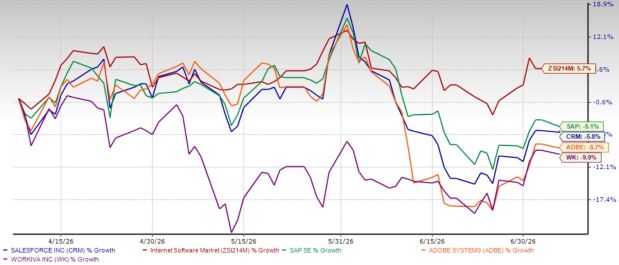

Salesforce Inc. CRM shares have declined 5.8% over the past three months, underperforming the Zacks Internet – Software industry’s 5.7% gain. While the weak performance may concern investors, Salesforce is far from being the only software stock under pressure.

Several enterprise software names, including SAP SE SAP, Adobe Inc. ADBE and Workiva Inc. WK, have also struggled during the same period. SAP, Adobe and Workiva have fallen 5.1%, 8.7% and 9.9%, respectively. The broad-based weakness suggests that investors are reassessing the software sector rather than losing confidence in Salesforce alone.

Salesforce 3-Month Price Return Performance

Image Source: Zacks Investment Research

The biggest overhang is the rapid rise of artificial intelligence, particularly agentic AI. These AI systems can automate complex business tasks with minimal human intervention, prompting investors to question whether the traditional software-as-a-service (SaaS) pricing model, which largely depends on per-user subscriptions, could face pressure over time. If enterprises eventually require fewer software users, subscription growth could slow across the industry.

At the same time, software companies continue to deal with a difficult macroeconomic backdrop. Higher interest rates, persistent inflation and geopolitical uncertainty have made businesses more cautious about technology spending. Many enterprises are taking longer to approve large software purchases, resulting in extended sales cycles across the industry.

Salesforce is naturally exposed to these trends because most of its revenues come from enterprise customers. Slower IT spending could delay new customer wins and reduce expansion opportunities. However, the recent pullback appears to reflect broader market concerns rather than any meaningful deterioration in Salesforce's business.

Salesforce Is Becoming More Than a CRM Company

Salesforce remains the global leader in customer relationship management software, according to Gartner. However, the company is no longer relying solely on its customer relationship management software for growth. It is transforming into a broader enterprise AI platform by combining customer data, collaboration tools and AI-powered automation.

This strategy has been built through both large and small acquisitions. Slack strengthened Salesforce's collaboration platform, and Informatica expanded its data management capabilities, while newer acquisitions such as Doti AI and Spindle AI are enhancing its AI offerings.

The company's biggest growth engine today is Agentforce. In the first quarter of fiscal 2027, Agentforce’s annual recurring revenues (ARR) surged 205% year over year to $1.2 billion, highlighting strong customer demand for Salesforce's AI agents.

The momentum extends beyond Agentforce. Combined AI and Data ARR, including Agentforce, Data 360 and Informatica Cloud, reached $3.4 billion in the first quarter, more than tripling from the year-ago period. Nearly half of Agentforce and Data 360 bookings came from existing customers, showing that Salesforce is successfully expanding relationships within its large installed customer base.

That matters because selling more products to existing customers is typically more profitable than acquiring new ones. It also demonstrates that enterprises are willing to spend more on Salesforce's AI platform despite the uncertain economic environment.

CRM’s Revenue Growth Shows Signs of Improvement

One of the biggest investor concerns has been Salesforce's slowing growth. As the company became larger, revenue growth naturally moderated from the high-growth rates seen several years ago, leading many investors to believe Salesforce had entered a mature phase.

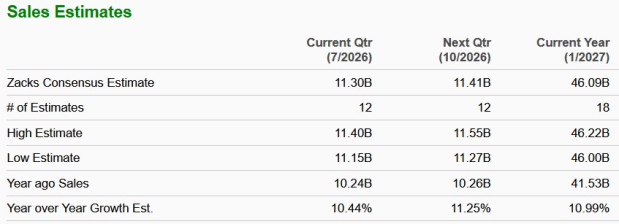

Recent results paint a more encouraging picture. First-quarter fiscal 2027 revenues increased 13.3% year over year, marking a noticeable acceleration from recent quarters. While Salesforce is still way behind its earlier hypergrowth phase, double-digit growth remains impressive for a company of its scale.

Management's guidance also reflects confidence in demand. Salesforce expects revenues to grow 10-11% in the fiscal second quarter and approximately 11% for the full fiscal year. Those projections are largely in line with Zacks Consensus Estimates and suggest that growth remains healthy despite a cautious enterprise spending environment.

Image Source: Zacks Investment Research

Salesforce’s Valuation Leaves Room for Upside

The recent share price weakness has also made Salesforce's valuation more attractive. CRM currently trades at a forward 12-month price-to-earnings (P/E) ratio of 11.26, well below the industry average of 26.32.

Salesforce Forward 12-Month P/E Ratio

Image Source: Zacks Investment Research

Compared with peers, Salesforce also appears reasonably valued. SAP and Workiva trade at forward P/E multiples of 17.74 and 16.24, respectively, while Adobe trades at 8.36 times forward earnings. Although Adobe is cheaper, Salesforce's valuation looks attractive considering its improving growth profile and expanding AI business.

Final Thoughts: CRM Stock Seems Worth Holding

Salesforce still faces legitimate challenges. The software industry is adjusting to the rise of AI, enterprise customers remain cautious about spending, and macroeconomic uncertainty could continue to weigh on near-term demand.

However, the recent decline appears to reflect investor sentiment more than weakening fundamentals. Salesforce is rapidly building one of the industry's strongest enterprise AI platforms and is showing early signs of reaccelerating revenue growth. At the same time, its expanding AI ecosystem is creating new monetization opportunities while strengthening customer relationships.

With the stock trading at a meaningful discount to the broader software industry, much of the near-term uncertainty already appears to be reflected in the valuation. While volatility may persist, the company's long-term growth story remains intact. For existing investors, holding the stock continues to look like the more sensible strategy than selling into the recent weakness.

Salesforce carries a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

7 Best Stocks for the Next 30 Days

Just released: Experts distill 7 elite stocks from the current list of 220 Zacks Rank #1 Strong Buys. They deem these tickers "Most Likely for Early Price Pops."

Since 1988, the full list has beaten the market more than 2X over with an average gain of +23.9% per year. So be sure to give these hand picked 7 your immediate attention.

See them now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Salesforce, Inc. (CRM): Free Stock Analysis Report

SAP SE (SAP): Free Stock Analysis Report

Adobe Inc. (ADBE): Free Stock Analysis Report

Workiva Inc. (WK): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).