Hamilton Beach Brands Holding Company HBB is benefiting from a series of strategic initiatives that are reinforcing its long-term growth prospects. The company continues to execute across product innovation, premium offerings, commercial expansion and healthcare.

Hamilton Beach has also delivered notable operational improvements. The gross margin expanded 510 basis points to 29.7% in the first quarter of 2026, supported by pricing actions, a favorable product mix, sourcing efficiencies and benefits from its foreign trade zone operations. The company is reinvesting a portion of these gains into promotional and marketing initiatives to drive demand and strengthen its competitive position.

On the consumer side, Hamilton Beach is enhancing its product portfolio through launches, including innovative blender systems, a redesigned Durathon iron platform and an expanded garment steamer lineup. The company has also secured additional shelf space with major retailers while increasing investments in digital marketing, social media and AI-driven campaigns to improve brand awareness and consumer engagement.

Its premium Lotus brand is also gaining momentum. Strong double-digit sell-through following the brand's 2025 launch has prompted a key retail partner to expand shelf space ahead of the planned rollout of the Lotus Signature line later this year.

The healthcare business remains another key growth driver. The segment has delivered its third consecutive quarter of profitable growth and is targeting 50% sales growth in 2026. Hamilton Beach is expanding partnerships with pharmaceutical companies and plans to launch a pill management platform in the third quarter of 2026, further strengthening its connected healthcare portfolio.

Will Whirlpool & Electrolux Also Gain?

Whirlpool Corporation WHR and Electrolux ELUXY are also positioned to benefit from several of the same industry trends supporting Hamilton Beach. These include pricing actions, easing promotional intensity and higher tariffs on imported appliances, which may favor manufacturers with larger localized production footprints. Whirlpool, in particular, expects its U.S.-centric manufacturing base and recent pricing actions to support margin recovery as tariff-related costs become increasingly reflected in industry pricing.

Nevertheless, both companies continue to face meaningful near-term challenges. Whirlpool reported a 410-basis-point decline in first-quarter 2026 gross margin to 12.7%, while its ongoing EBIT margin fell 460 basis points to 1.3% due to tariff impacts, aggressive promotional activity and soft consumer demand. The company also expects U.S. appliance industry demand to decline 5% in 2026, indicating cautious consumer spending and continued weakness in the housing market.

Electrolux is facing similar headwinds, including subdued consumer demand, pricing pressure and elevated input costs across several key markets. While ongoing cost-reduction initiatives and premium product introductions are expected to support profitability over time, the pace of recovery will likely depend on an improvement in consumer sentiment and housing market conditions.

HBB's Price Performance, Valuation & Estimates

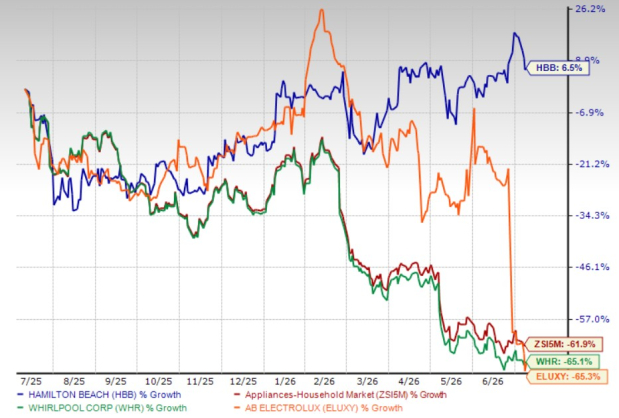

Shares of Hamilton Beachhave gained 6.5% over the past year against the industry's fall of 61.9%. The company also outperformed its peers, Whirlpool’s and Electrolux’s declines of 65.1% and 65.3%, respectively.

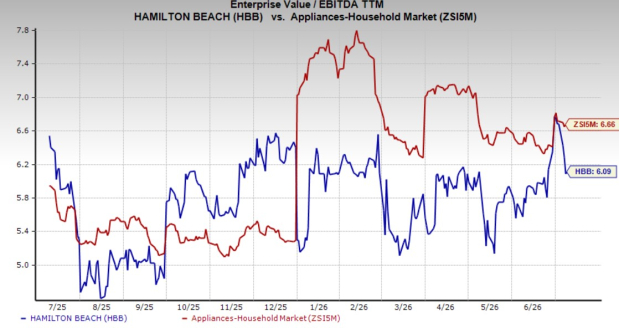

From a valuation perspective, HBB is currently trading at a trailing 12-month enterprise value-to-EBITDA multiple of 6.09X. This compares with the broader industry average of 6.66X.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Hamilton Beach Brands Holding Company (HBB): Free Stock Analysis Report

Whirlpool Corporation (WHR): Free Stock Analysis Report

Electrolux AB (ELUXY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).