Shares of Brighthouse Financial, Inc. BHF have gained 17.1% in the past year, outperforming its industry’s growth of 13.8%.

The stock surged following Aquarian Capital’s offer to acquire the company in November 2025 for $70 per share, a price significantly higher than where the stock traded before the announcement. Shareholder approval of the transaction in February 2026 provided additional support to the stock.

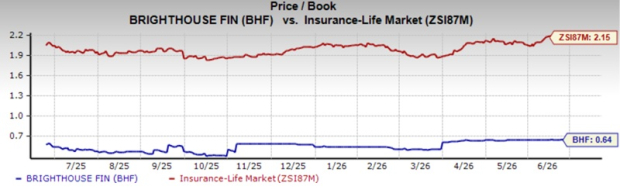

Image Source: Zacks Investment Research

Shares of other insurers like Sun Life Financial Inc. SLF, Primerica, Inc. PRI and Manulife Financial Corp MFC have gained 19.1%, 27% and 6.8%, respectively, over the past year.

BHF’s Valuation

Brighthouse Financial’s shares are still trading at a discount compared with the industry. Its trailing 12-month price-to-book value of 0.64X is lower than the industry average of 2.16X, the Finance sector’s 4.54X and the Zacks S&P 500 Composite’s 7.94X.

Image Source: Zacks Investment Research

Shares of other insurers like Sun Life Financial and Primerica are trading above the industry average, while Manulife Financial is trading at a discount to the industry average.

Projections Confirm Operational Momentum

The Zacks Consensus Estimate for Brighthouse Financial’s 2026 earnings per share (EPS) and revenues indicates a year-over-year increase of 22.8% and 3%, respectively.

The consensus estimate for 2027 revenues and EPS indicates a further increase of 1% and 6.5%, respectively, from the corresponding 2026 estimates.

Factors Acting in Favor of BHF

Brighthouse Financial is one of the largest providers of life insurance products in the United States. Given the expansive and compelling suite of life products, the company should benefit from the growing individual insurance market. The insurer remains focused on ramping up sales of life insurance products and expanding its distribution network, aiming to become a premier industry player. The launch of Brighthouse SmartGuard Plus, its first registered index-linked universal life insurance product, has broadened the company's offerings and supported sales growth.

Annuities remain the primary earnings engine and support cash generation, with annuity sales more than doubling since 2017. The segment generated a strong $324 million of adjusted earnings in the first quarter of 2026. Strong sales of Shield Level Annuities, the newly launched SecureKey fixed indexed annuity and fixed deferred annuities continue to fuel growth. BHF remains focused on enhancing its product portfolio with the launch of Shield Level Pay Plus, an addition to the suite of Shield Annuities. Supported by a diversified portfolio of retirement-focused solutions, BHF expects to maintain strong annuity sales momentum and drive further growth in this key business segment.

Net investment income has been exhibiting an improving trend over the past few quarters. Driven by alternative investment income, asset growth and higher interest rates, the insurer expects the metric to improve in the future. Given a well-diversified, high-quality portfolio and a conservative investment strategy, we expect continued improvement in the metric. BHF estimates a 9-11% annual yield over the long term on an alternative investment portfolio.

BHF’s trailing 12-month return on equity is 16.8%, ahead of the industry average of 15.8%, reflecting the effective utilization of its shareholders' funds.

BHF also remains committed to returning excess capital to shareholders through share repurchases, with $441 million remaining under its buyback authorization as of March 31, 2026.

Risks for BHF

The company has been incurring higher expenses over the past several years, attributable to an increase in policyholder benefits and claims and a deteriorating margin.

Brighthouse Financial’s high debt levels have added to the insurer’s woes. Debt increased fivefold in the last five years. The debt to capital was 35.9%, which deteriorated 430 basis points from the 2025-end level.

End Notes

Higher annuity and life insurance sales, a high-quality portfolio, effective capital deployment, and improving investment income position the life insurer well for growth. However, increasing expenses and high debt levels, leading to higher leverage, remain major concerns.

Higher returns, favorable growth estimates and attractive valuations should continue to benefit Brighthouse Financial. The stock currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Brighthouse Financial, Inc. (BHF): Free Stock Analysis Report

Manulife Financial Corp (MFC): Free Stock Analysis Report

Primerica, Inc. (PRI): Free Stock Analysis Report

Sun Life Financial Inc. (SLF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).