A reproducible, read-only Python audit for MetaTrader 5 that verifies history quality before any backtest. It exports M5 data from multiple terminals, detects gaps and synthetic bars by timestamp spacing, and reports coverage per year. The same deterministic strategy then runs on three broker feeds over a common window to quantify result drift and decompose it into spread, data/price, and trade effects.

Despite what was shown in the previous article, all of this may seem simple at first. In reality, several problems remain, along with many tasks that still need to be completed. You, dear reader, may imagine that everything is easy and straightforward. Out of inexperience, you may simply accept whatever is presented to you. And that is a mistake you should try to avoid. Even worse is trying to use something without truly understanding what exactly you are using. Beginners often pass through a copy-and-paste stage. If you do not want to remain stuck at that stage forever, you should learn how to use certain tools. One of the tools most often used by programmers is documentation. The second is testing, supported by log files. Here we will see how to do this.

Here we will start bringing together different components or applications that were previously completely isolated from each other. Chart Trade, the mouse indicator, and the Expert Advisor had already been linked to one another, but there was still no way to directly display on the chart the positions open on the trading server, which are often managed using a cross-order system. From this point on, this becomes possible, opening the way for various ideas and future implementations. Although we are only beginning to put these components into operation, we already have a direction for further development.

We extend the stateful supply and demand framework for MetaTrader 5 with a quantitative admission model and a dedicated interaction engine. Candidate zones are scored by structural symmetry, volume participation, and ATR‑normalized displacement, then classified into objective tiers. Admitted zones follow a deterministic lifecycle that tracks first touch, validates bounces, or confirms breakouts, with full telemetry for analysis and reproducibility.

In previous articles, we mentioned that sometimes we need to set a value for the ZOrder property. But why? The reason is that many pieces of code that add objects to a chart simply do not use, or more precisely do not define, a value for this property. The point is that I am not here to say what every programmer should or should not do, or how they should or should not write their code. I am here to show you, dear reader, and everyone who truly wants to understand how these processes work internally, what actually happens behind the scenes.

In this article, I will show how to use an indicator to track open positions on the trading server in the simplest and most practical way possible. I am doing this step by step to show that you do not necessarily have to move all of this into an Expert Advisor. Many of you have probably become used to doing that for one reason or another. In fact, that is not really justified, because as this implementation evolves, it will become clear that you can create or implement different types of indicators for this purpose.

The content we will cover from this point on is much more complex in terms of theory and concepts. I will try to make the material as simple as possible. The programming part itself is quite simple and straightforward. But if you do not understand the theory behind it, you will be left with no practical basis at all for refining or adapting the replay/simulation system to tasks different from the ones I am going to show. I do not want you merely to compile and use the code I present. I want you to learn, understand and, if possible, be able to create something even better.

This article demonstrates how to build a reusable prop‑firm evaluation module for MQL5 Expert Advisors and export results to an HTML dashboard. The module monitors balance and equity during backtests, simulates single or rolling challenges, checks profit target, daily and overall drawdown, and minimum trading days, then outputs both a terminal summary and a browser‑readable report.

We present a complete workflow for adaptive filtering in MQL5 using the CNlEq Levenberg–Marquardt–like solver. The EA fits a VAMAC model—two EWMAs with an ATR‑based scaling—by supplying residuals and a Jacobian through CNlEq's reverse‑communication loop, with optional numerical or analytical derivatives. Code, setup instructions, and GBPUSD H1 tests show how to replace static thresholds with on‑bar re‑estimation.

This article advances the stateful supply and demand zone framework for MetaTrader 5 by replacing polling with an event-driven model based on OnChartEvent(). We split synchronization into dedicated handlers for creation, modification, and deletion, and separate market logic in OnTick() from user interactions in OnChartEvent(). A persistent, append-only CSV logger records all lifecycle events, improving responsiveness, state consistency, and recoverable history for downstream analysis.

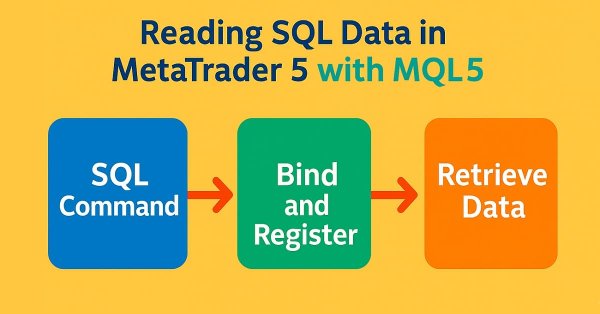

In the previous article, I showed how to proceed in order to add a query mechanism. This was needed so that, inside MQL5 code, you could fully use SQL and retrieve results using an SQL SELECT query. But there is still one last function we need to implement. This is the DatabaseReadBind function. Since understanding it properly requires a slightly more detailed explanation, it was decided to cover it not in the previous article, but in today's article. So, since the topic will be fairly extensive, let us proceed directly to the next section.

Many people tend to underestimate SQL, or even not use it at all, because they do not fully understand how it actually works. When running queries against an SQL database, we are not always looking for a universal answer; in some cases, we need a very specific and practical answer. If a database is created with a proper structure and data model, almost any type of information can be integrated into it.

The article presents an MQL5 Expert Advisor that adapts the Ford–Fulkerson max-flow method into a liquidity-capacity filter. Market structures—Swing Highs/Lows, Fair Value Gaps, Order Blocks, and Liquidity Pools—form a directed graph with edge capacities from volume, price reaction, distance, and structure quality. Maximum flow qualifies ICT setups, filters weak paths, and drives dynamic position sizing for a consistent, two-stage decision process.

Multi-core optimization in MetaTrader 5 can silently drop results when parallel agents contend for the same CSV file. A reusable MQL5 export engine applies an iteration-based spin-lock to acquire the file handle reliably and append rows without loss. It persists custom metrics such as the Sortino Ratio, average trade duration, and signal-quality measures (lag and whipsaws) into a consolidated CSV for downstream analysis.

In today's article we will begin studying the use of SQL in MQL5 code. We will also look at how to create a database. Or, more precisely, how to create a SQLite database file using the features built into MQL5. We will also see how to create a table, and then how to establish a relationship between tables by using primary and foreign keys. All of this, once again, will be done with MQL5. We will see how easy it is to create code that can later be migrated to other SQL implementations by using a class that helps hide the implementation being created. And, most importantly, we will see that at various points we may face the risk that something will go wrong when using SQL. This happens because, in MQL5 code, SQL code will always be placed inside a string.

Replace static drawings with automated, stateful zones controlled by a CZone wrapper. The system synchronizes user rectangles, sizes zones by ATR, validates breakouts using consecutive closes, applies ghost/deactivation rules, merges nearby structures by a 1.5×ATR threshold, and projects edges forward. Traders gain durable levels that update themselves and reduce repetitive chart management.

In the previous article, we completed the necessary introduction to SQL. And, in my opinion, we properly clarified what we wanted to show and explain about SQL. This was done so that anyone who comes to look at the market replay/simulation system being built can at least get an idea of what may be happening there. The point is that there is no sense in programming things that SQL handles perfectly.

In this article, we will see how to visualize a database and, from that, understand how it is structured. This is done by analyzing the database’s internal structure. Although this may seem unnecessary at first, it is fully justified if we really want to become database administrators. After all, some people make a living maintaining and designing databases.

Before you give up and decide to abandon learning SQL, allow me to remind you, dear readers, that here we are still using only the most basic elements. We have not yet looked at some of SQL's capabilities. Once you understand them, you will see that SQL is far more practical than it seems. Although, most likely, we will eventually change the direction of what we are building, because the creation process is dynamic. We will show a little more about creating different things in SQL, because this is truly important and useful for you. Simply thinking that you are more capable than an entire community of programmers and developers will only lead to wasted time and opportunities. Do not worry, because what comes next will be even more interesting.

Many of you may have far more experience working with databases than I do, and therefore may have a different opinion. Since it was necessary to explain why databases are designed the way they are, and why SQL has the form it does—especially why primary and foreign keys emerged—some things had to remain somewhat abstract.

This article presents a multi-symbol execution filter that scores real-time market quality before any trade is allowed. It measures spread behavior, tick velocity, quote gaps, micro-volatility, and a slippage estimate, then classifies the state to block degraded conditions. Once noise settles, a liquidity sweep continuation model evaluates structure shifts so entries occur only when execution is mechanically stable.

The article defines a buffer-based signal architecture for flag breakouts and an EA that consumes it. Breakout arrows and pole height are written to dedicated buffers only after confirmation, preventing repainting and ambiguity. The EA polls buffers with CopyBuffer(), validates signals using configurable filters, and executes trades with fixed or dynamic SL/TP.

The article examines an engineering approach to optimizing an Expert Advisor in MetaTrader 5: from collecting custom metrics through Optimization Frames to parameter surface analysis. A simple event-driven EMA/RSI model demonstrates CSV export, smoothing, and local stability assessment in Python. The goal is to find stable areas of configurations and validate them with forward optimization for reliable implementation.

In this article, we demonstrate how to use API of the MetaTrader 5 custom symbols to transform your terminal into a data constructor for generating timeless Renko, Range, and Equal-Volume charts and assembling synthetic instruments. We will analyze tick aggregation and history modification for stress tests (spread widening, stop level changes) taking into account platform limitations. Besides, you will get some practice of handling CiCustomSymbol and routing orders to a real symbol through the CustomOrder wrapper with ready-made code fragments.

Learn how to build a manual backtesting EA for MetaTrader 5's visual tester by adding chart buttons with CButton, executing orders through CTrade, and filtering positions with a magic number. The article implements Buy/Sell and Close All controls, configurable lot size and initial SL, and a trailing stop via CPositionInfo. You will also see how to load indicators with tester.tpl to validate ideas faster before automation and narrow optimization ranges.

A custom forward simulation engine detects fast/slow EMA crossovers and immediately projects synthetic candles ahead of the signal bar. It generates bodies and wicks using controlled logic, draws them with chart objects, and refreshes on every new signal or anchor change. You get a clear forward-looking view to test timing, visualize scenarios, and manage invalidation on the chart.

The article presents a systematic approach to news trading in MetaTrader 5 using the built-in economic calendar: data structure, API functions, time synchronization rules, and event filtering. Methods of caching and incremental updating without overloading the server are described. The article also provides a working mechanism for exporting history to an .EX5 resource for deterministic testing using the same algorithm.

The article applies the A* heuristic to market structure by modeling validated swing highs and lows as graph nodes and weighting edges with ATR‑normalized distance, spread, and noise penalties. The engine searches the most efficient route to infer trade direction and targets, then filters signals by directional ratio, total path cost, and opposing swings. It anchors TP to the final node and SL to prior structure, with on‑chart visualization and configurable inputs.

A backtest shows only one path among many possible outcomes. This MQL5 script performs 1000 bootstrap Monte Carlo resamples of a trade P&L series, draws a percentile fan chart on the chart via CCanvas, and reports probability of ruin, value at risk, and 95th‑percentile worst drawdown. The result is a practical view of path risk and drawdown exposure beyond a single equity curve.

If there is a need to display text on a chart, we can use the Comment() function. But its capabilities are quite limited. Therefore, in this article, we will create our own component - a full-screen dialog window capable of displaying multi-line text with flexible font settings and scrolling support.

This article implements a static, CSV-based news source for the Strategy Tester, so historical economic news events can be preloaded and queried during backtesting. It replaces live calendar calls in tester mode with a fast in-memory search, preserves the live logic for trading, and delivers deterministic, repeatable results with explicit control over included events, enabling reliable validation of news-aware filters, stop suspension, and trade-blocking rules.

This article presents an EA that automates the previously introduced Market Entropy methodology. It computes fast and slow entropy, momentum, and compression states, validates signals, and executes orders with SL/TP and optional position reversal. The result is a practical, configurable tool that applies information-theoretic signals without manual interpretation.

This article presents a Time-of-Day capital rotation engine for MQL5 that allocates risk by trading session instead of using uniform exposure. We detail session budgets within a daily risk cap, dynamic lot sizing from remaining session risk, and automatic daily resets. Execution uses session-specific breakout and fade logic with ATR-based volatility confirmation. Readers gain a practical template to deploy capital where session conditions are statistically strongest while keeping exposure controlled throughout the day.

We continue studying the chaotic optimization algorithm. The second part of the article deals with the practical aspects of the algorithm implementation, its testing and conclusions.

Before moving forward with the development of multi-currency EAs, let's try to switch to creating a new project using the developed library. This example will demonstrate how to best organize source code storage and how using the new code repository from MetaQuotes can help us.

Although we can perform operations on a database containing about 10 records, the material is absorbed much better when we work with a file that contains more than 15 thousand records. That is, if we tried to create such a database manually, this task would be enormous. However, it is difficult to find such a database, even for educational purposes, that is available for download. But in reality, we don’t need to resort to that — we can use MetaTrader 5 to create a database for ourselves. In today's article, we will look at how to do this.

This article presents an MQL5 Expert Advisor that upgrades raw swing detection to a rule-based Structural Validation Engine. Swings are confirmed by a break of structure, displacement, liquidity sweeps, or time-based respect, then linked to a liquidity map and a structural state machine. The result is context-aware entries and stops anchored to validated levels, helping filter noise and systematize execution.

As we explained in the first article about SQL, there is no point in spending time programming procedures to do what is already built into SQL. However, without knowing the basics, you won’t be able to do anything with SQL or take full advantage of everything this tool offers. Therefore, in this article, we will look at how to perform basic tasks in databases.

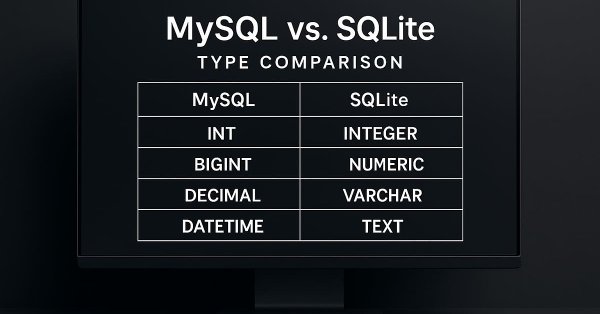

It doesn't matter which SQL program we use: MySQL, SQL Server, SQLite, OpenSQL, or another. They all have something in common, and the common element is the SQL language. Even if we do not intend to use Workbench, we can manipulate or work with the database directly in MetaEditor or through MQL5 to perform actions in MetaTrader 5, but to do so, you will need knowledge of SQL. So here, we will learn at least the basics.

The implementation of the part of the code that will run in MetaTrader 5 does not present any difficulty. However, there are several points that need to be taken into account. This is necessary so that you can make the system work. Remember one important thing: not just one program will be running. In reality, we will have to run three programs simultaneously. It is important to implement and structure each of them in such a way that they can interact and communicate with one another, and that each of them understands what the others are trying or intending to do.