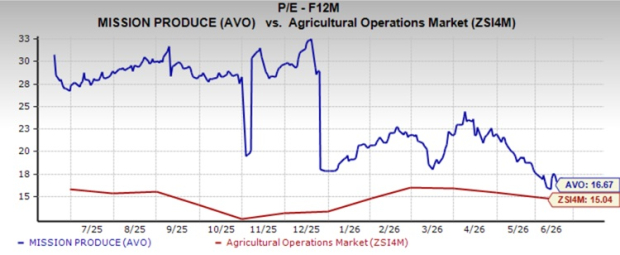

Mission Produce, Inc. AVO has been benefiting from progress on strategic initiatives aimed at deepening customer relationships and expanding across products and global markets. However, the company’s current forward 12-month price-to-earnings (P/E) multiple of 16.67X raises concerns about whether the stock's valuation is justified. This multiple is significantly higher than the Zacks Agricultural - Operations industry average of 15.04X, making the stock appear relatively expensive.

The price-to-sales ratio of Mission Produce is 0.57X, above the industry’s 0.56X. This adds to investor unease, suggesting that it may not be a strong value proposition at the current levels.

Image Source: Zacks Investment Research

AVO’s Premium Valuation Surpasses Peers

At 16.67X P/E, Mission Produce trades at a significant premium to its industry peers. The company’s peers, such as Archer Daniels Midland Company ADM, Dole Plc DOLE and Adecoagro AGRO, are delivering solid growth and trade at more reasonable multiples. Archer Daniels, Corteva and Adecoagro have forward 12-month P/E ratios of 16.32X, 9.97X and 7.51X — all significantly lower than that of AVO.

The AVO stock currently seems somewhat overvalued, and a premium valuation may suggest that investors have strong expectations for its growth.

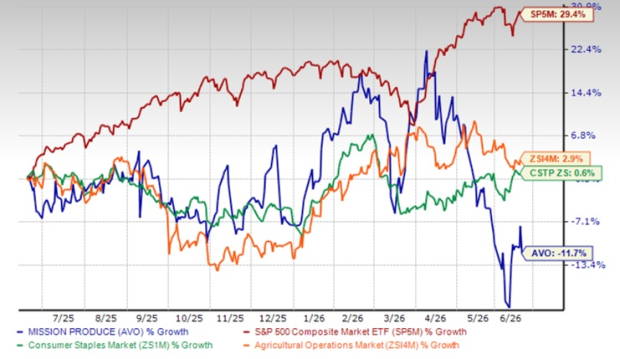

In the past year, the company’s shares have declined 11.7%, outperforming the broader Agricultural - Operations industry’s growth of 2.9% and the Consumer Staples sector’s rise of 0.6%. The stock has underperformed the S&P 500’s growth of 29.4% in the same period.

AVO’s 1-Year Stock Return

Image Source: Zacks Investment Research

Mission Produce’s performance is notably stronger than its competitors. The stock has underperformed Adecoagro and Dole, which have risen 1.5% each in the past year. AVO has also lagged Archer Daniels, which has rallied 41.7% in the past year.

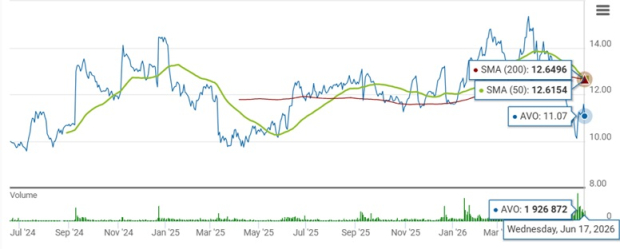

Mission Produce’s current share price of $11.07 is 28.7% below its 52-week high mark of $15.53 and 9.9% above its 52-week low of $10.07. AVO trades below its 50 and 200-day moving averages, indicating a bullish sentiment.

AVO Stock Trades Below 50 & 200-Day Moving Averages

Image Source: Zacks Investment Research

What’s Impacting AVO’s Performance?

Mission Produce’s second-quarter fiscal 2026 performance was primarily impacted by an unusually high avocado supply environment, driven by the largest Mexican crop in years. While the company achieved strong year-over-year volume growth of 15%, excessive supply led to significantly lower avocado prices, with average per-unit selling prices declining 36% from the prior-year period.

The most significant challenge emerged in April when Mission Produce experienced a mismatch between supply and demand for key avocado sizes. High-demand sizes were in short supply, forcing the company to purchase fruit on the spot market at elevated prices, while excess inventory of lower-demand sizes had to be sold at discounted prices. This temporary imbalance compressed per-unit margins and reduced profitability despite healthy consumer demand.

As a result, fiscal second-quarter revenues declined 24% year over year to $290.9 million, while adjusted EBITDA fell to $7.1 million from $19.1 million in the prior-year quarter. Gross profit also decreased to $20.5 million from $28.4 million.

Despite these headwinds, management emphasized that avocado demand remained robust. U.S. avocado consumption reached record levels in the quarter, with more than 1.6 million households entering the category. The company also highlighted that supply conditions have begun normalizing as sourcing shifts from Mexico to California and Peru, leading to recovering margins and improving operating conditions entering the second half of fiscal 2026.

Mission Produce’s Estimate Revision Trend

The Zacks Consensus Estimate for AVO’s fiscal 2026 and 2027 EPS was down 23.9% and 19.7%, respectively, in the last 30 days. For fiscal 2026, the Zacks Consensus Estimate for AVO’s sales implies year-over-year growth of 5.3%, while the same for EPS implies a decline of 35.4%. The consensus mark for fiscal 2027 sales and earnings suggests year-over-year growth of 27.2% and 66.7%, respectively.

Image Source: Zacks Investment Research

Is AVO’s Long-Term Growth Potential Intact?

Mission Produce’s long-term growth potential appears intact despite near-term margin pressure in second-quarter fiscal 2026. Management highlighted several indicators that support a positive outlook, including record U.S. avocado consumption and the addition of more than 1.6 million households to the category in the quarter. The company noted that more than 50% of new avocado-consuming households typically remain in the category, creating a durable demand base for future growth.

AVO also continues to benefit from favorable consumer trends, including increasing demand for fresh, nutrient-dense foods. Management believes that avocados remain one of the grocery industry’s most attractive growth categories, with significant expansion opportunities in both the United States and international markets, such as Europe and Asia, where consumption levels remain relatively low.

The recently completed Calavo acquisition strengthens AVO’s growth profile by expanding packing capacity, enhancing supply-chain flexibility, and providing entry into higher-margin prepared foods products such as guacamole. The company also expects at least $25 million in annualized cost synergies, supporting long-term earnings growth.

AVO’s Investment Rationale

Mission Produce’s long-term growth story remains compelling, supported by favorable avocado consumption trends, international expansion opportunities and the strategic benefits of the Calavo acquisition. However, investors should balance these positives against the company’s current challenges. The stock has delivered weak share price performance in the past year, while downward earnings estimate revisions for fiscal 2026 and 2027 reflect growing near-term uncertainty. These factors suggest that the outlook remains pressured despite improving industry fundamentals.

At the same time, AVO’s premium valuation indicates that investors continue to have confidence in its long-term growth prospects. Given this mixed picture, prospective investors may be better served waiting for a more attractive entry point and closely monitoring the company’s ability to restore margins, deliver synergies and execute its growth strategy before initiating or adding to positions. The company currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Archer Daniels Midland Company (ADM): Free Stock Analysis Report

Dole PLC (DOLE): Free Stock Analysis Report

Adecoagro S.A. (AGRO): Free Stock Analysis Report

Mission Produce, Inc. (AVO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).