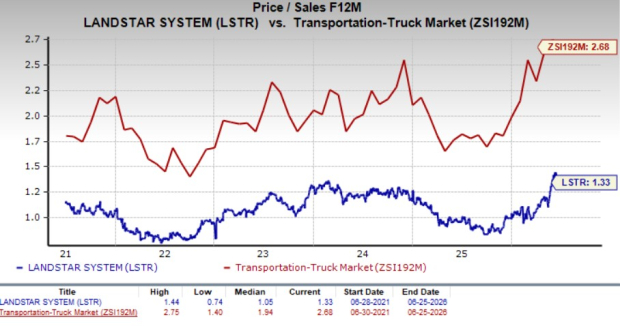

Landstar System, Inc. (LSTR) looks cheap from a valuation standpoint. Considering the forward 12-month price-to-sales ratio (P/S-F12M), LSTR is trading at a discount compared to the industry.

The stock has a forward 12-month P/S-F12M of 1.33X compared with 2.68X for the industry over the past five years. These factors indicate that the stock’s valuation is attractive.

LSTR P/S Ratio (Forward 12 Months) Vs. Industry

Now, the question is whether it is worth buying, holding, or selling the Landstar stock at current prices. Let us delve deeper to find out.

Tailwinds Working in Favor of LSTR Stock

Landstar's efforts to develop its heavy haul services in addition to the cross-border transportation with Mexico are commendable. Cross-border transportation offers significant growth opportunities to LSTR as companies are increasingly sourcing products from Mexico because it moves production lines close to the United States, not only saving production costs but also making the supply chain more secure. Development of the company's heavy haul services should also boost profitability. Heavy haul business refers to the transportation of loads that are larger and heavier than the prepared roadways and bridges can bear, and they need specialized equipment and expert drivers. By bolstering its heavy haul capabilities, LSTR will be able to deliver goods between different sectors (mining, construction and manufacturing) that need transportation of large machinery and equipment.

Landstar’s strong balance sheet increases financial flexibility. The company ended first-quarter 2026 with cash and cash equivalents (and short-term investments) of $353.25 million, much higher than the current debt level of $26.1 million. This implies that the company has sufficient cash to meet its current debt obligations. Meanwhile, long-term debt has decreased to $43.14 million at first-quarter 2026 end from $48.5 million at fourth-quarter 2025 end.

A solid balance sheet enables the company to reward shareholders with dividends and share repurchases. As a reflection of its shareholder-friendly stance, in 2022, 2023, 2024 and 2025, LSTR paid dividends of $115.6 million, $117.1 million, $120.5 million and $124.7 million, respectively. Dividend-paying stocks like LSTR are generally safe bets for creating wealth, as these payouts act as a hedge against economic uncertainty, which characterizes current times.

Landstar is also active on the buyback front. LSTR repurchased shares worth $285.9 million in 2022, $53.9 million in 2023, $81.4 million in 2024 and $179.8 million in 2025. During the first quarter of 2026, Landstar purchased 150,923 shares for $22.6 million. Landstar is currently authorized to purchase up to an additional 1,115,195 shares under its longstanding share purchase program. Buybacks not only reduce the total outstanding share count, thereby increasing earnings per share, but also signal management's belief in the intrinsic value of the stock.

What Do Earnings Estimates Say for LSTR?

The positive sentiment surrounding LSTR stock is evident from the fact that the Zacks Consensus Estimate for second-quarter 2026 and third-quarter 2026 earnings has been revised upward in the past 90 days. The consensus mark for 2026 and 2027 earnings has also been projected northward in the past 90 days.

The favorable estimate revisions indicate brokers’ confidence in the stock.

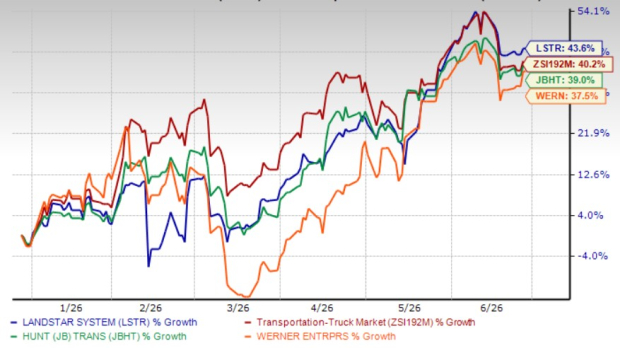

LSTR Stock’s Price Performance

Shares of LSTR stock have gained 43.6% over the past six months, underperforming the transportation-truck industry’s 40.2% surge, as well as that of other industry players, J.B. Hunt Transport Services JBHT and Werner Enterprises, Inc. (WERN), within the same time frame.

LSTR Stock’s Six-month Price Comparison

Headwinds Weighing on LSTR Stock

Landstar is being hurt by reduced demand for freight services and increased truck capacity. Due to the weakness in freight demand, shipment volumes and rates are low. The top line has been suffering mainly due to the below-par performance of its key segment, namely, truck transportation. Revenues are likely to be weak going forward.

Risks associated with the economic slowdown, geopolitical tensions and tariff-induced economic uncertainty continue to bother the stock’s performance. As things stand now, consumer spending and business investments remain low, and production levels have decreased in response to reduced demand, affecting demand for goods transportation and resulting in a freight recession (The Cass Freight Shipments Index, which has declined in all the first five months of 2026. This measure has also deteriorated year over year in each of the past 12 months in 2025, which confirms the overall declining trend). We currently believe that these factors indicate persistent weakness in freight demand through the remainder of this year.

The still-high inflation reading continues to hurt consumer sentiment and growth expectations. With labor and material costs showing no signs of letting off, the ability to pass these increases through to the consumer will determine the profitability of trucking companies like LSTR.

The truck industry, of which Landstar is an integral part, has been persistently battling a driver shortage for several years. As old drivers are retiring, trucking companies are finding it difficult to find new drivers to take their place since the low-paying job does not appeal to the younger generation.

Not an Opportune Time to Buy LSTR Stock

It is understood that LSTR stock is currently attractively valued. Moreover, Landstar's efforts to develop its heavy haul services are commendable and should boost profitability. Cross-border transportation with Mexico also offers significant growth opportunities. A solid balance sheet allows the company to continue paying dividends and buying back shares, reflecting its pro-shareholder stance.

Despite these positives, we advise investors not to buy LSTR stock now, as it continues to be hurt by reduced demand for freight services and increased truck capacity. Due to the demand weakness, shipment volumes and rates are low. Driver shortage continues to be another major concern. Considering all these factors, we advise investors to wait for a better entry point and not buy LSTR now. For those who already own the stock, it will be prudent to stay invested. The company’s current Zacks Rank #3 (Hold) justifies our analysis. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Landstar System, Inc. (LSTR): Free Stock Analysis Report

J.B. Hunt Transport Services, Inc. (JBHT): Free Stock Analysis Report

Werner Enterprises, Inc. (WERN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).