This article extends the MQL5 RQA library to Cross-Recurrence Quantification Analysis (CRQA) for comparing two time series. We implement dual‑series embedding, cross‑recurrence matrix construction, adapted metrics (CRR, CDET, CLAM, CENTR, and others), and rolling‑window analysis, with optional GPU acceleration via OpenCL. A ready-to-use indicator compares two symbols in real time, supporting timestamp alignment and normalization for practical inter-market analysis.

This work presents an end-to-end pipeline: collect MetaTrader 5 data, engineer entropy/volatility/trend features, train a PyTorch classifier, and expose predictions through a Flask API. An MQL5 EA posts rolling prices each tick, receives probability and regime, and applies adaptive position sizing and stop distances. The result is a clear recipe for integrating ML inference with MetaTrader 5.

This article presents a custom MQL5 signal class, CSignalBitwisePerceptron, for ultra-lightweight entry logic. It packs 64 bars into a single uint64 via bitwise vectorization and evaluates them with a perceptron that sums weights only for active bits. A two-gate flow (algorithmic hash map plus neural threshold) minimizes array iteration and heavy math. Readers get a practical template to cut latency and refine entry validation.

This article starts the MMAR pipeline on EURUSD M5 data. We load market data via the MetaTrader5 Python API and run partition-function analysis with non-overlapping intervals to test for multifractal scaling. The result is an evidence-based decision on fractality, a prerequisite for building MMAR and for choosing whether to proceed beyond GARCH.

This article presents CPyramidEngine, a reusable MQL5 class that adds disciplined pyramiding to any Expert Advisor with about six lines of integration. The engine enforces three constraints: strictly decreasing lot sizes, a single unified stop that advances after each add-on, and broker-level validation of every modification. It explains common failure modes in naive implementations and shows how to keep total account risk quantifiable and controlled as positions are added.

We turn the Tools Palette sidebar from a static shell into an interactive MQL5 system. The article implements flyout menus per category, a chart event handler, a multi-click drawing engine (one-, two-, and three-click tools), and mouse interactions including drag, bottom-edge resize, scrolling, hover states, and live theme toggling. You will be able to select a tool and place chart objects directly from the palette for analysis

This article extends a Flask backend to reliably receive, validate, and store closed trade data from MetaTrader 5 using SQLite and Flask‑SQLAlchemy. It implements required‑field checks, timestamp conversion, transaction‑safe persistence, and working retrieval endpoints for all trades and single records, plus a basic summary. The result is a complete data pipeline with local testing that records trades and exposes them through a structured API for further analysis.

The article describes the arrangement of a coordinated ML pipeline in MetaTrader 5 with separation of roles: Python trains and exports the model to ONNX, MQL5 reproduces normalization and PCA via matrix/vector and performs inference. This approach makes the model's inputs stable and verifiable, and the MetaTrader 5 strategy tester provides metrics for analyzing the system behavior.

The article addresses the loss of temporal information in ML pipelines by encoding periodic time variables with Fourier harmonics and adding forex session structure. It implements session and overlap flags, lagged session volatility, and calendar effects, then prunes features by timeframe. The get time features function returns an index‑aligned, ML‑ready set of time features suitable for integration with price‑based signals.

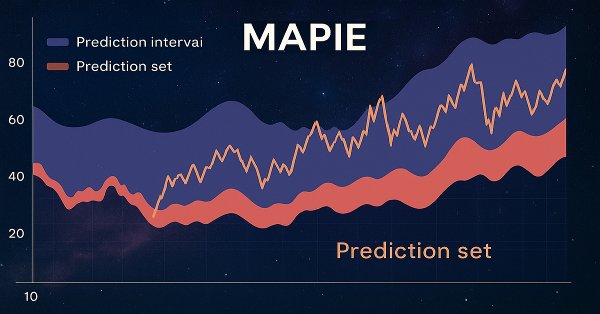

In this article, we will consider conformal predictions and the MAPIE library that implements them. This approach is one of the most modern ones in machine learning and allows us to focus on risk management for existing diverse machine learning models. Conformal predictions, by themselves, are not a way to find patterns in data. They only determine the degree of confidence of existing models in predicting specific examples and allow filtering for reliable predictions.

Learn to engineer an MQL5 indicator that converts trend, momentum, and volatility into a single raw score using a matrix.mqh (ALGLIB). The article covers a separate‑window oscillator to validate the core mathematics, then a main‑chart indicator that plots non‑repainting buy/sell arrows when the score crosses user‑defined thresholds. An optional long‑term EMA filter, a minimum‑bar cooldown, and built‑in alerts make the tool practical for live trading.

This article applies the Optimal Trading Rule from AFML Chapter 13 to set profit targets and stop-losses without in-sample calibration. We model post-entry P&L with a discrete Ornstein–Uhlenbeck process, run a 100,000-path search, and implement Python, multiprocessing, and a Numba @njit parallel kernel (242× faster). The result is an optimal (PT, SL) under three forecast specifications, constrained by the prop-firm daily loss limit.

The article replaces hardcoded cost assumptions in triple-barrier labeling with measured inputs. An MQL5 script captures spread distribution, swap rates, and symbol metadata from your broker, and a Python model converts them into a broker-calibrated min ret you can pass to get events. Labels then reflect the actual round-trip friction for your instrument and holding period.

We refactor the Tools Palette from a flat, function-based panel into a modular, class-driven sidebar in MQL5. The design introduces supersampled canvas rendering for anti-aliased shapes, theme control, a category registry, snap alignment, and selective corner rounding. The result is a reusable, scalable sidebar foundation that you can extend with tool selection, dragging, and fly-out menus in future steps.

This article builds the foundation layer of a twelve-part MQL5 market microstructure toolkit. It implements guarded math helpers (SafeDivide, SafeLog, SafeSqrt, SafeExp, SafeTanh), robust data validation (ValidateSymbolV2, SafeCopyClose), trimmed statistical estimators (robust mean var), a linear regression slope, shared structs, and an FFT. You compile a single include file that hardens indicators and expert advisors against silent numerical failures and standardizes data flow for later parts.

This article tests three common filters on a standard MACD crossover for US_TECH100 H1 using five years of broker-native data. Filters are layered incrementally: regime, higher timeframe (HTF) alignment, and US session timing, to isolate each one's marginal impact. Results show session timing contributes far more than indicator refinements, while regime and HTF add little on their own. Includes a reproducible MQL5 regime classifier.

The article replaces clock-based sampling with López de Prado's alternative bar types and provides two aligned implementations: a unified Python module for batch tick histories and an object‑oriented MQL5 library for live EAs. It covers Parquet/Dask infrastructure, data cleaning, and a single API. Practical issues are solved explicitly: zero‑tick time‑bar filtering, imbalance threshold initialization, EWM state persistence, and parity between Python and MQL5 outputs.

Higher-timeframe CRT ranges are informative, yet traders often execute on lower timeframes without that context. We implement an MQL5 indicator that reads higher-timeframe OHLC, projects the full candle range, body, and wicks onto the active lower-timeframe chart, and marks entries, stops, and targets. This improves situational awareness and removes the need to switch windows.

We introduce an MQL5 discipline engine that enforces risk consistently at the account level. It continuously scans positions from any source, validates SL/TP, equity-based exposure, and target R:R, and automatically corrects deviations by setting levels or adjusting volume. The result is uniform risk structure across manual and EA trades, supported by on-chart feedback and mode-based control.

Create an object-oriented fair value gap (FVG) scanner in MQL5 and display liquidity gaps directly on a MetaTrader 5 chart, this article formalizes the imbalance geometry based on three candlesticks, synchronizes OHLC arrays with CopyRates, manages rectangles without leaks, and monitors mitigation in real time. It also shows how to integrate this class into an Expert Advisor with a strict new bar filter for stable and efficient execution.

The article applies the A* heuristic to market structure by modeling validated swing highs and lows as graph nodes and weighting edges with ATR‑normalized distance, spread, and noise penalties. The engine searches the most efficient route to infer trade direction and targets, then filters signals by directional ratio, total path cost, and opposing swings. It anchors TP to the final node and SL to prior structure, with on‑chart visualization and configurable inputs.

Our next focus in these series on ideas that can be rapidly prototyped with the MQL5 Wizard, is a Custom Trailing class that uses the Blooming Filter. Trailing Stop systems are an optional but very resourceful part to any trading system that we want to explore more in these series besides the traditional Entry Signals.

We present a chart-embedded RSI panel that removes the need for a separate window by attaching momentum directly to live price. The article explains the design and MQL5 code: real-time RSI retrieval, slope-based signal classification, and adaptive positioning. Traders get RSI value, state, and signal strength where decisions are made, improving clarity across timeframes.

A backtest shows only one path among many possible outcomes. This MQL5 script performs 1000 bootstrap Monte Carlo resamples of a trade P&L series, draws a percentile fan chart on the chart via CCanvas, and reports probability of ruin, value at risk, and 95th‑percentile worst drawdown. The result is a practical view of path risk and drawdown exposure beyond a single equity curve.

Mining central bank balance sheet data provides a picture of global liquidity in the Forex market and key currencies. We combine data from the Fed, ECB, BOJ and PBoC into a composite index and use machine learning to uncover hidden patterns. This approach turns raw data into real trading signals by combining fundamental and technical analysis.

This article presents a custom MQL5 money management class that adapts position sizing to real-time volatility using a monotonic queue for O(N) sliding-window extremes. The class applies inverse volatility scaling and optionally validates risk with an RBF network. We show implementation details in the Optimize method and compare results with the inbuilt Size-Optimized class to assess latency and risk control benefits.

This article implements a complete MQL5 Expert Advisor that monitors manually drawn support and resistance levels in real time. It synchronizes horizontal lines, detects approaches, touches, breakouts, reversals, and retests, and adds optional candlestick pattern checks. Alerts and on‑chart markers provide clear, repeatable feedback, allowing you to keep manual analysis while automating the surveillance of key price levels.

In this article, we expand our butterfly animation program with a four-stage animation pipeline: sequential curve drawing, smooth wing fill fading, detailed body rendering, and continuous flight. We implement a timer-driven state machine, four oscillators for wing flapping, vertical bobbing, horizontal sway, and tilt, as well as a neon glow around the wing outlines and a cyclical color change based on hue. You will learn how to structure these effects on the MetaTrader 5 canvas for clean and controlled playback.

The article describes a variant of options emulation through an underlying asset implemented in the MQL5 programming language. The pros and cons of the chosen approach are compared with real exchange options using the example of the FORTS futures market of the MOEX Moscow exchange and the Bybit crypto exchange.

We build a lightweight bridge that captures closed trades in MetaTrader 5 and sends them to an external backend over HTTP as JSON. It uses OnTradeTransaction for event detection, reads details from deal history, assembles a JSON payload, and posts it via WebRequest. A local Flask API is used to test the flow, delivering a working path to move trade data outside the terminal.

We implement an MQL5 expert advisor that detects order blocks formed after consolidation breakouts and confirms them with fair value gaps. Each zone is validated by a break of structure and a preceding inducement, then filtered by the higher-timeframe trend. The program adds mitigation tracking, risk-based lot sizing, and two trailing stop modes, providing clear on-chart visuals and backtest-ready trade execution logic.

The CATCH framework combines Fourier transform and frequency patching to accurately identify market anomalies beyond the reach of traditional methods. Let us examine how this approach reveals hidden patterns in financial data.

We continue to build the algorithms that form the basis of the DADA framework, which is an advanced tool for detecting anomalies in time series. This approach enables effective distinguishing random fluctuations from significant deviations. Unlike classical methods, DADA dynamically adapts to different data types, choosing the optimal compression level in each specific case.

This article implements an MQL5 module that analyzes the lower‑timeframe bars inside each liquidity‑zone base candle. It detects swing points and applies objective rules to classify the internal structure as an ascending, descending, or symmetrical triangle; a rectangle; M; W; or undefined. The indicator displays geometry labels on the chart and adds the pattern to alerts, reducing manual lower‑timeframe inspection.

An MQL5 control system that blocks orders outside scheduled trading hours and during scheduled news releases, converting time rules into executable restrictions. It combines a permissions management mechanism, a transaction-level expert advisor, and a visual dashboard for real-time status and upcoming restrictions. Configuration is accomplished using editable files, with caching and a CSV audit log for traceability.

We expand the capabilities of the MetaTrader 5 butterfly curve canvas by adding multi-layered wing fills, vein lines, scale dots, and a full body (abdomen, thorax, head, eyes, antennae). This article implements polygon fills with vertical and radial gradients, as well as filled circles and ellipses, all using supersampling antialiasing. You will also receive reusable MQL5 helper functions and a rendering order that transforms a simple curve into a customizable, detailed chart illustration.

Self-training EA with a neural network based on a state matrix. We combine Markov chains with a multilayer neural network MLP developed using the ALGLIB MQL5 library. How can Markov chains and neural networks be combined for Forex forecasting?

Forecasting the movements of currency pairs is an important factor in trading success. This article explores various price movement models, analyzes their advantages and disadvantages, and explores their practical application in trading strategies. We will consider approaches that allow us to identify hidden patterns and improve the accuracy of forecasts.

We are going to create a matrix forecasting model based on a Markov chain. What are Markov chains, and how can we use a Markov chain for Forex trading?

The article presents an MQL5 method for detecting psychological round numbers by converting prices to strings and counting trailing zeros (ZeroSize). It outlines the theory of institutional liquidity at integers, explains the GetZeroCount logic with tick-size normalization to avoid floating‑point errors, and details hierarchical visualization. Case studies across forex, metals, and crypto, plus timeframe filters and inputs, show how to use confluence and basic risk controls in practice.