Vicor VICR has become one of the more dramatic AI infrastructure stories in the power-components space. The stock’s surge reflects better demand, stronger backlog and improving earnings trends.

The question is no longer whether the business has momentum. It is whether the stock still offers enough room for new buyers after a major rerating.

VICR’s Rally Has Raised the Bar

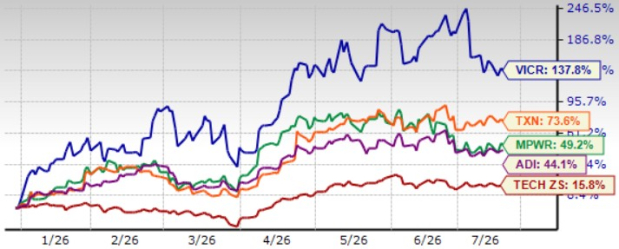

VICR shares have jumped a whopping 137.8% year to date (YTD), outperforming the Zacks Computer & Technology sector’s return of 15.8%. The company has outperformed competitors, including Monolithic Power MPWR, Analog Devices ADI and Texas Instruments TXN over the same timeframe. Shares of Monolithic Power, Analog Devices and Texas Instruments have appreciated 49.2%, 44.1% and 73.6%, respectively, YTD.

VICR Stock’s Price Performance

Image Source: Zacks Investment Research

A move that large can be justified when fundamentals improve, but it also raises expectations. For VICR, the market is already pricing in stronger AI demand, higher capacity utilization and smoother conversion of backlog into revenues.

Vicor’s Value Score of F suggests a premium valuation at this moment.

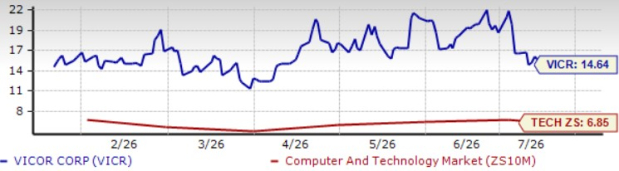

In terms of the forward 12-month price/sales (P/S), VICR is trading at 14.64X, higher than the broader sector’s 6.85X and Analog Devices’ 11.99X. However, Vicor is trading at a discount compared with Monolithic Power’s 16.17X and Texas Instruments’ 12.54X.

VICR Shares Trade at a Premium

Image Source: Zacks Investment Research

The $273 price target is above the cited stock price of $260.20, but the implied upside is modest. That makes the setup more selective, even though end-market demand remains favorable.

VICR’s Earnings Story Has Real Strength

Vicor reported first-quarter 2026 earnings of 44 cents per share, beating the Zacks Consensus Estimate by 10%. Earnings rose sharply from 6 cents in the year-ago quarter.

Revenues increased 20.2% year over year to $112.97 million. Gross margin expanded 800 basis points to 55.2%, while royalty revenues grew 39.1% to $14.97 million.

On May 26, Vicor updated its second-quarter revenue guidance from $126 million to $142 million. VICR cited rising product revenues and royalties from an additional licensee to its patented power system technology behind the revised upward guidance.

The Zacks Consensus Estimate for second-quarter 2026 revenues is currently pegged at $138.7 million, indicating 1.67% decline from the figure reported in the year-ago quarter.

The consensus mark for earnings is pegged at 62 cents per share, up 34.8% over the past 30 days but indicates a decline of 31.87% from the figure reported in the year-ago quarter.

Vicor Corporation Price and Consensus

Vicor Corporation price-consensus-chart | Vicor Corporation Quote

Where the Bull Case Gets Less Comfortable for VICR

Demand is not the main problem, execution is. Management has described near-term capacity as essentially sold out, while a second three-dimensional interconnect line is expected to matter more in late 2026 and beyond.

Growth now depends on debottlenecking, cycle-time gains and relocating selected process steps before larger capacity additions arrive. Customer concentration is another risk because large original equipment manufacturer, original design manufacturer and contract manufacturing forecasts can change quickly.

Margin quality also needs context. Royalties and litigation-related items have helped profitability, while legal spending tied to intellectual-property enforcement has risen. That can make margins uneven even when product demand is healthy.

How to Read Vicor’s Risk-Reward Now

Vicor offers direct exposure to a critical AI constraint, namely dense and efficient power delivery. Analog Devices is a broader analog and power-management peer with data-center exposure, while Monolithic Power provides another comparison point for investors watching advanced power solutions.

VICR also has a cash-rich balance sheet, ending the first quarter with $404.25 million in cash and cash equivalents. That gives the company flexibility to fund manufacturing expansion, research and development, and intellectual-property efforts.

Still, the stock-selection case is less obvious than the operating story. Investors are paying a premium for backlog support, AI optionality and licensing leverage before the timing and scale of throughput improvements are fully proven.

Conclusion

The bottom line is that Vicor looks operationally attractive but no longer obviously cheap. The company has strong demand signals, improving estimates and a balance sheet that supports expansion, but valuation and execution risk limit the margin for error.

VICR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vicor Corporation (VICR): Free Stock Analysis Report

Analog Devices, Inc. (ADI): Free Stock Analysis Report

Texas Instruments Incorporated (TXN): Free Stock Analysis Report

Monolithic Power Systems, Inc. (MPWR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).