London-based Willis Towers Watson Public Limited Company (WTW) operates as an advisory, broking, and solutions company worldwide. Valued at a market cap of $27.8 billion, the company operates through two segments: Health, Wealth & Career and Risk & Broking and offers strategy and design consulting, plan management services and support, broking and administration services for health, wellbeing, and more.

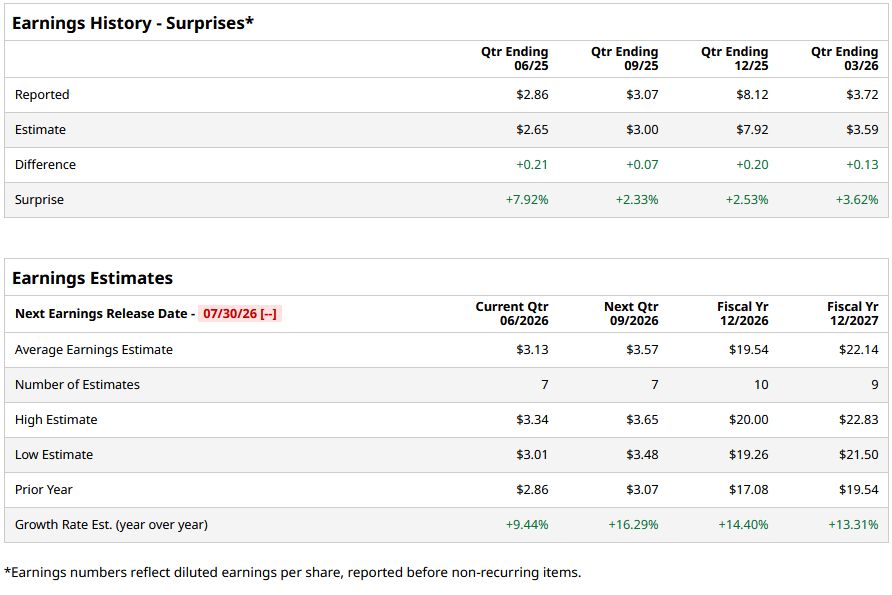

The company is expected to release its Q2 2026 earnings soon. Ahead of the event, analysts expect the company’s EPS to be $3.13 on a diluted basis, up 9.4% from $2.86 in the year-ago quarter. The company has exceeded Wall Street’s EPS estimates in each of its last four quarters.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

For fiscal 2026, analysts project the company’s EPS to be $19.54, up 14.4% from $17.08 in fiscal 2025. Moreover, its EPS is expected to rise by roughly 13.3% year over year (YoY) to $22.14 in fiscal 2027.

www.barchart.com

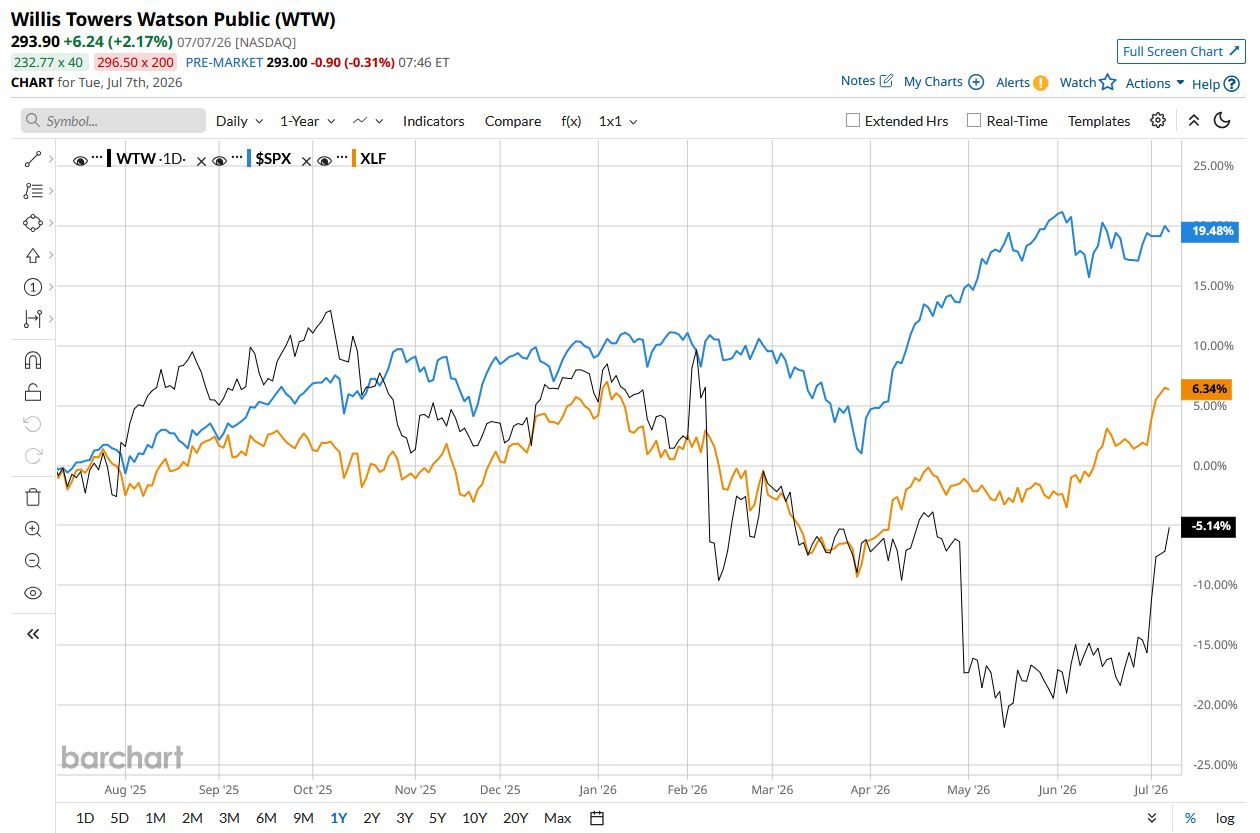

www.barchart.comWTW stock has declined 3.7% over the past 52 weeks, outperforming the S&P 500 Index’s ($SPX) 20.5% rise and also the State Street Financial Select Sector SPDR ETF’s (XLF) 6.4% rise during the same time frame.

www.barchart.com

www.barchart.comOn June 2, WTW shares dipped marginally following the news of its acquisition of Redefind, an end-to-end web-based platform designed to facilitate access to insurance products for crypto and digital assets. This move by the company builds on its long-term strategy to enter next-generation protection solutions for clients exposed to digital finance, crypto ecosystems and tokenized asset environments. Investors, however, were not impressed by this acquisition, leading to another 2% decline in its shares in the following trading session.

Analysts are somewhat bullish about WTW, with the stock having a “Moderate Buy” rating overall. Among the 24 analysts covering the stock, 15 recommend a “Strong Buy,” one recommends a “Moderate Buy,” and 8 recommend a “Hold.” WTW’s average analyst price target is $332.19, indicating an upside of 13% from the current levels.

On the date of publication, Aritra Gangopadhyay did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Nvidia Doubles Down on AI Startups With a Historic Revenue Sharing Model Everyone Thinks Meta’s Cloud Business Is Bad News for CRWV. Here’s What They’re Missing. Memory Prices Heat Finally Reaches Nvidia. Here’s How Jensen Huang Is Dealing With It. This Solar Stock Could Be the Biggest Winner From Trump’s Inverter Crackdown