Vicor VICR is drawing investor attention as AI systems require denser and more efficient power delivery. The company’s role is not in processors themselves, but in helping those processors receive power more effectively.

That makes Vicor’s outlook a mix of demand, manufacturing execution and intellectual property monetization. The opportunity is clear, but so are the operating constraints.

How Vicor Fits the AI Power Stack

Vicor designs modular power components and systems used to convert electrical power across data centers, transportation, military and industrial markets. Its core strength is high-density AC and DC power conversion, including 48V distribution.

This matters as AI accelerators, GPUs and custom ASICs push processor power density higher. Monolithic Power Systems MPWR is a relevant peer in power-management semiconductors.

Advanced Products have become the main AI-linked growth engine. They accounted for 61% of Vicor’s net revenues in 2025, with demand concentrated in data center and hyperscaler computing.

VICR’s Growth Drivers Are Getting Clearer

The bullish case rests on order strength and a widening backlog. In the first quarter of 2026, Vicor’s book-to-bill ratio was above 2, showing that orders were more than twice the value of products shipped.

The one-year backlog reached $300.6 million, up 70% sequentially. Management also expects 2026 revenues of nearly $570 million, supported by AI-driven demand and a lead computing customer continuing a steep production ramp.

Advanced Products and royalties are central to that outlook. Royalty revenues were about $15 million in the first quarter, while product revenue rose to $98 million.

Why Vicor’s Factory Plan Matters

Demand is no longer the only question. The bigger swing factor is whether Vicor can convert orders into shipments without straining its operations.

Management expects the company to remain capacity constrained for a substantial period. Near-term capacity is tight, and the second 3Di line is expected to be installed in the third-to-fourth-quarter time frame of 2026.

The company is trying to add flexibility inside its existing footprint. Vicor raised its Fab 1 annual revenue capacity target to at least $1.5 billion from roughly $1 billion through cycle-time reductions, debottlenecking and moving some process steps to a nearby Vicor-controlled site.

Vicor’s Licensing Adds a Second Lever

Licensing gives Vicor a second earnings lever beyond product shipments. The company licenses technology and receives recurring royalties, which can support margins without requiring the same manufacturing volume.

Management’s 2026 revenue outlook assumes no new licensing agreements before the second International Trade Commission case reaches final determination in 2027. That leaves possible upside if enforcement actions lead to earlier agreements.

Still, licensing is harder to model than product demand. Legal outcomes, agreement timing and enforcement costs can make the profit contribution uneven.

What Could Hold VICR Back

The main risk is execution. Strong end-market demand does not automatically translate into smooth revenue recognition when capacity is constrained. Customer timing also matters. Vicor’s shift toward larger high-volume customers can improve scale, but it raises exposure to forecast changes from original equipment manufacturers, original design manufacturers and contract manufacturers.

Tariff and geopolitical risks add another layer. The company incurred approximately $7.4 million of tariff expenses in 2025 and still generates meaningful revenues from international markets. Legal spending is another watch item. First-quarter operating expenses rose sequentially to $45.5 million, including higher costs tied to intellectual-property enforcement.

Apart from Monolithic Power, Vicor faces stiff competition from the likes of Texas Instruments TXN and Analog Devices ADI in power management. Monolithic Power is Vicor’s closest direct competitor in AI power delivery, offering highly integrated power management ICs and multiphase regulators that have won significant GPU and AI server designs through strong integration and cost advantages. Analog Devices and Texas Instruments are much larger diversified analog semiconductor companies with broad portfolios spanning industrial, automotive, communications and embedded markets.

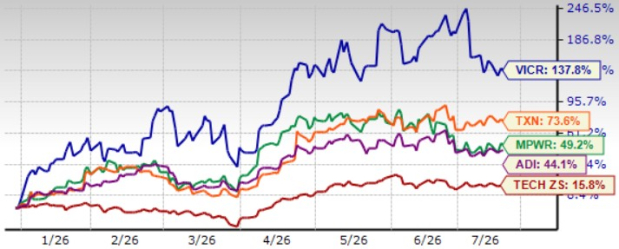

On a year-to-date (YTD) basis, Vicor has outperformed Monolithic Power, Analog Devices and Texas Instruments. Shares of Monolithic Power, Analog Devices and Texas Instruments have appreciated 49.2%, 44.1% and 73.6%, respectively, while Vicor has jumped 137.8%, YTD.

VICR Stock's Price Performance

Image Source: Zacks Investment Research

Conclusion

The bottom line is that Vicor has a credible AI power-delivery story, but the stock is not a clean one-way trade. Demand, backlog and licensing all point to growth potential, while capacity and legal timing keep execution risk high.

VICR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vicor Corporation (VICR): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).