This article shows how to run Python-trained models natively in MetaTrader 5 via the terminal's ONNX functions. We build an MQL5 class that encapsulates session creation, fixes input/output tensor shapes, applies min-max feature normalization to mirror training, and executes OnnxRun once per bar to protect the CPU, the result is a reliable, maintainable inference path for live charts and the Strategy Tester without sockets or DLLs.

This work presents an end-to-end pipeline: collect MetaTrader 5 data, engineer entropy/volatility/trend features, train a PyTorch classifier, and expose predictions through a Flask API. An MQL5 EA posts rolling prices each tick, receives probability and regime, and applies adaptive position sizing and stop distances. The result is a clear recipe for integrating ML inference with MetaTrader 5.

This article presents a custom MQL5 signal class, CSignalBitwisePerceptron, for ultra-lightweight entry logic. It packs 64 bars into a single uint64 via bitwise vectorization and evaluates them with a perceptron that sums weights only for active bits. A two-gate flow (algorithmic hash map plus neural threshold) minimizes array iteration and heavy math. Readers get a practical template to cut latency and refine entry validation.

This article starts the MMAR pipeline on EURUSD M5 data. We load market data via the MetaTrader5 Python API and run partition-function analysis with non-overlapping intervals to test for multifractal scaling. The result is an evidence-based decision on fractality, a prerequisite for building MMAR and for choosing whether to proceed beyond GARCH.

Downloading international monetary fund data in Python: Mining IMF data for use in macroeconomic currency strategies. How can macroeconomics help an ordinary and an algorithmic trader?

Biogeography-Based Optimization (BBO) is an elegant global optimization method inspired by natural processes of species migration between islands within archipelagos. The algorithm is based on a simple yet powerful idea: high-quality solutions actively share their characteristics, while low-quality ones actively adopt new features, creating a natural flow of information from the best solutions to the worst. A unique adaptive mutation operator provides an excellent balance between exploration and exploitation. BBO demonstrates high efficiency on a variety of tasks.

The article describes the arrangement of a coordinated ML pipeline in MetaTrader 5 with separation of roles: Python trains and exports the model to ONNX, MQL5 reproduces normalization and PCA via matrix/vector and performs inference. This approach makes the model's inputs stable and verifiable, and the MetaTrader 5 strategy tester provides metrics for analyzing the system behavior.

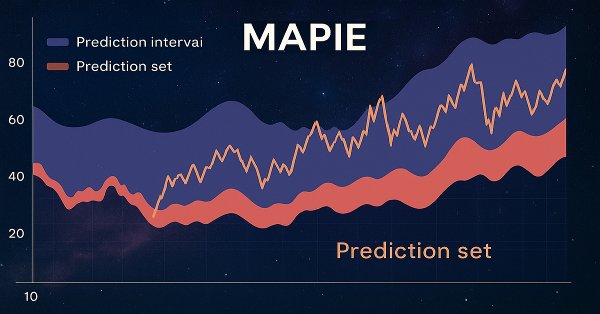

In this article, we will consider conformal predictions and the MAPIE library that implements them. This approach is one of the most modern ones in machine learning and allows us to focus on risk management for existing diverse machine learning models. Conformal predictions, by themselves, are not a way to find patterns in data. They only determine the degree of confidence of existing models in predicting specific examples and allow filtering for reliable predictions.

This article applies the Optimal Trading Rule from AFML Chapter 13 to set profit targets and stop-losses without in-sample calibration. We model post-entry P&L with a discrete Ornstein–Uhlenbeck process, run a 100,000-path search, and implement Python, multiprocessing, and a Numba @njit parallel kernel (242× faster). The result is an optimal (PT, SL) under three forecast specifications, constrained by the prop-firm daily loss limit.

This article builds the foundation layer of a twelve-part MQL5 market microstructure toolkit. It implements guarded math helpers (SafeDivide, SafeLog, SafeSqrt, SafeExp, SafeTanh), robust data validation (ValidateSymbolV2, SafeCopyClose), trimmed statistical estimators (robust mean var), a linear regression slope, shared structs, and an FFT. You compile a single include file that hardens indicators and expert advisors against silent numerical failures and standardizes data flow for later parts.

Our next focus in these series on ideas that can be rapidly prototyped with the MQL5 Wizard, is a Custom Trailing class that uses the Blooming Filter. Trailing Stop systems are an optional but very resourceful part to any trading system that we want to explore more in these series besides the traditional Entry Signals.

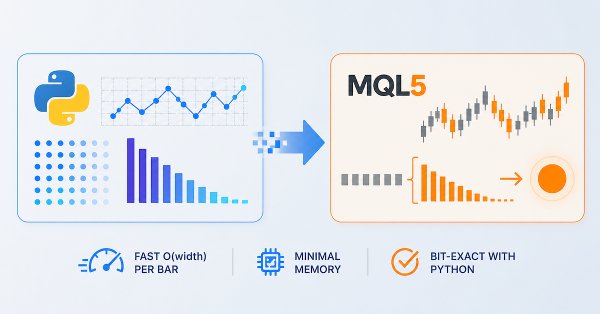

This article delivers a production-grade MQL5 implementation of fixed-width fractional differentiation for live MetaTrader 5 feeds. We introduce a header-only CFFDEngine that precomputes weights without a fixed cap, performs O(width) per-bar updates, and avoids per-tick allocations. The FFD.mq5 indicator supports all ENUM_APPLIED_PRICE types and prev_calculated optimization. Validation scripts confirm numerical equivalence with the standard Python frac diff_ffd pipeline.

The article demonstrates how Python and MetaTrader 5 integration combines research flexibility and trade execution into a single workflow. Python is used for data analysis, feature selection and model training, while MetaTrader 5 is used for testing and trading automation. This approach simplifies the transfer of solutions into practice, increases reproducibility, and makes the development of trading systems faster and more structured.

Let's try mining CFTC data, downloading COT and TFF reports via Python, connecting all this with MetaTrader 5 quotes and an AI model, and get forecasts. What are COT reports in the Forex market? How to use COT and TFF reports for forecasting?

Mining central bank balance sheet data provides a picture of global liquidity in the Forex market and key currencies. We combine data from the Fed, ECB, BOJ and PBoC into a composite index and use machine learning to uncover hidden patterns. This approach turns raw data into real trading signals by combining fundamental and technical analysis.

This article presents a custom MQL5 money management class that adapts position sizing to real-time volatility using a monotonic queue for O(N) sliding-window extremes. The class applies inverse volatility scaling and optionally validates risk with an RBF network. We show implementation details in the Optimize method and compare results with the inbuilt Size-Optimized class to assess latency and risk control benefits.

Adaptation of the classical CAPM model for the Forex currency market in MQL5. The indicator calculates expected return and risk premium based on historical volatility. The indicators rise at peaks and bottoms, reflecting the fundamental principles of pricing. Practical application for counter-trend and trend-following strategies, taking into account the dynamics of the risk-reward ratio in real time. The article includes mathematical apparatus and technical implementation.

The CATCH framework combines Fourier transform and frequency patching to accurately identify market anomalies beyond the reach of traditional methods. Let us examine how this approach reveals hidden patterns in financial data.

We continue to build the algorithms that form the basis of the DADA framework, which is an advanced tool for detecting anomalies in time series. This approach enables effective distinguishing random fluctuations from significant deviations. Unlike classical methods, DADA dynamically adapts to different data types, choosing the optimal compression level in each specific case.

Deterministic Oscillatory Search (DOS) algorithm is an innovative global optimization method that combines the advantages of gradient and swarm algorithms without the use of random numbers. The fitness oscillation and slope mechanism allows DOS to explore complex search spaces in a deterministic manner.

We build a production MQL5 bet‑sizing toolkit: utilities, snippets, and user‑level functions that mirror the Python originals. The methods cover probability‑to‑size mapping with overlap correction, dynamic forecast‑price sizing (calibrated sigmoid/power with limit price), occupancy‑based budgeting, and mixture‑model reserve sizing (EF3M). The result is a signed [−1, ..., 1] position plus diagnostics you can plug directly into order logic.

Self-training EA with a neural network based on a state matrix. We combine Markov chains with a multilayer neural network MLP developed using the ALGLIB MQL5 library. How can Markov chains and neural networks be combined for Forex forecasting?

We are going to create a matrix forecasting model based on a Markov chain. What are Markov chains, and how can we use a Markov chain for Forex trading?

Computer vision for trading: how it works and how to develop it step by step. We create an algorithm for recognition of RGB images of price charts using the attention mechanism and a bidirectional LSTM layer. As a result, we obtain a working model for forecasting the EURUSD price with the accuracy of up to 55% in the validation section.

The Camel Algorithm, developed in 2016, simulates the behavior of camels in the desert to solve optimization problems, taking into account temperature, supply, and endurance. This article also presents a modified version of the algorithm (CAm) with key improvements: the use of a Gaussian distribution in generating solutions and the optimization of the oasis effect parameters.

Time series forecasting in trading has evolved from traditional statistical models (like ARIMA) to deep learning approaches, but both require heavy tuning and training. Inspired by advances in NLP, Google’s TimesFM introduces a pretrained “foundation model” for time series that can perform strong forecasts even without task-specific training. For traders, this is powerful because it can be efficiently fine-tuned on their own data using lightweight methods like LoRA, reducing overfitting while adapting to changing market conditions.

Hidden Markov Models (HMMs) are a powerful class of probabilistic models designed to analyze sequential data, where observed events depend on some sequence of unobserved (hidden) states that form a Markov process. The main assumptions of HMM include the Markov property for hidden states, meaning that the probability of transition to the next state depends only on the current state, and the independence of observations given knowledge of the current hidden state.

The article presents a new metaheuristic method based on a fractal approach to partitioning the search space for solving optimization problems. The algorithm sequentially identifies and separates promising areas, creating a self-similar fractal structure that concentrates computing resources on the most promising areas. A unique mutation mechanism aimed at better solutions ensures an optimal balance between exploration and exploitation of the search space, significantly increasing the efficiency of the algorithm.

Integer differentiation forces a binary choice between stationarity and memory: returns (d=1) are stationary but discard all price-level information; raw prices (d=0) preserve memory but violate ML stationarity assumptions. We implement the fixed-width fractional differentiation (FFD) method from AFML Chapter 5, covering get_weights_ffd (iterative recurrence with threshold cutoff), frac_diff_ffd (bounded dot product per bar), and fracdiff_optimal (binary search for minimum stationary d*).

Tree-based classifiers are typically overconfident: true win rates near 0.55 appear as 0.65–0.80 and inflate position sizes and Kelly fractions. This article presents afml.calibration and CalibratorCV, which generate out-of-fold predictions via PurgedKFold and fit isotonic regression or Platt scaling. We define Brier score, ECE, and MCE, and show diagnostics that trace miscalibration into position sizes, realized P&L, and CPCV path Sharpe distributions to support leakage-free, correctly sized trading.

The article contains a detailed description of the cross-rate calculation algorithm, a visualization of the imbalance matrix, and recommendations for optimally setting the MinDiscrepancy and MaxRisk parameters for efficient trading. The system automatically calculates the "fair value" of each currency pair using cross rates, generating buy signals in case of negative deviations and sell signals in case of positive ones.

We continue studying the chaotic optimization algorithm. The second part of the article deals with the practical aspects of the algorithm implementation, its testing and conclusions.

This is an improved chaotic optimization algorithm (COA) that combines the effects of chaos with adaptive search mechanisms. The algorithm uses a set of chaotic maps and inertial components to explore the search space. The article reveals the theoretical foundations of chaotic methods of financial optimization.

How to use Renko bars with AI? Let's look at Renko trading on Forex with forecast accuracy of up to 59.27%. We will explore the benefits of Renko bars for filtering market noise, learn why volume is more important than price patterns, and how to set the optimal Renko block size for EURUSD. This is a step-by-step guide on integrating CatBoost, Python, and MetaTrader 5 to create your own Renko Forex forecasting system. It is ideal for traders looking to go beyond traditional technical analysis.

The bet-sizing signal from Part 10 is concurrency-corrected but carries no payoff-ratio adjustment, no response to a hard drawdown budget, and no validation across combinatorial paths. This article covers three additions: a two-stage architecture in which a Kelly payoff multiplier is applied on top of get_signal, preserving the concurrency correction while incorporating win/loss asymmetry; a prop firm integration layer that calibrates the sigmoid w parameter continuously from the remaining drawdown budget under FundedNext Stellar 2-Step rules; and a CPCV backtest framework that simulates a fresh account state across all φ[N, k] paths, producing a Sharpe distribution and a PBO audit.

Fixed fractions and raw probabilities misallocate risk under overlapping labels and induce overtrading. This article delivers four AFML-compliant sizers: probability-based (z-score → CDF, active-bet averaging, discretization), forecast-price (sigmoid/power with w calibration and limit price), budget-constrained (direction-only), and reserve (mixture-CDF via EF3M). You get a signed, bounded position series with documented conditions of use.

In this article, we will explore what pair trading is and how correlation trading works. We will also create an EA for automating pair trading and add the ability to automatically optimize this trading algorithm based on historical data. In addition, as part of the project, we will learn how to calculate the differences between two pairs using the z-score.

This article introduces Jardine's Gate, a six-gate orthogonal signal filter for MetaTrader 5 that validates LSTM predictions across entropy, expert interference, confidence, regime-adjusted probability, trend direction, and consecutive-loss kill switch dimensions. Out of 43,200 raw signals per month, only 127 pass all six gates. Readers get the complete QuantumEdgeFilter MQL5 class, threshold calibration logic, and gate performance analytics.

The article presents a comprehensive analysis of the Coral Reef Optimization (CRO) algorithm, a metaheuristic method inspired by the biological processes of coral reef formation and development. The algorithm models key aspects of coral evolution: broadcast spawning, brooding, larval settlement, asexual reproduction, and competition for limited reef space. Particular attention is paid to the improved version of the algorithm.

We invite you to get acquainted with the DADA framework, which is an innovative method for detecting anomalies in time series. It helps distinguish random fluctuations from suspicious deviations. Unlike traditional methods, DADA is flexible and adapts to different data. Instead of a fixed compression level, it uses several options and chooses the most appropriate one for each case.