Most investors are wondering which tech titan will eventually win the artificial intelligence (AI) race. However, I believe there may not be one single winner, as the AI ecosystem is too large and too complex for one company to dominate everything. AI is actually several massive markets stacked together.

Today, Nvidia (NVDA) has the dominant position in chips, while Amazon (AMZN) controls the cloud. Meanwhile, Alphabet (GOOGL) has the data advantage, and Meta Platforms (META) holds a massive scale of users. But this is where Taiwan Semiconductor Manufacturing Company (TSM) — or TSMC — becomes fascinating. Even as all of these tech titans win simultaneously, TSMC is a winner, too.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Why TSMC Holds All the Cards

Valued at a market capitalization of $2.1 trillion, TSMC manufactures the advanced semiconductor chips that companies like Nvidia, Apple (AAPL), AMD (AMD), Google, Amazon, and Microsoft (MSFT) design. Some of the world's most sophisticated chips currently manufactured by TSMC include the Nvidia Blackwell GPU, Apple M4, Apple A18 Pro, Amazon's Trainium AI chips, and AMD Instinct MI350, among others. In fact, the more aggressively these tech giants compete against each other, the more chips they need and the more business TSMC receives. So, the stronger they get, the more TSMC's profits grow.

In the first quarter of fiscal 2026, revenue climbed almost 41% year-over-year (YOY) to $35.9 billion, while EPS surged more than 58%. The company’s high-performance computing (HPC) segment, which powers AI workloads, accounted for 61% of total revenue.

Building a leading-edge semiconductor fab is expensive and complex. A tiny defect can ruin an entire chip, and TSMC has mastered this process. It can manufacture millions of these chips with extremely high yields (percentage of working chips coming off the production line). This makes the company irreplaceable. Additionally, TSMC spends billions of dollars in capital expenditures. It intends to spend $52 billion to $56 billion in 2026. Most competitors cannot afford that level of spending year after year while maintaining profitability. This creates a huge barrier to entry. Despite the massive investments, TSMC also holds one of the strongest balance sheets in the semiconductor industry, with $106 billion in cash and marketable securities.

Currently, the strongest competitor for TSMC is Samsung Electronics. Samsung has a plethora of resources and advanced manufacturing technology. Yet, it hasn’t been able to match TSMC's reputation of reliability, on-time delivery, higher yield, and manufacturing consistency. Intel (INTC) is also investing heavily to become a foundry competitor. But it could take a while to catch up to Taiwan Semiconductor. And the AI boom, in particular, is strengthening TSMC's position as every AI company now wants faster, more efficient, and more advanced chips. In fact, in Q1, technologies at 7 nanometers accounted for just 13% of the firm's wafer revenue, while 5nm and 3nm represented 36% and 25%, respectively.

Massive Expansion Plans for N2 and A14

N2, TSMC's most advanced node, is in high-volume manufacturing with strong demand from both smartphone and HPC/AI customers. Many future flagship chips from companies like Qualcomm (QCOM), Apple, Nvidia, and AMD are expected to migrate to N2. Management believes the N2 family will become “another large and long-lasting node" for the company. This implies that customers could most likely build multiple generations of products around the N2 ecosystem, which could extend N2’s revenue potential well into the future.

While N2 is just beginning its ramp, TSMC is already preparing for its next-generation A14 technology. This even more advanced node is scheduled for volume production in 2028. Management is confident that “compared with N2, A14 will provide 10% to 15% speed improvement at the same power for 25% to 30% power improvement at the same speed and close to 20% chip density gain.” The company believes when A14 goes into production, it is likely to become the world's most advanced commercial semiconductor manufacturing technology.

As AI models become more advanced, the need for cutting-edge manufacturing increases. Management even mentioned that not only its customers but also its customers' customers — particularly cloud service providers — continue to provide very strong signals regarding future AI demand. As a result, TSMC now expects more than 30% revenue growth in 2026, with analysts forecasting a 44% increase in earnings.

Simply put, TSMC is more of an enabler of the AI race than a participant. Whether one or all of its customers win, TSMC will continue to benefit for a long time.

What Do Analysts Think of TSM Stock?

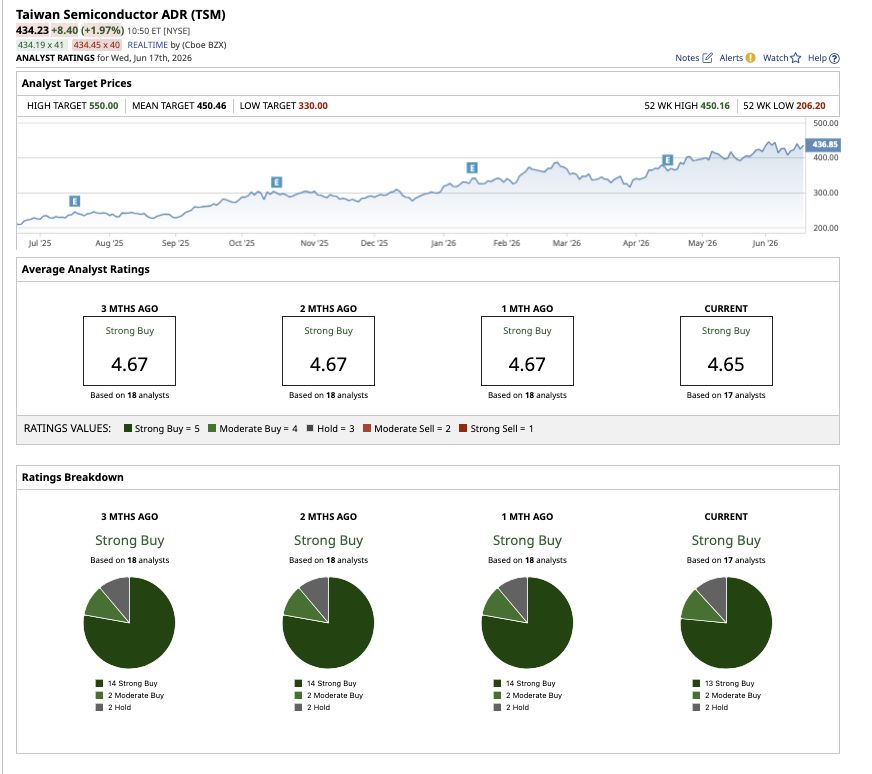

On Wall Street, TSMC holds a consensus “Strong Buy” rating. Out of 17 analysts with coverage, 13 rate TSM stock as a “Strong Buy,” two have a “Moderate Buy" rating, and two analysts offer a “Hold" rating. TSM stock has surged 52% year-to-date (YTD), outpacing the overall market's gain. Shares have surpassed the average price target of $450.46, while the high target price of $550 implies potential upside of 19% over the next 12 months.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Why TSMC Doesn’t Even Need to Win the AI Race Cathie Wood Loads Up on SpaceX Stock. She Is Betting Big That Musk’s AI Vision Will Pay Off. Michael Burry Thinks the Market Has Adobe Stock Wrong. What Management Needs to Do to Prove Him Right. Nothing Seems to Be Going Right for Meta Platforms. How to Play META Stock Here.