HealthEquity, Inc. HQY has been gaining from its business model and strategy. The optimism, led by a solid first-quarter fiscal 2027 performance and strength in Health Savings Accounts (HSAs), is expected to contribute further. However, data security threats are major concerns.

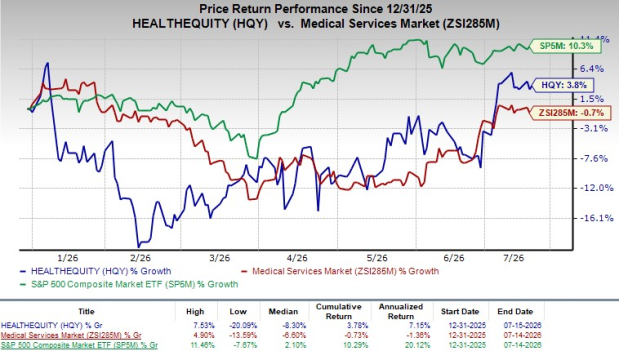

In the year-to-date period, this Zacks Rank #3 (Hold) company’s shares have gained 3.8% against the 0.7% decline of the industry. The S&P 500 has increased 10.3% during the said time frame.

The renowned provider of technology-enabled services platforms for healthcare savings and spending decisions has a market capitalization of $7.9 billion. The company projects 15.2% growth over the next five years and expects to witness continued improvements in its business. HealthEquity’s earnings surpassed the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 12.02%.

Image Source: Zacks Investment Research

Reasons Favoring HQY’s Growth

AI & Digital Innovation Drive Scalable Efficiency:In the first quarter of fiscal 2027, management said AI-driven tools reduced manual handling of member and client service emails by 25%. In targeted workflows such as card servicing and claims inquiries, AI-enabled automation reduced manual efforts by more than 90% and accelerated processing times by up to 50%. These initiatives are being paired with continued technology and security investments embedded in the raised fiscal 2027 outlook, suggesting management intends to keep pushing automation while sustaining service quality.

Expansion of Health Savings Accounts: HealthEquity has experienced significant growth in its HSA offerings. As of April 30, 2026, the total number of HSAs for which HealthEquity served as a non-bank custodian was 10.6 million, up 8% year over year.

HealthEquity reported 909,000 HSAs with investments as of April 30, 2026, up 18% year over year. Total accounts, as of April 30, 2026, were 17.8 million. This uptick included total HSAs and 7.2 million Consumer Direct Benefits (CDBs).

Total HSA assets were $37.1 billion at the end of April 30, 2026, up 19% year over year. This included $17.5 billion of HSA cash and $19.6 billion of HSA investments. This figure compares with our fiscal first-quarter HSA cash and HSA investments projection of $17.6 billion and $17.9 billion, respectively. We projected total HSA assets of $35.5 billion for the fiscal first quarter.

Client-held funds, which are deposits held on behalf of HealthEquity’s clients to facilitate the administration of its CDBs and from which the company generates custodial revenues, were $1 billion as of April 30, 2026.

Strong Fiscal Q1 Results: HealthEquity exited first-quarter fiscal 2027 with better-than-expected results. The company witnessed solid top and bottom-line performances in the reported quarter. Solid growth in HSAs also drove the top line. The solid uptick in total HSA assets in the reported quarter is promising. Improvements in operating and gross margins also bode well.

Management noted that the company opened approximately 172,000 new HSAs during the quarter. The company noted that it outpaced industry HSA growth, supported by strong client retention, an active enterprise sales pipeline and continued adoption of HSA-qualified plans.

Management also emphasized that digital engagement continues to strengthen, with monthly active mobile usage surging 90% year over year. The increased use of the mobile platform is helping improve member engagement, boost investing activity and support marketplace adoption, all of which are expected to enhance long-term member lifetime value.

Factor That May Offset HQY’s Gains

Data Security Threats: HealthEquity manages sensitive personal data and large custodial balances, which keeps cybersecurity risk elevated despite recent progress in fraud reduction. The company remains subject to a consolidated putative class action related to a fiscal 2025 cybersecurity incident involving a business partner’s user account and is also subject to regulatory inquiries connected to that incident.

In May 2026, the company filed a renewed motion to compel arbitration, and the potential loss associated with the lawsuit and any regulatory action was not reasonably estimable based on available information. Any adverse outcome could increase costs, create operational distraction and impact member and client confidence, which can weigh on the long-term margin and growth profile.

Estimate Trend

HealthEquity has been witnessing a stable estimate revision trend for fiscal 2027. Over the past 30 days, the Zacks Consensus Estimate for earnings per share (EPS) has remained stable at $4.71.

The Zacks Consensus Estimate for second-quarter fiscal 2027 revenues is pegged at $350.2 million, implying a 7.5% rise from the year-ago reported number. The consensus mark for fiscal second-quarter EPS is pinned at $1.19, implying a 10.2% improvement year over year.

Key Picks

Some better-ranked stocks from the broader medical space are West Pharmaceutical WST, Intuitive Surgical ISRG and Cardinal Health CAH, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

West Pharmaceutical reported first-quarter 2026 earnings per share of $2.13, which beat the Zacks Consensus Estimate by 26.8%. Revenues of $844.9 million surpassed the Zacks Consensus Estimate by 8.5%.

West Pharmaceutical has an estimated long-term earnings growth rate of 13.9%. WST’s earnings surpassed estimates in the trailing four quarters, the average surprise being 19.4%.

Intuitive Surgical reported first-quarter 2026 adjusted EPS of $2.50, which beat the Zacks Consensus Estimate by 20.2%. Revenues of $2.77 billion surpassed the Zacks Consensus Estimate by 6.2%.

Intuitive Surgical has an estimated long-term earnings growth rate of 14.3%. ISRG’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 16.8%.

Cardinal Health reported a third-quarter fiscal 2026 adjusted EPS of $3.17, which beat the Zacks Consensus Estimate by 13.2%. Revenues of $60.94 billion missed the Zacks Consensus Estimate by 2.3%.

Cardinal Health has an estimated long-term earnings growth rate of 17%. CAH’s earnings surpassed estimates in the trailing four quarters, the average surprise being 10.3%.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

HealthEquity, Inc. (HQY): Free Stock Analysis Report

Intuitive Surgical, Inc. (ISRG): Free Stock Analysis Report

Cardinal Health, Inc. (CAH): Free Stock Analysis Report

West Pharmaceutical Services, Inc. (WST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).