Moving iMage Technologies, Inc. MITQ shares have gained 17.2% over the past month against the industry’s 2.1% decline. The company has outperformed other industry players, including Parsons Corporation PSN and Aduro Clean Technologies Inc. ADUR. Shares of PSN have rallied 3.3%, while ADUR stock has declined 8.2% in the same time frame. MITQ is benefiting from the QSC Digital Cinema Speaker Series (DCS) acquisition, premium cinema upgrade demand, higher-margin product mix, diversified solutions, expanding international reach, and improving operational execution.

Image Source: Zacks Investment Research

A Key Look at MITQ’s Business Operations

MiT, originally incorporated as MiT Acquisition Corporation in 2020, provides technology, products, software, and technical services for movie theaters, sports venues and entertainment facilities. The company delivers end-to-end project management, including design, integration, installation, procurement, and refurbishment, while manufacturing proprietary products such as automation systems, LED lighting, power management solutions, accessibility equipment, and projection components. It also distributes leading third-party cinema technologies, including projectors, servers, audio systems, and screens. Its CineQC SaaS platform enables real-time monitoring, remote control, and operational reporting to improve theater performance and efficiency.

MiT’s Key Tailwinds

MiT is benefiting from the strategic acquisition of QSC's DCS, which expands its presence in the premium cinema audio market. Management views DCS as a long-term growth driver capable of strengthening customer relationships, broadening international reach, and generating higher-margin revenue. Early customer reception has been encouraging, reinforcing confidence in the acquisition's strategic value and its ability to support future revenue expansion.

The company's profitability is improving as its revenue mix shifts toward higher-margin products. During the first nine months of fiscal 2026, gross margin expanded to 31.5% from 27.5% a year earlier, driven by stronger DCS sales and the benefit of discounted inventory acquired through the QSC transaction. Management expects the remaining acquired inventory and future DCS shipments to continue supporting above-average margins, providing a favorable earnings profile even if revenue growth remains gradual.

Industry trends continue to create attractive growth opportunities for the company. Cinema operators are investing in premium large-format auditoriums, immersive audio systems, and laser projection upgrades to enhance the moviegoing experience. These modernization initiatives align well with MiT's integrated engineering, design, installation, and proprietary technology offerings, positioning the company to participate in a multi-year cycle of cinema infrastructure upgrades.

MiT is also expanding its addressable market through a broader portfolio of products and services. Alongside proprietary hardware, the company offers third-party equipment, SaaS-based theater management solutions, remote monitoring, accessibility technologies and language translation solutions. This diversified offering enhances cross-selling opportunities, supports larger integrated projects, deepens customer relationships, and provides access to new international distribution channels.

Operational execution has strengthened the company's financial outlook. For the first nine months of fiscal 2026, revenues increased 4.1%, gross profit rose 19.3%, and the company nearly achieved breakeven results due to stronger margins and disciplined cost management. Management also expects seasonal improvement in customer activity during the fourth quarter, supported by a growing DCS backlog and projected quarterly revenues of approximately $5.3 million, providing additional momentum for future performance.

Challenges Persist for MITQ’s Business

MiT faces several headwinds, including soft and seasonal customer project activity that pressured quarterly revenues, dependence on one-time cinema projects that can cause order and earnings volatility, and uncertainty around cinema industry spending. The company also remains exposed to pricing pressure, competitive dynamics, tariff and trade-policy risks that could increase input costs, supply-chain disruptions, labor shortages, and delays in content production or theater upgrades. Additionally, elevated inventory following the DCS acquisition reduced cash balances and increased working-capital usage.

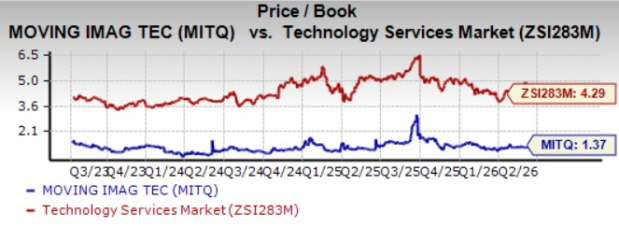

MiT’s Valuation

The company is cheaply priced compared with the industry average. Currently, MITQ is trading at 1.37X trailing 12-month price/book value, below the industry’s average of 4.29X. The metric also remains lower than that of the company’s peers, Parsons (2.2X) and Aduro Clean Technologies (15.58X).

Image Source: Zacks Investment Research

Conclusion

Despite soft and seasonal customer project activity, competitive and tariff-related pressures, supply-chain risks, and elevated working-capital requirements, MiT is supported by the strategic DCS acquisition, an expanding higher-margin product mix, favorable cinema modernization trends, a broader portfolio of integrated solutions, and improving operational execution.

Strong fundamentals, coupled with MITQ’s undervaluation, present a lucrative opportunity for investors to add the stock to their portfolios.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Parsons Corporation (PSN): Free Stock Analysis Report

Moving iMage Technologies, Inc. (MITQ): Free Stock Analysis Report

Aduro Clean Technologies Inc. (ADUR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).