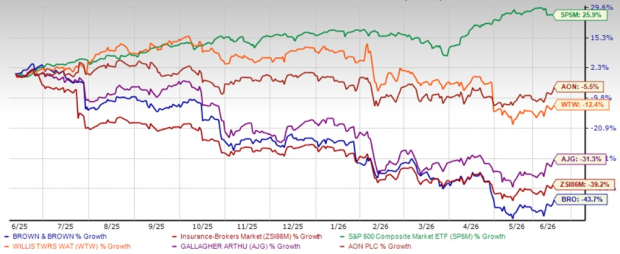

Shares of Brown & Brown, Inc. BRO have lost 43.7% in the past year compared with the industry’s 39.2% decline.

Flat organic growth, margin pressure, valuation compression and earnings estimate cuts are pushing the stock down. Despite these factors, the company's strong client retention, new business generation and acquisitions remain intact, and recovery depends on improving earnings growth, stronger insurance market conditions and margin stabilization.

Shares of other insurers like Aon plc. AON and Arthur J. Gallagher & Co. AJG and Willis Towers Watson Public Limited Company WTW have lost 5.5%, 31.3% and 12.4%, respectively, over the past year.

1 Year Price Performance - BRO, AON, AJG, WTW, Industry & S&P 500

Image Source: Zacks Investment Research

BRO’s Valuation

Shares of Brown & Brown are trading at a discount compared with the Zacks Brokerage Insurance industry. Its forward price-to-earnings multiple of 12.86X is lower than the industry average of 14.91X. It currently carries a Value Score of B.

Image Source: Zacks Investment Research

BRO’s Growth Projection

The Zacks Consensus Estimate for Brown & Brown’s 2026 earnings per share (EPS) indicates a year-over-year increase of 5.9%. The consensus estimate for revenues is pegged at $7.13 billion, implying a year-over-year improvement of 20.9%.

The consensus estimate for 2027 EPS and revenues indicates an increase of 8.3% and 5.2%, respectively, from the corresponding 2026 estimates.

Earnings have grown 19.2% in the past five years, better than the industry average of 13.9%.

The Zacks Consensus Estimate for 2026 and 2027 earnings moved 0.6% and 1.8% south, respectively, in the last 60 days.

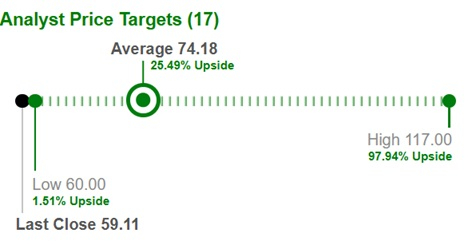

BRO’s Average Target Price Suggests Upside

Based on short-term price targets offered by 17 analysts, the Zacks average price target is $74.18 per share. The average suggests a potential 25.5% upside from the last closing price.

Image Source: Zacks Investment Research

Factors That Benefit BRO

Commissions and fees, the main component of the top line, benefit from increasing new business, strong retention and ongoing rate rises across most lines of coverage. These factors support recurring revenues and earnings visibility. The company met its intermediate annual revenue goal of $4 billion in 2024 and now targets $8 billion in revenues. Last year, its revenues reached $5.9 billion.

Brown & Brown’s strategic buyouts help it capitalize on growing market opportunities, strengthen its products and service portfolio, expand global reach and accelerate growth rate. From 1993 through the first quarter of 2026, Brown & Brown acquired 725 insurance intermediary operations.

The company operates across Retail and Specialty Distribution businesses, providing broad exposure to multiple insurance markets. Revenues from the retail segment have contributed a lion’s share to the company’s total revenues. In the first quarter of 2026, Retail revenues increased 33.4% year over year, while Specialty Distribution revenues rose 40%. The balanced contribution from multiple business lines reduces reliance on any single product line.

The strength of its operating model and diversity of businesses ensures strong cash conversion. It generated operating cash flow of $262 million in the first quarter, up 23% from a year ago. The company effectively deploys cash into acquisitions, capital expenditure and wealth distribution for shareholders via dividend increases. The company has an annualized dividend growth rate of 13.2% over the past five years. The current dividend yield is 1.1%.

Headwinds

Brown & Brown has been experiencing rising expenses due to higher employee compensation and benefits, amortization, changes in estimated acquisition earn-out payables, as well as other operating expenses and interest expense. These factors are creating pressure on margins despite revenue growth.

BRO's expanding international operations expose it to foreign currency, regulatory and economic risks across global markets. Additionally, rising debt levels from acquisition-driven growth are increasing interest expenses. Its total debt to EBITDA of 2.9% is above the industry average of 2.4%.

Profitability metrics also lag industry levels. Brown & Brown’s return on equity is 12.9%, well below the industry average of 18.8%.

Conclusion

New business, strong retention, strategic buyouts, diversified brokerage platform and impressive dividend history position the company well for growth. Robust capital position and cheap valuation are other positives. However, international expansion risks, unfavorable ROE, rising expenses, and debt levels are the headwinds.

Therefore, it is wise to adopt a wait-and-see approach on this Zacks Rank #3 (Hold) stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.7% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Aon plc (AON): Free Stock Analysis Report

Arthur J. Gallagher & Co. (AJG): Free Stock Analysis Report

Brown & Brown, Inc. (BRO): Free Stock Analysis Report

Willis Towers Watson Public Limited Company (WTW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).