Haemonetics Corporation’s HAE impressive Plasma franchise is poised to drive growth in the upcoming quarters. The robust uptake of the NexSys PCS system bodes well for its long-term growth. However, a debt-burdened balance sheet and fierce competitive pressure remain concerns for HAE’s operations.

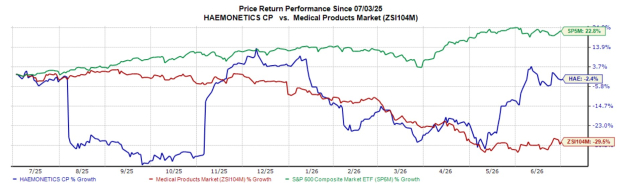

In the past year, this Zacks Rank #3 (Hold) company’s shares have lost 2.4% compared with the industry’s decline of 29.5%. The S&P 500 composite has grown 22.8% in the same time frame.

The global provider of blood and plasma supplies and services has a market capitalization of $2.82 billion. HAE beat on earnings in each of the trailing four quarters, delivering an average surprise of 6.6%.

Let us delve deeper.

Haemonetics’ Key Upsides

Potential Growth Drivers for the Plasma Franchise: Haemonetics’ Plasma business unit focuses on the collection of source plasma for pharmaceutical manufacturers using apheresis devices that only collect plasma. In fiscal 2025, Haemonetics signed new long-term agreements with BioLife and Grifols, reinforcing its continued close partnership and highlighting its ability to bring innovation to plasma collections.

In the fourth quarter of fiscal 2026, the Plasma franchise returned to growth with revenues of $130 million, up 3% on a reported basis and 13% on an organic basis (excluding CSL). Plasma momentum continued with growth driven by category leadership, differentiated innovation, and strong market fundamentals. Its share of U.S. plasma collections grew in the high single digits in fiscal 2026, along with double-digit growth in Europe.

NexSys PCS System Continues to Thrive: Haemonetics’ FDA-cleared, NexSys PCS (plasma collection system) is designed to increase plasma yield collections, improve productivity in customers’ centers, enhance the overall donor experience and provide safe and reliable collections that will become life-changing medicines for patients. Haemonetics received 510(k) clearance for the NexSys PCS Plasma Collection System with Persona PLUS technology. The company’s full transition from the PCS2 devices to the latest NexSys with Persona Technology should drive meaningful improvements in the upcoming quarters.

Image Source: Zacks Investment Research

Haemonetics’ Key Downsides

Weak Solvency: Haemonetics exited the fiscal fourth quarter with cash and cash equivalents of $245.4 million and short-term debt & current maturities of $5 million on its balance sheet. The long-term debt at the end of the fiscal fourth quarter was $1.22 billion, indicating a highly leveraged balance sheet. Debt-to-capital ratio was 50.2%, while times interest earned ratio was 5.5 at the quarter’s end, down 5.5 sequentially.

Competitive Landscape: Haemonetics operates in a very competitive environment, both for manual and automated systems. Slower-than-expected product adoption by customers, especially the American Red Cross, might reduce the company’s revenues and profit.

HAE’s Estimate Trend

The Zacks Consensus Estimate for fiscal 2026 earnings has moved south 1 cent to $5.22 per share in the past 30 days.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $1.40 billion, which indicates a 4.9% decrease from the year-ago reported number.

Key Picks

Some better-ranked stocks in the broader medical space are Globus Medical GMED, Integra LifeSciences IART and Phibro Animal Health PAHC.

Globus Medical has an earnings yield of 5.5%, well ahead of the industry’s negative 3% yield. Its earnings surpassed estimates in each of the trailing four quarters, the average surprise being 26.3%. The company’s shares have rallied 43.8% against the industry’s 4.8% decline over the past year.

GMED carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Integra LifeSciences, carrying a Zacks Rank #2 at present, has an earnings yield of 16% against the industry’s negative 3% yield. Shares of the company have gained 22.8% compared with the industry’s 4.8% growth. IART’s earnings topped estimates in each of the trailing four quarters, the average surprise being 16.8%.

Phibro Animal Health, carrying a Zacks Rank #2 at present, has an earnings yield of 9.2% compared with the industry’s 2.8% yield. Shares of the company have climbed 43.1% against the industry’s 27.9% decline. PAHC’s earnings beat estimates in each of the trailing four quarters, the average surprise being 16.3%.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Haemonetics Corporation (HAE): Free Stock Analysis Report

Integra LifeSciences Holdings Corporation (IART): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

Phibro Animal Health Corporation (PAHC): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).