Fresenius Medical Care AG & Co. FMS entered 2026 with improving profitability, accelerating execution of its transformation strategy and growing momentum in HighVolumeHDF and value-based care. However, persistent treatment volume weakness, looming reimbursement headwinds, regulatory pressure in China and inflation-related cost risks continue to pose meaningful challenges to the company's long-term growth outlook.

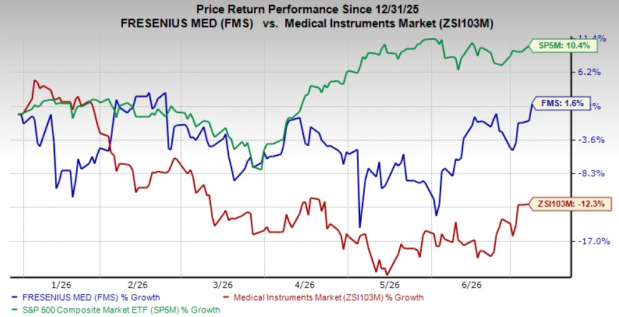

Shares of this Zacks Rank #3 (Hold) company have risen 1.6% so far this year against the industry’s 12.3% decline. However, the S&P 500 Index has gained 10.4% in the same time frame.

FMS, with a market capitalization of $12.68 billion, is one of the largest integrated providers of products and services for individuals undergoing dialysis following chronic kidney failure. Its bottom line is anticipated to improve 2.5% over the next five years. FMS’ earnings beat estimates in three of the trailing four quarters and missed once, delivering an average surprise of 6.6%.

Image Source: Zacks Investment Research

Factors Driving FMS’ Prospect

FME25+ Execution Is Delivering Sustainable Margin Expansion: Fresenius Medical Care's turnaround strategy is increasingly translating into measurable financial improvement instead of remaining a restructuring narrative. During the quarter, the company generated EUR 50 million of sustainable FME25+ savings, supporting 10% operating income growth and a 70-basis-point expansion in operating margin despite only modest revenue growth.

Management highlighted that underlying Care Delivery earnings still increased around 6%, excluding temporary TDAPA reimbursement benefits. Revenue cycle management initiatives, manufacturing optimization, supply-chain efficiencies and accelerated clinic rationalization are collectively improving profitability. With 64 of the planned 100 U.S. clinic closures already completed and further savings expected through the year, FMS appears increasingly capable of expanding earnings even in a slow-growth dialysis market.

HighVolumeHDF Rollout Represents Competitive Advantage: The rollout of the 5008X CAREsystem and HighVolumeHDF therapy represents one of the most significant strategic initiatives in Fresenius Medical Care's history. More than 100 clinics have already converted, more than 100,000 treatments have been performed, and management has reported overwhelmingly positive feedback from physicians, staff and patients.

Beyond improving patient comfort, HighVolumeHDF is expected to reduce hospitalizations, missed treatments and long-term mortality — three variables that directly influence clinic utilization and profitability. While financial benefits will emerge gradually, the technology could materially strengthen FMC's competitive positioning by improving clinical outcomes alongside operating efficiency. If real-world evidence supports clinical trial results, HighVolumeHDF may become an important differentiator in both payer negotiations and patient acquisition over the coming years.

AI-Driven Value-Based Care Creates New Growth Opportunities: Fresenius Medical Care continues to expand beyond conventional dialysis reimbursement by strengthening its value-based care platform. During the quarter, the business achieved profitability for the second consecutive quarter, supported by improved savings rates, contract expansion and operational efficiencies.

Particularly encouraging is management's growing use of AI-driven interventions, which have reduced hospitalizations by as much as 15% and missed dialysis treatments by 26% among high-risk ESRD patients. Combined with more than $270 million in shared savings generated through the U.S. CKCC program and industry-leading quality scores, FMS is demonstrating that better patient outcomes can translate into stronger financial performance. As healthcare reimbursement increasingly shifts toward value-based models, this platform could become a meaningful earnings contributor.

Image Source: Zacks Investment Research

Key Challenges

Uncertain U.S. Dialysis Volume Recovery: Although management reaffirmed expectations for flat U.S. treatment growth in 2026, underlying patient volumes remain under pressure. Same-market treatment growth declined 37 basis points, reflecting weather-related disruptions, elevated mortality, slower patient referrals, insurance uncertainty following ACA subsidy changes and continued missed dialysis treatments.

While management expects HighVolumeHDF, catheter lock solutions and operational improvements to gradually improve patient retention and treatment frequency, these benefits are yet to materially offset structural volume challenges. Because Care Delivery remains FMS' largest earnings contributor, any prolonged weakness in patient growth could reduce clinic utilization and limit operating leverage, forcing additional restructuring initiatives to sustain profitability.

TDAPA Reimbursement Creates a Significant Second-Half Earnings Cliff: A substantial portion of Fresenius Medical Care's first-half earnings strength is being supported by temporary TDAPA reimbursement benefits, particularly from phosphate binders and catheter lock solutions. Management estimated roughly EUR 80 million of TDAPA-related benefit during the first quarter but simultaneously warned that the reimbursement program may become a meaningful earnings headwind during the second half of 2026.

While first-half operating income is expected to grow, management already anticipates year-over-year earnings declines later in the year. This creates difficult comparisons and raises investor concerns about the sustainability of current profitability once temporary reimbursement support expires, increasing the importance of underlying operational improvements to offset the potential revenue gap.

China Continues to Pressure Care Enablement Growth: China remains one of the company's most challenging markets due to volume-based procurement programs, stricter tender requirements and increasingly intense pricing pressure. Management indicated that China accounted for roughly half of the expected annual regulatory headwind during the first quarter and acknowledged that competitive dynamics continue evolving across the country's medical technology market.

While Fresenius Medical views China as an attractive long-term opportunity, future success depends on redesigning its product portfolio, strengthening local manufacturing capabilities and adapting its commercialization strategy. Until these adjustments are fully implemented, regulatory uncertainty and pricing pressure are likely to continue limiting revenue growth and margin expansion within the Care Enablement segment.

Estimate Trend

The Zacks Consensus Estimate for 2026 revenues is pegged at $22.94 billion, indicating 3.4% year-over-year growth. The consensus mark for earnings is pinned at $2.24 per share, implying a decline of 7.4% from the year-ago level.

Fresenius Medical Care AG & Co. KGaA Price

Fresenius Medical Care AG & Co. KGaA price | Fresenius Medical Care AG & Co. KGaA Quote

Key Picks

Some better-ranked stocks from the broader medical space are Veracyte VCYT, West Pharmaceutical WST and Intuitive Surgical ISRG.

Veracyte, currently sporting a Zacks Rank #1 (Strong Buy), reported a first-quarter 2026 adjusted earnings per share (EPS) of 52 cents, which surpassed the Zacks Consensus Estimate by 52.94%. Revenues of $139 million beat the Zacks Consensus Estimate by 6.6%. You can see the complete list of today’s Zacks #1 Rank stocks here.

VCYT has an estimated earnings growth rate of 5.1% for 2026 compared with the industry’s 14% growth. The company’s earnings beat estimates in each of the trailing four quarters, the average surprise being 45.88%.

West Pharmaceutical, currently carrying a Zacks Rank #2 (Buy), reported first-quarter 2026 EPS of $2.13, which beat the Zacks Consensus Estimate by 26.8%. Revenues of $844.9 million surpassed the Zacks Consensus Estimate by 8.5%.

WST has an estimated long-term earnings growth rate of 13.9% compared with the industry’s 9.6% growth. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 19.37%.

Intuitive Surgical, carrying a Zacks Rank of 2 at present, reported first-quarter 2026 adjusted EPS of $2.50, which beat the Zacks Consensus Estimate by 20.2%. Revenues of $2.77 billion surpassed the Zacks Consensus Estimate by 6.2%.

ISRG has a long-term estimated growth rate of 14.3% compared with the industry’s 12.5% growth. The company’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Fresenius Medical Care AG & Co. KGaA (FMS): Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

Veracyte, Inc. (VCYT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).