Vicor VICR is scheduled to release its second-quarter 2026 results on July 21.

On May 26, this modular power components and systems provider updated its second-quarter revenue guidance from $126 million to $142 million. VICR cited rising product revenues and royalties from an additional licensee to its patented power system technology behind the revised upward guidance.

The Zacks Consensus Estimate for second-quarter 2026 revenues is currently pegged at $138.7 million, indicating 1.67% decline from the figure reported in the year-ago quarter.

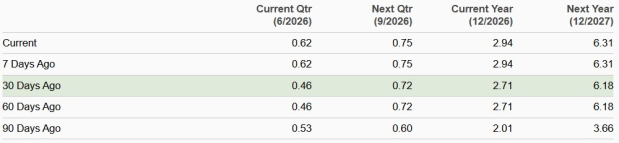

The consensus mark for earnings is pegged at 62 cents per share, up 34.8% over the past 30 days but indicates a decline of 31.87% from the figure reported in the year-ago quarter.

Consensus Earnings Trend

Image Source: Zacks Investment Research

Vicor reported earnings of 44 cents per share in the first quarter of 2026, beating the Zacks Consensus Estimate by 10%. However, revenues of $113 million lagged the consensus mark by 0.99%. The figure increased 20.2% year over year.

Vicor Corporation Price and Consensus

Vicor Corporation price-consensus-chart | Vicor Corporation Quote

Let’s see how things are shaping up prior to this announcement.

Vicor’s Q2 Earnings: Factors to Consider

Vicor’s to-be-reported quarter results are expected to have benefited from stronger product shipments combined with royalties from a newly signed licensee. In May, an OEM secured an all-inclusive license covering Vicor’s power-conversion topologies, control systems, components and distribution architectures, including Factorized Power Architecture and Vertical Power Delivery (VPD). The resulting royalty contribution, together with rising product revenues, prompted the company to raise its second-quarter 2026 guidance by $16 million.

Vicor entered the second quarter of 2026 with considerable revenue visibility. In the first quarter of 2026, book-to-bill exceeded 2, while backlog jumped 70% sequentially to $300.6 million. The company also indicated that bookings remained strong during the second quarter and expected book-to-bill to remain well above 1. Backlog growth was supported by high-performance computing customers, hyperscalers, industrial customers and aerospace and defense programs.

Demand from Vicor’s lead computing customer is likely to have remained a major second-quarter 2026 growth driver. Strong demand from hyperscaler customers and continued engagement with additional high-performance computing companies are expected to have driven top-line growth. Industrial demand should have provided another second-quarter 2026 tailwind. Vicor’s top industrial OEM customers, particularly those serving automated test and semiconductor-manufacturing equipment, have been benefiting from AI data-center investments. The company’s power modules are used in ASIC and memory test heads, pin electronics and other high-current applications. Higher geopolitical tensions, rising defense budgets and the replenishment of weapons and defensive systems are likely to have continued to support aerospace and defense orders in the to-be-reported quarter.

Higher royalty revenues should also have supported profitability because licensing carries substantially higher margins than product sales. The second-quarter 2026 gross margins are likely to have benefited from higher production volumes, improved factory utilization and a richer royalty mix. In the first quarter of 2026 gross margin reached 55.2%, up sharply from 47.2% in the year-ago quarter, reflecting higher sales, favorable product mix, royalty growth and better production efficiency.

However, manufacturing capacity constraints as well as higher tariffs and inbound freight costs are expected to have hurt top-line growth and margin expansion. The company continues to invest aggressively in Advanced Products, prototypes, manufacturing processes and VPD capacity, which is likely to have kept margins under pressure in the to-be-reported quarter.

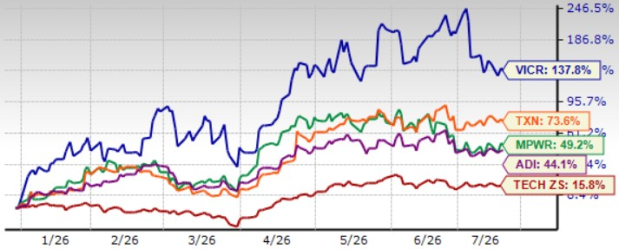

Vicor Shares Beat Sector YTD, Trades at a Premium

VICR shares have jumped a whopping 137.8% year to date (YTD), outperforming the Zacks Computer & Technology sector’s return of 15.8%. The company has outperformed competitors including Monolithic Power MPWR, Analog Devices ADI and Texas Instruments TXN over the same timeframe. Shares of Monolithic Power, Analog Devices and Texas Instruments have appreciated 49.2%, 44.1% and 73.6%, respectively, YTD.

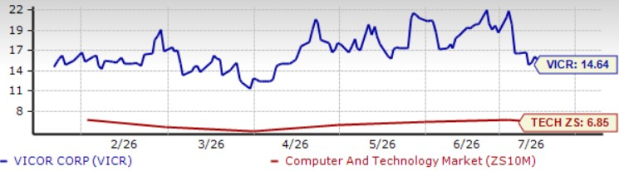

VICR Stock’s Price Performance

Image Source: Zacks Investment Research

Vicor’s Value Score of F suggests a premium valuation at this moment.

In terms of the forward 12-month price/sales (P/S), VICR is trading at 14.64X, higher than the broader sector’s 6.85X and Analog Devices’ 11.99X. However, Vicor is trading at a discount compared with Monolithic Power’s 16.17X and Texas Instruments’ 12.54X.

VICR Shares Trade at a Premium

Image Source: Zacks Investment Research

AI, Licensing and Capacity Drive Vicor’s Future Growth

Vicor’s long-term growth is supported by several structural drivers. The adoption of second-generation VPD positions the company to benefit from the rising power demands of next-generation AI processors. Expansion of VICR’s IP licensing business creates a high-margin, recurring revenue stream while extending the reach of its patented technologies.

Meanwhile, investments in manufacturing capacity should enable Vicor to meet growing demand and support larger hyperscale customers. Continued AI infrastructure spending is expanding opportunities across data centers and high-performance computing, while diversified exposure to industrial, semiconductor test, aerospace and defense markets reduces dependence on any single end market and supports more resilient long-term growth.

Conclusion

Vicor enters its second-quarter earnings report with strong operational momentum, supported by accelerating AI infrastructure demand, expanding royalty revenues and a record backlog. The upward revision to revenue guidance suggests that product shipments and licensing income are tracking ahead of earlier expectations. However, investors will also be watching whether manufacturing capacity constraints, tariff-related costs and elevated investment spending limit near-term margin expansion. While the stock’s premium valuation leaves little room for disappointment, Vicor’s growing exposure to AI power delivery, IP licensing and hyperscale customers continues to strengthen its long-term growth outlook.

Vicor currently has a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vicor Corporation (VICR): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).