Taiwan Semiconductor Manufacturing Company (TSM), commonly known as TSMC, is the world’s largest and most advanced semiconductor foundry. The company is known for producing chips for giants like Apple (AAPL), Nvidia (NVDA), AMD (AMD), and Qualcomm (QCOM), building its position as an irreplaceable center of global AI infrastructure. TSMC operates across leading-edge process nodes, including 3-nanometer and 5nm, and it leads over 90% of the advanced foundry market for 7nm and below.

Let's take a closer look at what's going on with TSM stock as the company's upcoming earnings report approaches on July 16.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

About Taiwan Semiconductor Stock

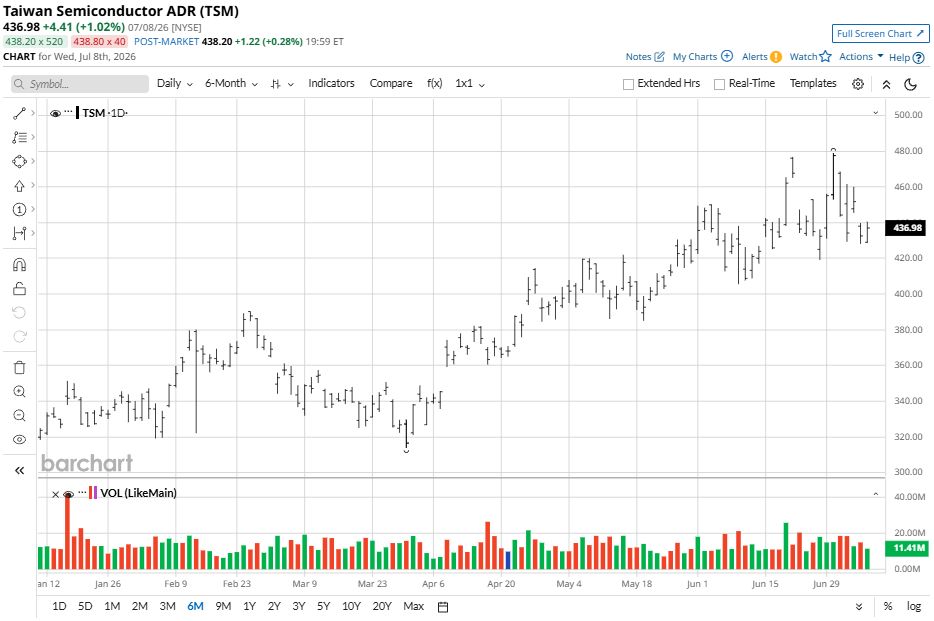

TSM stock has gained approximately 89% over the last 52 weeks, recently setting a high of $479 in late June. Shares are also up 94% from the 52-week low of $223.70 per share. Currently, the stock trades near the $434 mark, having gained roughly 43% on a year-to-date (YTD) basis.

Next to the S&P 500 Information Technology Index ($SRIT), which has posted strong but comparatively modest gains in 2026, TSM stock has dramatically outperformed the benchmark. TSMC has emerged as a standout in the global semiconductor space as AI-driven wafer demand and advanced node pricing power continue to expand its profitability and market dominance.

www.barchart.com

www.barchart.com Taiwan Semiconductor Posts Blockbuster Results

Taiwan Semiconductor posted first-quarter 2026 results on April 16, showing revenue of $35.9 billion, up 41% year-over-year (YOY) and more than 6% sequentially. This surpassed its own guidance range of $34.6 billion to $35.8 billion while also topping analyst estimates of $35.5 billion. Earnings came in at NT$22.08 or $3.49 per ADR, beating estimates, while net income spiked 58% YOY.

Gross margin for the quarter expanded to 66.2%, operating margin touched 58.1%, and net profit margin expanded to 50.5%, strengthened by a favorable technology mix with 3nm at 25% of wafer revenue, 5nm at 36%, and 7nm at 13%. A whopping 74% of total revenue originated from advanced technology of 7nm and below.

For the upcoming Q2 results, scheduled to be released on July 16, the company guided revenue between $39 billion and $40.2 billion with a gross margin of 65.5% to 67.5%. Management indicated that 3nm gross margins are expected to cross over to corporate average levels in the second half of 2026, supporting continued margin expansion.

Full-year 2026 revenue growth is projected to be above 30% in U.S. dollar terms. Capital expenditures are also expected to remain elevated toward the high end of $52 billion to $56 billion for 2026, reflecting TSMC's commitment to expanding AI capacity across its global fab network, with Arizona Phase 1 already producing 4nm chips for Apple and Phase 2 on track for 2nm production.

GF Securities Is Bullish on Q2 results

Taiwan Semiconductor is expected to raise its full-year revenue guidance and signal higher 2027 capital expenditures at its upcoming Q2 analyst meeting on July 16, according to GF Securities analyst Jeff Pu. The analyst recently reiterated a “Buy” rating on shares and raised his price target to NT$2,900 from NT$2,808. Pu anticipates that Q2 revenue will grow 11% sequentially, with gross margin reaching approximately 68%, above the company's guided range. The broader analyst consensus projects TSMC to report Q2 adjusted EPS of $3.83 on revenue of $39.3 billion.

For Q3, GF Securities also estimates revenue growth of 13% sequentially, materially ahead of the consensus estimate of 9%. Full-year 2026 capex is projected at $56 billion, while GF Securities expects 2027 capex to accelerate to $73 billion as Taiwan Semiconductor ramps capacity additions in the second half of next year.

Is TSM Stock Still a Buy Ahead of Earnings?

GF Securities' bullish expectations reinforce TSMC's position as the irreplaceable backbone of global AI infrastructure, with pricing power and margin expansion firmly intact.

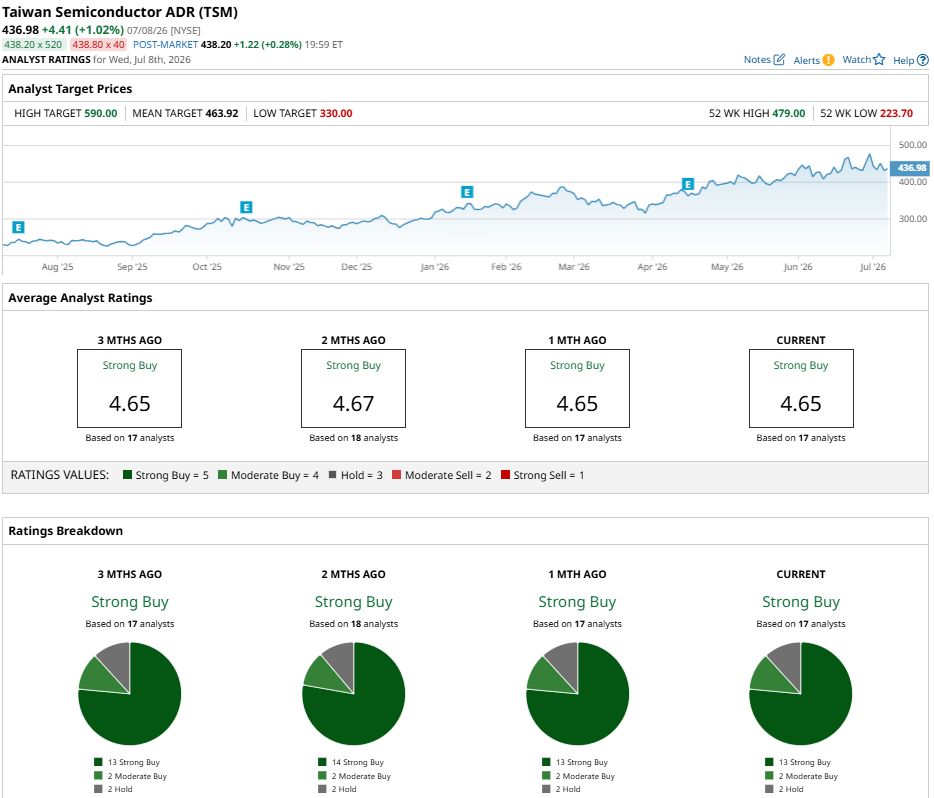

Wall Street broadly agrees. TSM stock holds a consensus “Strong Buy” rating across 17 analysts. That breaks down to 13 “Strong Buy” ratings, two “Moderate Buy” ratings, and two “Hold” ratings. The mean price target of $463.92 implies modest potential upside of 7% from current levels, suggesting TSM stock is approaching fair value but remains a high-conviction long-term compounder.

www.barchart.com

www.barchart.com On the date of publication, Ruchi Gupta did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Forget GPUs. Nvidia’s Next AI Gold Mine Could Be Even Bigger. Taiwan Semi Stock Is Approaching Fair Value Ahead of July 16. How to Play TSM Here. The U.S. Is Considering Removing Steering Wheels From Cars. Tesla Is the Reason Why. Nvidia Stock Hasn’t Been This Cheap Since Before 2019. How to Play NVDA Stock Here.