Cloudflare (NET) received a strong vote of confidence this week. Scotiabank upgraded NET stock to “Sector Outperform” and raised its price target from $225 to $300. This is one of the most bullish calls on Wall Street, with the average consensus being $251.27 according to Barchart's Analyst Ratings data.

Analyst Patrick Colville said that he spent more than four weeks digging into the company before concluding that now is the time to own it. Colville’s bullish view comes from a combination of factors. The big one is that Cloudflare’s Workers platform is quietly becoming the go-to place for building AI-generated apps, including tools like OpenAI Codex and Lovable. The analyst feels that investors haven’t fully realized its significance yet.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

He also pointed to the rising internet traffic, the financial impact of which usually hits the financial books three quarters later. The traffic is now climbing quickly because of the growing importance of agentic AI. Colville believes that this could help Cloudflare beat and raise its forecasts in the second half of the year. Moreover, the analyst’s confidence has grown further after he’s seen Cloudflare winning over the top AI-native customers. He sees this as proof that the company’s technology is built for where the industry is heading.

The timing isn’t a coincidence. Just days earlier, on July 1, Cloudflare launched its Monetization Gateway. This is a tool that lets website owners charge AI agents for access on a pay-per-use basis. It’s a direct attempt to turn AI traffic into actual revenue, which fits neatly with Scotiabank’s thesis. While some analysts remain skeptical, the bulls clearly feel the AI opportunity is only getting bigger.

About Cloudflare Stock

Cloudflare is a cloud connectivity and cybersecurity company that helps make websites and applications faster, safer, and more reliable. Its product portfolio includes Zero Trust security, cybersecurity solutions, cloud networking, and content delivery network services. Founded in 2009, the company is headquartered in San Francisco, California, and is led by co-founder and CEO Matthew Prince.

Over the last 12 months, Cloudflare’s stock has climbed 52%, easily outperforming the broader software sector. The iShares Expanded Tech-Software ETF (IGV) has been down 14% over the same period. The company has further gained momentum in the last month, with NET stock increasing 26%, driven by growing optimism around its position in the AI shift.

www.barchart.com

www.barchart.comCloudflare’s valuation reflects the strength of its underlying business. The forward GAAP P/E isn’t meaningful, as the company’s heavy reinvestment has kept GAAP profits low. The price-to-sales ratio of 44.58x sits 60% above its own 5-year average of 27.82x, suggesting a considerable premium to its historical norms. The earnings outlook and capital structure help justify this premium. The EPS consensus shows improved growth each year through 2029. The expected growth is 29% in 2026, accelerating to over 55% by 2029. The solid trajectory reflects strong analyst confidence in Cloudflare’s expanding role in AI. The balance sheet is another strength of the company, with $4.16 billion in cash against $3.52 billion in debt.

There is no denying that the company is trading at a steep premium. However, with demand from AI and agentic workloads accelerating, many investors believe the premium is well justified.

Cloudflare’s Revenue Rises 34% as AI Demand Accelerates

Cloudflare reported its first-quarter fiscal 2026 earnings on May 7. Revenue of $639.8 million increased 34% year-on-year (YoY), beating the roughly $620.9 million consensus. Non-GAAP EPS of $0.25 also beat the $0.23 consensus. The firm’s sales productivity increased for the ninth consecutive quarter, with deals of over $1 million growing 73%. The operating income also climbed to $73.1 million, and free cash flow reached $84.1 million. Cloudflare announced a restructuring toward an AI-first operating model. This reduced the workforce by more than 1,100 employees. The CEO described the quarter as a strong start to 2026, crediting the company’s strengthened position in AI.

For the second quarter, the management expects revenue of $664 million to $665 million, representing a 30% YoY growth. The company raised its full-year guidance to $2.805 billion to $2.813 billion, along with a higher full-year earnings forecast. The management pointed to accelerating demand from AI and agentic workloads as the key driver for the optimistic guidance. This is consistent with Scotiabank’s reasoning for upgrading Cloudflare’s stock rating.

What Analysts Are Saying About NET Stock

Much like Scotiabank, William Blair analyst Jonathan Ho has also kept a bullish stance for NET stock, maintaining a “Buy” rating. The analyst cited Cloudflare’s growing role in the AI-driven internet as one of the reasons for the positive outlook. A few days before Scotiabank’s upgrade, Bernstein analyst Peter Weed set Cloudflare’s lowest price target on Wall Street of $136, maintaining a “Hold” rating for the firm.

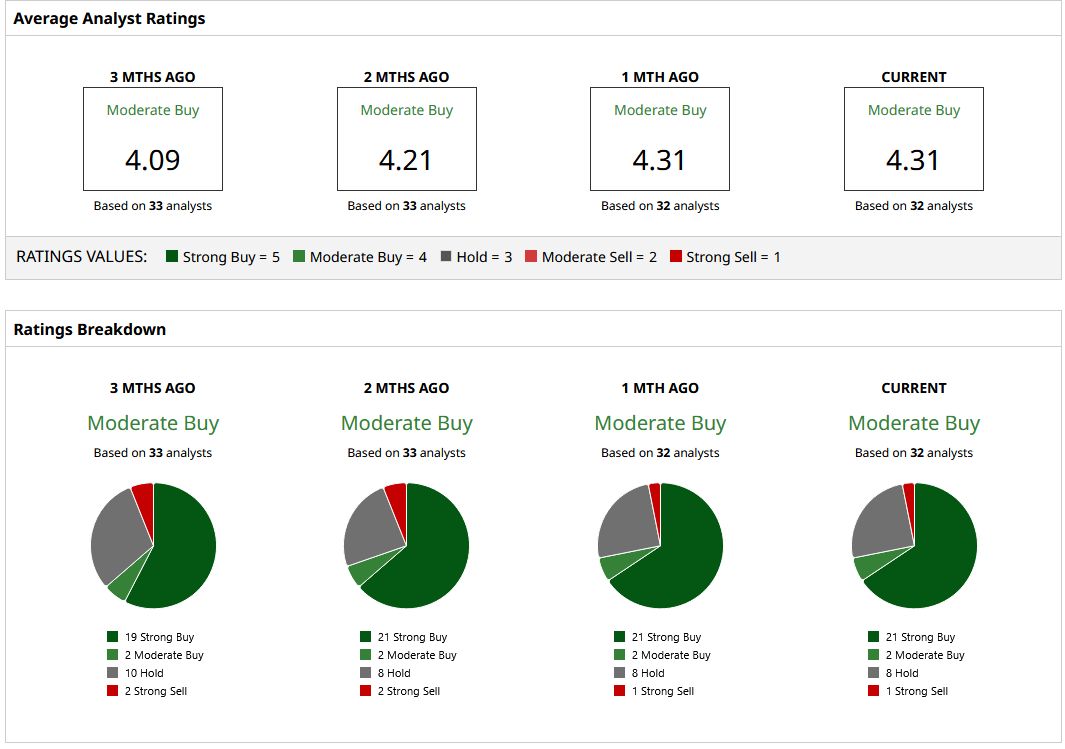

Based on the 32 Wall Street analysts, NET stock holds a “Moderate Buy” rating with a mean price target of $251.27, indicating a 7% downside. Although most of the analysts maintain a bullish view, the marginal downside reflects how strongly the stock has climbed recently, leaving it near its 52-week high.

barchart.com

barchart.com On the date of publication, Jabran Kundi did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Taiwan Just Waved a Red Flag for Nvidia Stock Wall Street Says Investors Are Missing Cloudflare’s Biggest AI Opportunity Navitas Semiconductor Stock Is on the Ropes. It Faces a New Patent Infringement Lawsuit. Grok’s Ongoing Market Share Decline Raises Questions About SpaceX’s AI Strategy Post-IPO