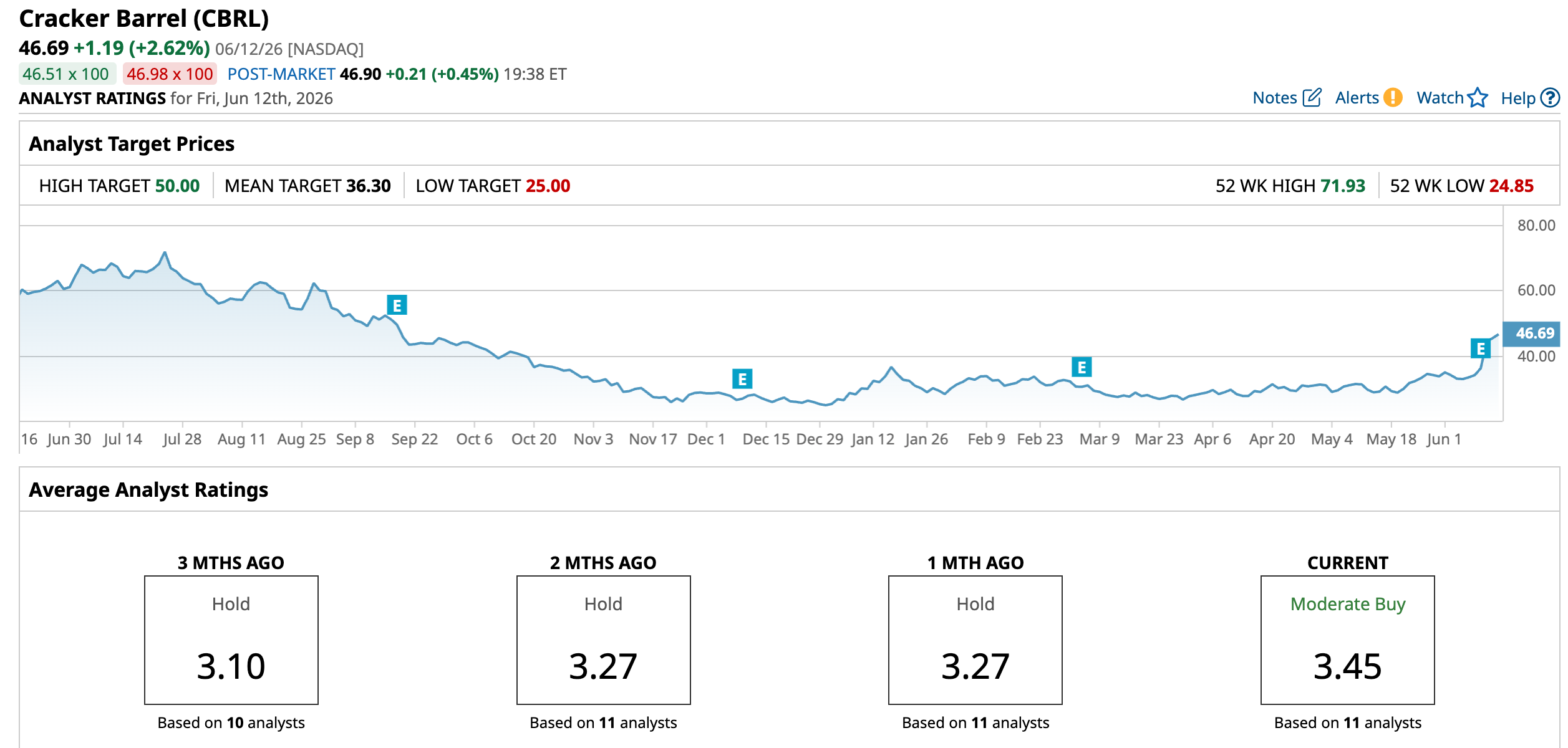

Shares of the restaurant operator have staged an impressive comeback in 2026. After peaking at $71.93 last July, shares tumbled for months and eventually bottomed near $25 in January 2026. Since then, the stock has surged 86.8%, although it remains 35.1% below its 2025 high.

CBRL stock is up 83.82% year-to-date (YTD) and has climbed 69.6% over the past three months alone. Even more striking, the stock has jumped about 39.21% in just the last five trading sessions, decisively breaking above the key $40 level.

The latest rally was sparked by a stronger-than-expected fiscal third-quarter earnings report and a string of analyst price target increases from prominent firms. However, improving fundamentals may not be the only force behind the move. With roughly 30% of the company’s float sold short, Cracker Barrel became a prime candidate for a short squeeze. As the stock surged higher, bearish traders likely rushed to cover their positions, adding fuel to the rally.

The volume chart tells the story. Trading activity exploded following earnings, with volume reaching 11.3 million shares, nearly 10 times the stock’s average daily volume. The surge in green volume bars suggests buying demand far exceeded normal levels.

The momentum remains firmly bullish. The MACD oscillator shows the MACD line above the signal line, while the histogram remains in positive territory. Meanwhile, the 14-day RSI of 82.88 has moved into overbought territory, a sign that the stock may be stretched in the near term. However, with short interest still exceptionally high, additional short-covering could continue to fuel the rally, allowing shares to push higher even as technical indicators suggest caution.

www.barchart.com

www.barchart.com Even after its recent rally, Cracker Barrel’s valuation remains relatively modest. The stock currently trades at 0.31 times forward sales, a level that sits below both the broader restaurant sector average and the company’s own historical valuation.

Income investors may also find the stock appealing. Cracker Barrel has maintained a dividend-paying track record for 27 consecutive years and recently declared a quarterly dividend of $0.25 per share, payable to the shareholders on Aug. 12. It equates to an annualized dividend of $1.00 per share and offers a dividend yield of roughly 2.25%, providing shareholders with a steady income stream while the company's turnaround story unfolds.

A Snapshot of Cracker Barrel’s Impressive Q3 Report

On June 9, Cracker Barrel posted better-than-expected Q3 numbers, and it impressed investors. Revenue slipped 2.9% year-over-year (YOY) to $797.4 million, while adjusted EPS fell 50% annually to $0.29. On the surface, those numbers may not look impressive. However, both revenue and earnings came in ahead of Wall Street’s expectations, giving investors a reason to feel cautiously optimistic. Adjusted EBITDA amounted to $40.3 million, or 5.1% of revenue.

Cracker Barrel continued to push through menu price increases, helping lift the average guest check by 4.3% to $15.85. Even so, management emphasized that the brand remains one of the more affordable dining options in its category, an important advantage as consumers continue to watch their spending.

Customer engagement also moved in the right direction. The company's loyalty program has grown to roughly 12 million members, with loyalty-related sales now accounting for more than 40% of revenue. And off-premise sales, including catering and delivery, gained momentum and represented nearly one-fifth of restaurant sales during the quarter.

Meanwhile, Cracker Barrel’s retail business delivered an encouraging surprise. Retail revenue reached $139 million, and retail comparable sales outperformed restaurant comparable sales for the first time in more than four years. Popular items such as toys, collectible salt-and-pepper shakers, and seasonal merchandise helped drive results.

Further, management highlighted improving guest satisfaction metrics. The company’s Google star rating rose 4% YOY and reached its highest quarterly level since 2018, while scores related to food quality, service improved 5% and food temperature rose 7%. Lower employee turnover among both managers and hourly workers provided another positive signal that operational improvements are taking hold.

Financially, Cracker Barrel remains on solid footing. The company ended the quarter with $541.3 million in available liquidity and $486.6 million in total debt. At the same time, restructuring efforts are expected to generate annual savings of $20 million to $25 million, while investments in artificial intelligence and digital tools are helping improve labor planning, forecasting, and online ordering capabilities.

Looking ahead, management acknowledged that pressure on lower-income consumers, higher gas prices, and tougher YOY comparisons could create challenges. But they also pointed to several encouraging trends that support a gradual recovery. Improving guest satisfaction scores, stronger loyalty engagement, growing off-premise sales, and tighter cost controls have given leadership greater confidence in the company’s direction.

That same confidence was reflected in the company's updated outlook. Cracker Barrel now expects fiscal 2026 revenue to range between $3.27 billion and $3.30 billion, supported largely by menu pricing in the low-4% range. Meanwhile, commodity and wage inflation are expected to remain relatively manageable, tracking in the low-2% range. Management also raised its adjusted EBITDA forecast to between $120 million and $125 million, signaling expectations for continued operational improvement despite ongoing sales pressures.

The company is taking a disciplined approach to spending as well. Capital expenditures are projected at $105 million to $115 million and will be focused primarily on maintaining existing restaurants and infrastructure rather than pursuing aggressive expansion initiatives. And, Cracker Barrel has paused a broad rollout of its store remodel program, choosing instead to preserve capital and focus on initiatives that can deliver quicker returns. While that decision may slow efforts to refresh the brand's image across its footprint, management believes it provides greater financial flexibility as the turnaround progresses.

Meanwhile, analysts monitoring Cracker Barrel anticipate the company to remain in the red during fiscal 2026, with analysts forecasting a loss of about $1.26 per share. However, expectations improve considerably beyond that, with the company projected to return to profitability and earn roughly $0.64 per share in the following fiscal year.

What Do Analysts Expect for Cracker Barrel Stock?

Wall Street came away from Cracker Barrel’s latest earnings report more encouraged, with several analysts raising their price targets as signs of progress emerged in the company’s ongoing turnaround effort. The biggest vote of confidence came from Wells Fargo, which upgraded CBRL stock to “Overweight” from “Equal Weight” and lifted its price target to $50 from $35. Analyst Anthony Trainor said the earnings beat and higher guidance suggest the business is on firmer footing, with comparable sales trends moving in the right direction.

He also noted that fourth-quarter guidance points to improving sales momentum and believes the company could see a more meaningful sales inflection in the first half of fiscal 2027 as it moves past challenges tied to last year's logo change. Wells Fargo added that the stock still trades at an attractive valuation despite its recent rally.

Not everyone is fully convinced, however. Citi raised its price target to $34 from $28 but maintained a “Sell” rating, arguing that while the stock could benefit from positive momentum in the near term, broader traffic trends remain a concern.

UBS struck a similar middle ground. The brokerage firm increased its target price to $37 from $31 while keeping a “Neutral” rating. Analyst Dennis Geiger pointed to stronger-than-expected same-store sales, improving customer traffic, and better execution, but cautioned that it is still too early to declare victory, as visibility into a sustained recovery remains limited.

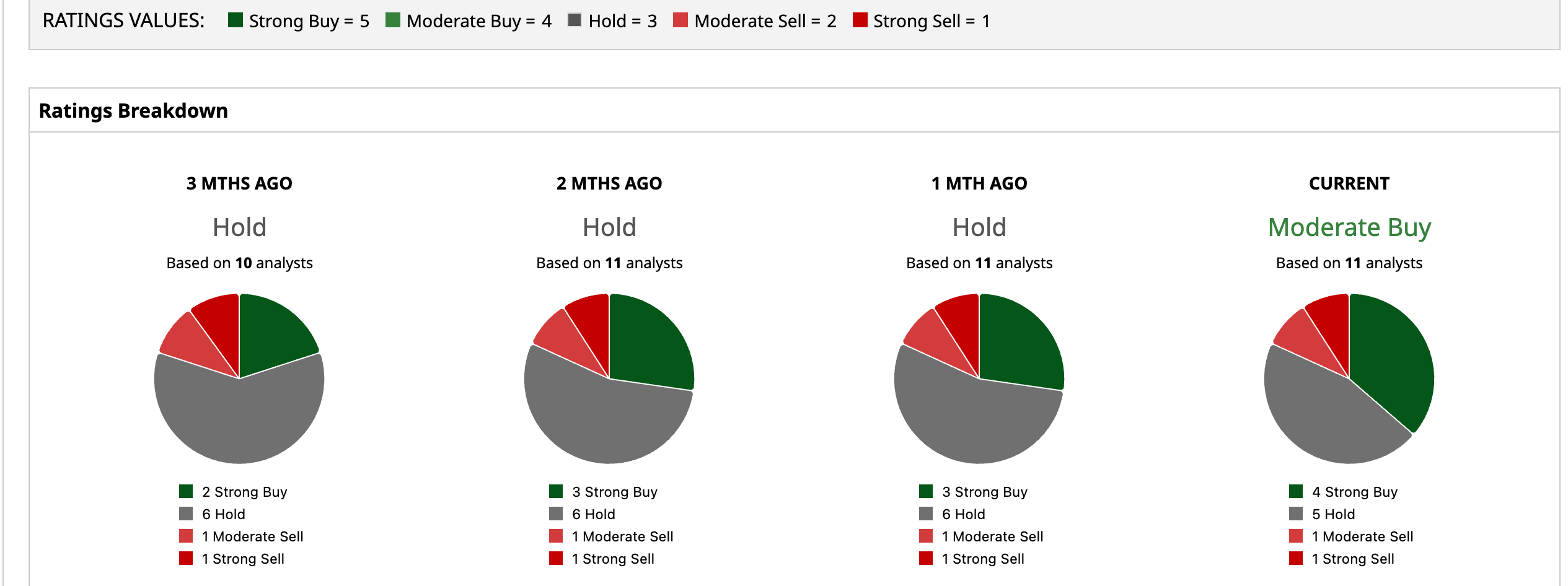

CBRL has a consensus “Moderate Buy” rating from the 11 analysts covering the stock. Among them four advise a “Strong Buy,” five recommend a “Hold,” one has a “Moderate Sell,” and the remaining one analyst is outright skeptic, giving a “Strong Sell” rating to the stock. CBRL’s powerful rally has already carried the stock well above the mean price target of $36.30. Even Wells Fargo's Street-high target of $50 implies only about 7.1% upside from current levels.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A Major Short Squeeze Could Be Brewing in Cracker Barrel Stock A $1.24 Trillion Reason to Buy Dell Stock Now Why Wells Fargo Is Warning That Surging AI Token Costs Is a Death Knell for Hyperscaler Stocks Like Meta and Microsoft Home Depot or Lowe’s: 1 Has Raised Its Dividend for 50+ Years. The Other Pays More Now