Encore Capital Group ECPG is no longer a turnaround story waiting for proof. Shares have climbed 56.2% in the past six months and 120.4% over the trailing 12-month period.

The valuation question is now harder. Investors must decide whether low earnings multiples and higher profit forecasts still leave room for upside, or whether leverage and cost risks should cap the rerating.

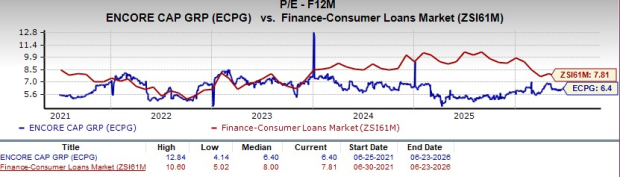

Why ECPG Still Looks Cheap on Earnings

ECPG trades at 6.4X forward 12-month earnings, while its current fiscal-year price-to-earnings ratio is 6.6. That remains below 7.88X for the Zacks sub-industry, 16.29X for the Zacks Finance sector and 21.32X for the S&P 500 index.

The stock is also trading at its five-year median forward multiple of 6.4X, despite a stronger operating setup than it had during weaker collection periods. Its five-year range of 4.14X to 12.84X leaves room for a higher multiple if earnings quality continues to improve.

Image Source: Zacks Investment Research

PRA Group, Inc. PRAA is the closest public comparison because it also acquires and collects nonperforming loan portfolios. That makes portfolio supply, funding access and recovery efficiency central issues for both companies. On the other hand, FirstCash Holdings, Inc. FCFS offers a different way to view consumer-finance exposure. Its pawn-focused model depends less on charged-off receivable purchases, making it a useful contrast to ECPG’s debt-purchasing cycle.

At present, PRA Group and FirstCash Holdings are trading at a premium to ECPG.

How Encore Capital Earnings Are Moving Higher

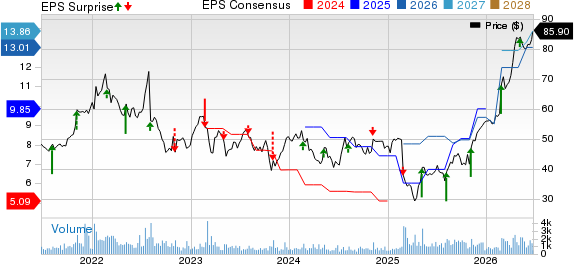

Encore’s latest quarter helped reset the earnings base. First-quarter 2026 earnings of $3.86 per share beat the Zacks Consensus Estimate by 18.4%, while revenues of $475 million rose 21% year over year.

The operating support was clear. Global collections increased 19% to a record $718.4 million, and the U.S. MCM business generated record collections of $556 million, up 23% from the prior-year quarter.

Encore Capital Group Inc Price, Consensus and EPS Surprise

Encore Capital Group Inc price-consensus-eps-surprise-chart | Encore Capital Group Inc Quote

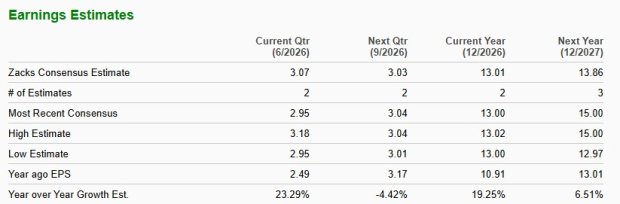

Management raised its 2026 earnings outlook to $13 per share from $12, implying 19% year-over-year growth. The consensus estimate shows earnings rising from $10.91 in 2025 to $13.01 in 2026 and $13.86 in 2027.

Image Source: Zacks Investment Research

What the ECPG Price Target Implies

The $99 price target reflects 7.38X forward earnings. That is not an aggressive multiple relative to the broader market, but it does imply some rerating from the current 6.40X forward 12-month level.

A modest multiple expansion could be supported if collection outperformance keeps flowing into results. Collections exceeded expectations in the first quarter, and positive changes in expected future recoveries suggest estimated remaining collection curves are beginning to move higher.

As those curves adjust, management expects more of the benefit to shift from cash overperformance into portfolio revenues. Stronger reported portfolio revenue can make earnings visibility more durable.

Why Encore Capital Is Not a Simple Value Bet

ECPG’s low multiple comes with balance-sheet risk. Borrowings totaled $4.03 billion at the end of the first quarter, and the company depends on debt funding to purchase receivable portfolios.

Interest expense and other income are projected to total about $300 million in 2026. If borrowing costs remain elevated or portfolio returns normalize, the earnings benefit from higher collections could face pressure.

Legal collection costs are another margin risk. Rising legal activity can support recoveries, but it can also create fixed and semi-variable cost pressure if collections growth slows.

The business mix adds a limitation. The U.S. business is driving most of the momentum, while Cabot in Europe continues to face subdued lending, low delinquencies and strong competition.

How ECPG’s Scores Shape the Investment Call

The bottom line is that ECPG still looks inexpensive, but not risk-free. The earnings reset, low forward multiple and $99 price target support the undervaluation argument, while leverage, legal costs and geographic concentration keep the case selective.

ECPG currently sports a Zacks Rank #1 (Strong Buy), which supports the view that estimate trends remain favorable in the near term. Its Value Score of B also strengthens the bargain case for investors focused on valuation. You can see the complete list of today’s Zacks #1 Rank stocks here.

The rest of the style profile is less supportive. ECPG has a VGM Score of C, Growth Score of D and Momentum Score of F. That mix suggests the stock is better viewed as a selective value opportunity backed by earnings revisions, rather than an all-clear momentum play after a major rally.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

PRA Group, Inc. (PRAA): Free Stock Analysis Report

FirstCash Holdings, Inc. (FCFS): Free Stock Analysis Report

Encore Capital Group Inc (ECPG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).